Uber Is a Growth Business That Has Trouble Growing

The ride-hailing company’s latest IPO filing demonstrates the need to expand into new markets and businesses.

(Bloomberg Opinion) -- Remember this moment. Early 2019 may have showed us the ceiling for the business of selling car rides at the tap of a smartphone.

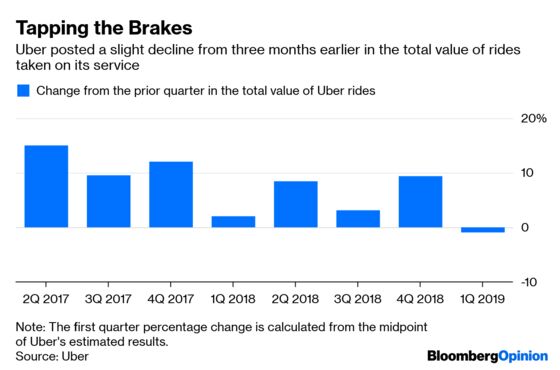

In an updated financial document for its coming initial public offering, Uber Technologies Inc. disclosed that the total value of rides on its service was between $11.3 billion and $11.45 billion in the first quarter of the year. At the midpoint of that range, that would be a 1 percent decline from the total value of rides the company recorded in the December quarter.

Uber is a growth business whose largest business stopped growing, at least for now.

The quarter-over-quarter decline in what Uber calls “gross bookings” for rides in Uber cars, motorbikes and taxis needs context. Looking at Uber’s prior first-quarter growth rates for the total value of rides on its service, there is pattern of dips between the December quarter and the one ending in March.

That seems logical. In many countries, November and December are busy months for travel, family visits and other activities that might call for an Uber ride. The U.S. dollar is strong, which weighs down companies like Uber that generate a significant share of sales in places like Brazil with wobbly currencies. Those explanations shouldn’t, however, result in a decline for a turbocharged growth business.

This dip in ride bookings didn’t come of the blue. It’s been clear from Uber’s disclosure of select financials even before its IPO filing that its on-demand ride business, which generates about 80 percent of the total value of its services, was slowing. Uber is asking investors to buy up to $9 billion in shares — valuing the company at up to $91.5 billion, including shares held by employees and others — just as on-demand rides have stopped growing.

The fresh numbers from Uber take me back to the question I had when Lyft Inc. went public: What if demand simply isn’t very large for rides in de facto taxis? To be fair, 5.2 billion rides or food deliveries were made with Uber worldwide last year, and that’s not nothing. And the total number of car rides, scooter trips and food deliveries with Uber did increase about 4 percent in the first quarter from the December quarter.

The picture that’s emerging is that future growth for companies like Uber and Lyft will be harder to come by.

To keep growing their rides businesses, the companies will need to expand further outside the big cities that generate a significant share of demand for Uber and Lyft now. The companies will need to accelerate their efforts to get people into carpool-type shared rides, onto bicycles and electric scooters and other types of transportation that cost people less and therefore may expand the number of people likely to take a trip. Those are not easy tasks.

It makes me wonder whether Uber started its business of delivering food from restaurants because it saw this ceiling for on-demand rides and needed to shift gears to maintain growth. Optimists will see that as a savvy move. Uber loves comparing itself to Amazon, so let’s say it was smart of Amazon to shift from initially selling books — surely not a long-term growth business — to selling every physical good possible.

That comparison assumes there is some commonality between connecting drivers with people who want a car ride across town and signing up restaurants who want to reach hungry people. I’m not convinced there is as much overlap as Uber pitches to investors.

Yes, maybe if I’m used to taking Uber rides I will be more likely to try Uber Eats to order a burger and fries from my sofa. But I’m not sure Uber’s logistics expertise in rides gives it special advantages to help the burger restaurant in my neighborhood reach potential diners. Uber Eats is the company’s only large fast-growing division, and a bet on Uber’s IPO is effectively a wager that the company can supercharge the food-delivery industry and eventually turn a profit from burritos on-demand.

This fresh information fuels investors to ask tough questions of themselves and Uber executives as the company pitches its IPO. Buying stock in a company going public is inherently a gamble. Now that Uber’s main business has reached a plateau, investors in Uber’s IPO will essentially be betting that the company can find more markets to conquer.

The total value of rides increased 21 percent from the first quarter of 2018.

Uber says one-quarter of its ride gross bookings come from five big metropolitan areas: Los Angeles, New York City, San Francisco and the surrounding area, London and Sao Paulo.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.