Hey China! Check How the U.S. Trade War With Japan Went Down

(Bloomberg Opinion) -- China may be suffering from President Donald Trump’s trade war. A substantial number of Chinese companies are laying off staff, cutting wages and reducing capital expenditures. Prices are being slashed on goods subject to tariffs. And China’s export growth has slowed.

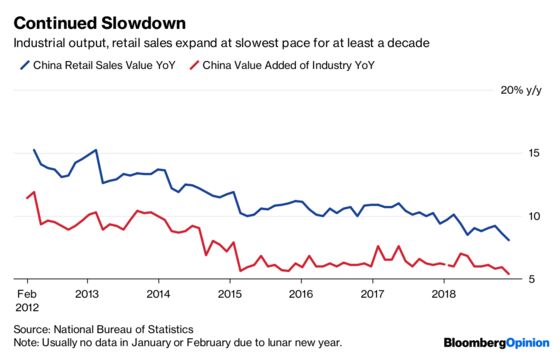

Of course, U.S. consumers and manufacturers will also get hurt by the tariffs. And there’s a chance that China’s slowdown is just a coincidence, and that the trade war has only slightly exacerbated the pain. China had already been trying to cool off credit growth in its shadow banking system, and its economy has been decelerating for the past six years:

But nevertheless, there’s a strong possibility that tariffs — and quieter but potentially more important restrictions on tech exports to and investment from China — are causing China pain. That raises the question of what kind of concessions the U.S. can demand from China, and what China is likely to agree to, in order to end that the conflict.

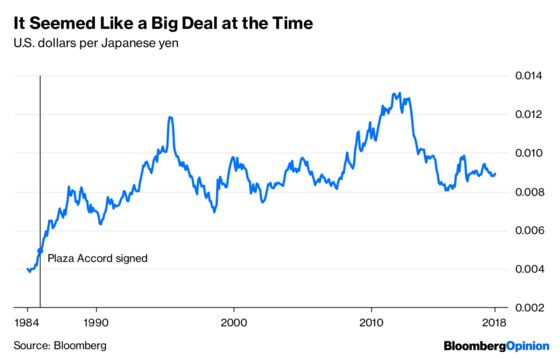

Earlier this year I suggested that one aim — in addition to concessions on intellectual property and lifting restrictions on U.S. business operations in China — would be to get the country to loosen its capital controls. This would help China take steps toward shouldering the burden of being the world’s reserve currency. In the short run, letting investors move money in and out of China might cause the yuan to fall in value against the dollar, but in the long run it would probably result in yuan appreciation, as global capital starts to park itself in China. This would be somewhat similar to the 1985 Plaza Accord, in which Japan and some European countries agreed to let their currencies appreciate relative to the dollar.

But it seems there’s little chance that China would agree to such a deal. Some people believe that Japan’s concessions to the U.S. in those long-ago trade talks sowed the seeds of its later economic bust in the 1990s. Thus, China’s leaders will probably be wary of repeating history.

This fear is misplaced. The Plaza Accord almost certainly did not cause Japan’s lost decade.

First of all, the agreement didn’t seem to do anything to halt Japan’s export juggernaut. Yes, the yen appreciated by about 100 percent against the dollar after 1985:

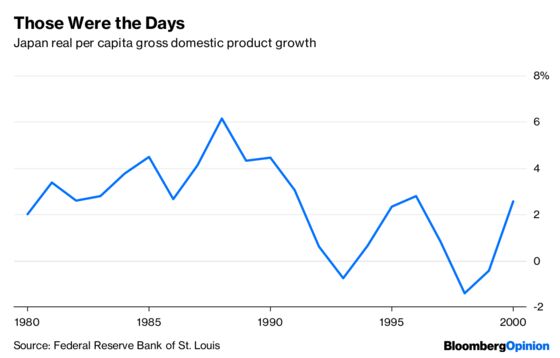

But despite the big currency swing, Japan’s trade surplus didn’t shrink much in the years that followed. What’s more, Japanese growth accelerated for years after the accord was signed. The late 1980s were a legendary boom time in Japan:

So those who believe that the Plaza Accord crushed Japan’s economy must believe that it did so through indirect means. Instead of halting Japan’s trade surpluses or slowing its growth, they must believe that the Plaza Accord gave rise to the asset bubbles whose bursting caused Japan’s economy to stagnate in the 1990s.

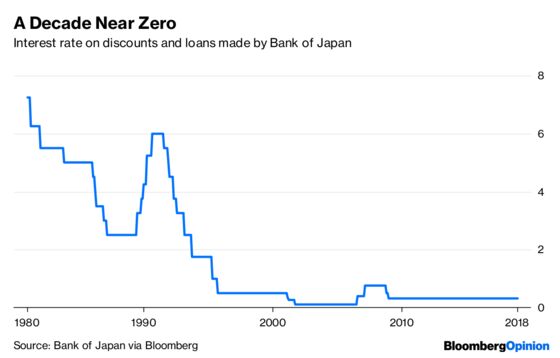

Writing in the Wall Street Journal, Peter Landers makes this argument. The idea is that the Bank of Japan, concerned that the Plaza Accord would slow Japan’s economy, kept interest rates too low in the late 1980s, giving rise to bubbles in the price of land and stocks. The BOJ cut interest rates from 5 percent in November 1985 to 2.5 percent by March 1987, and didn’t raise rates again until two years later:

But there are several problems with this account. First, even if true, it would mean that Japan’s bubble and crash weren’t really caused by the Plaza Accord, but by policy mistakes. By 1987, it should have been clear that the yen’s appreciation wasn’t causing a slowdown in exports or growth. Keeping the BOJ’s foot on the monetary accelerator for years after Plaza seems like an unforced error, rather than a necessary response to the currency deal.

Second, it’s far from clear that low interest rates are a major cause of financial bubbles. In theory, raising rates should reduce prices, by raising the opportunity cost of capital. That, in turn, could puncture the irrational exuberance, extrapolative expectations or chain of speculation that sustains a bubble. For this reason, monetary policy makers sometimes cite bubbles as a reason to avoid setting rates too low.

But in reality, the link between interest rates and bubbles is weaker than one might think. There’s only a weak correlation between interest rates and housing-price appreciation. Lab experiments generally find that paying higher interest rates does nothing to discourage bubble formation. And a number of countries have found that it’s hard to restrain rising asset prices via government policy without sending the economy into recession, meaning that the cure might be worse than the disease.

So it seems highly unlikely that the Plaza Accord caused Japan’s economic crash and lost decade, even indirectly through monetary policy. So China shouldn’t be afraid of coming to a similar arrangement with the U.S.

But there’s also the possibility that such an arrangement wouldn’t accomplish much after all. If a doubling of Japan’s currency didn’t put a dent in its trade surplus with the U.S., removing China’s capital controls might also leave the two countries’ trade imbalance intact. It’s still a good thing to do, since China should eventually try to make the yuan a global currency. But it might not be the big victory Trump is looking for.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.