(Bloomberg Opinion) -- President Donald Trump has from time to time lobbed tweets toward OPEC, imploring it to open the spigots and boost supply to lower the price of oil. The cartel has largely ignored the pleas, but U.S. producers seem to have responded in one of the few positive developments for the economy and markets.

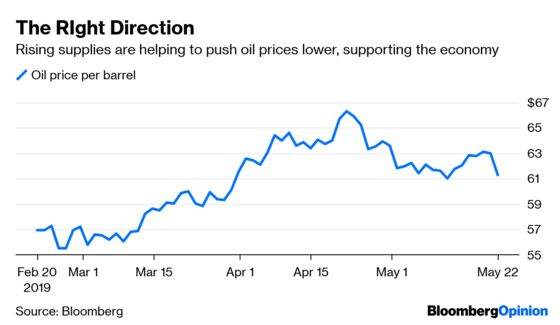

West Texas Intermediate crude futures tumbled as much as 3.11% in their biggest decline since February after the U.S. Energy Department said weekly American crude inventories swelled to the highest in almost two years. The report rekindled talk of a glut beginning to form, which helped send prices tumbling below $45 a barrel at the end of last year. Though at a low of about $61 on Wednesday, the glut would most likely have to get much bigger before oil prices fell back to those levels. Nevertheless, any declines are a welcome development when concern is rising that America’s economy might not be able to shrug off the e scalating trade war with China or the worldwide economic slowdown. After all, as recently as October oil had broken through the $75-a-barrel level and strategists were talking about $100 being reached before too long. That would be devastating for the U.S. and global economy, especially with the Organization for Economic Cooperation and Development — which had already made big cuts to its global economic projections in March — doing so again on Tuesday, trimming its 2019 forecast to 3.2% from 3.3%.

Where oil goes from here may depend on the production agreement between OPEC and Russia. While they have managed to push crude prices higher, production cuts are weighing on Russia’s economy, which expanded by just 0.5% in the first quarter, below all 14 estimates in a Bloomberg survey. There is now speculation that the President Vladimir Putin of Russia may not agree to extend the deal when it expires next month, according to Bloomberg News’s Olga Tanas.

BONDS MAY SEE SOME SUPPLY RELIEF

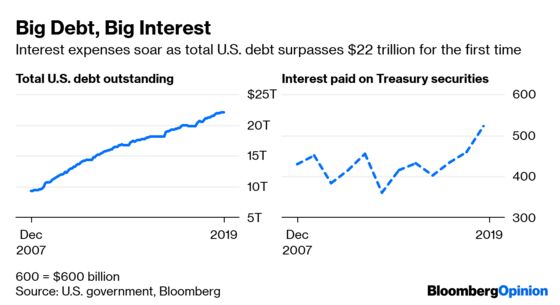

U.S. Treasuries rallied on Tuesday despite minutes of the Federal Reserve’s April 30-May 1 monetary policy meeting showing that policy makers avoided any discussion of a possible interest-rate cut. Maybe bond traders were just relieved that the meeting between Trump and Democratic leaders in Congress to discuss infrastructure fell apart. After all, it’s common knowledge that the only way to pay for what both sides have estimated would be a $2 trillion plan would entail more borrowing. And while bond yields have fallen this year, there are signs that a surge in borrowing may be causing demand at U.S. debt auctions to be trending lower. Lower demand would generally mean that the U.S. isn’t able to borrow at the best rates possible, costing taxpayers billions of dollars. The total amount of U.S. debt outstanding has grown by $2 trillion to $22 trillion under the Trump administration, while the interest that the U.S. pays out to holders of its Treasury securities has risen to $523 billion from $432.6 billion in 2016.

BUYBACKS RETURN AFTER SHORT VACATION

Although the Fed minutes showed policy makers didn’t talk rate cuts, stock traders seemed happy that they at least judged that their patient approach to monetary policy would be appropriate “for some time.” At least that’s what the brief rebound in stocks from their lows of the day after the minutes were released would suggest. Or maybe it was the return of the primary driver of stocks in recent years: corporate buybacks. With earnings season basically over, companies are back to buying their shares. Client data compiled by Bank of America showed that at $2.4 billion, the amount of buybacks last week jumped 23% from a year earlier, making the week the eighth-busiest since the firm began tracking the data in 2008, according to Bloomberg News’s Lu Wang and Vildana Hajric. Last month, the equity strategists at Goldman Sachs made evident just how important buybacks have been to stocks. Net buybacks averaged $420 billion annually since 2010, while buying from households, mutual funds, pension funds and foreign investors was less than $10 billion for each, Fed data compiled by the firm showed.

PLAYING POSSUM?

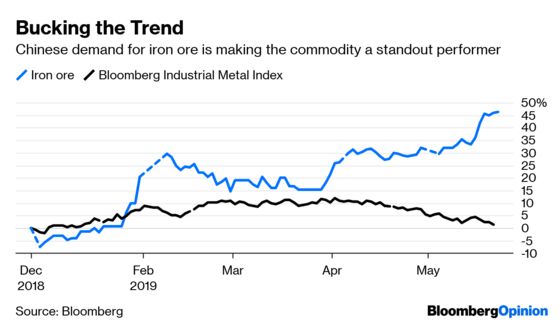

The conventional wisdom is that the trade war is hurting China more than the U.S. Indeed, the OECD estimates the country’s economy will slow by 0.4 percentage point this year, while the U.S.’s will slow by just 0.1 percentage point. But what if the data (which is generally believed to be heavily massaged before release) coming out of China that shows a softening economy is just a ruse, or at least partly a ploy to throw the U.S. off track? Admittedly, that sounds like something for the tin-foil-hat-wearing conspiracy crowd, but what else explains China’s booming demand for iron ore? The analysts at Goldman Sachs on Wednesday boosted their price outlook for iron ore, saying an unexpected rise in China’s use of the steel-making ingredient is compounding supply shortfalls. They raised their average 2019 price target to $91 a ton from $81, according to Bloomberg News’s Marvin G. Perez. “Chinese steel consumption has surprised to the upside,” the Goldman Sachs analysts wrote in a research note. Chinese steel production jumped 6.6% in 2018 and 10% in the first four months of this year, and Goldman upgraded its forecast for steel output in the nation from a contraction of 0.5% to a 4% expansion this year.

THE ONE DIP NOBODY’S BUYING

Already one of the two worst-performing currencies this year, Turkey’s lira took it on the chin again Wednesday, depreciating a world leading 0.86%. The weakness brought the lira’s decline this year to 13.4%, behind only the Argentine peso’s 16% slide. But here’s one dip that nobody wants to buy. It turns out that a barrage of interventionist policies by President Recep Tayyip Erdogan’s government has backfired, starving the economy of investment, fueling demand for foreign currency among households and businesses and further undermining the lira, according to Bloomberg News’s Cagan Koc and Constantine Courcoulas. Despite assurances that capital controls aren’t an option, Turkey has sought to stabilize its currency by reintroducing a tax on foreign-currency sellers and imposing a settlement delay for purchases by individuals of more than $100,000. “I can’t see any significant flows returning until policy makers become more market-friendly,” said Win Thin, global head of currency strategy at Brown Brothers Harriman & Co.

TEA LEAVES

The National Association of Realtors said Tuesday that existing home sales fell 0.4% in April, which was a mild shocker because the median estimate of economists surveyed by Bloomberg was for a 2.7% gain. Sales have now fallen in five of the past six months, and in 13 of the past 17 months. That qualifies as a slump. New home sales have held up better, rising in each of the first months of the year to about the highest since before the financial crisis. But April, it seems, was not kind to the real estate industry despite a big drop in mortgage rates. Economists forecast the government will say Thursday that new home sales dropped 2.5% in the month. The economy depends on a strong and healthy housing market, but if the real estate market is cooling off despite the decline in borrowing costs, it may force economists to ratchet down their 2019 growth forecasts.

DON’T MISS

U.S.-China Trade Clash Has Now Gone Global: Mohamed A. El-Erian

The Fed Is Likely to Make an ‘Insurance’ Rate Cut: Tim Duy

Trade-War Refugees May Find Emerging-Markets Haven: Nir Kaissar

Google ‘Minsky Moment’ Before Buying These Bonds: Shuli Ren

Why Silicon Valley Is Seeing Virtues of Nationalism: Conor Sen

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.