(Bloomberg Opinion) -- The prospect of leaving the European Union has forced Britain’s financial community to make expensive preparations for life outside of the trading bloc. Whatever happens on March 29 – a no-deal Brexit, a delay to the departure or some kind of agreement – the U.K. faces a slow but steady erosion to its position as the European center of looking after other people’s money.

London-based think tank New Financial said in a report published this week that it identified 269 U.K.-based financial firms that have reacted to Brexit by setting up new hubs, moving staff or rebasing assets elsewhere in the EU. The moves are real, not theoretical; the firms can’t afford to wait and see whether Brexit actually happens. “The days of `contingency planning’ are long gone,” as New Financial puts it.

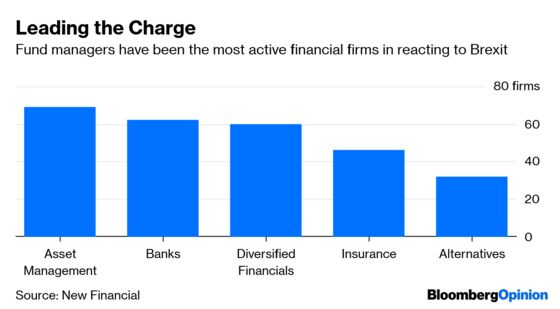

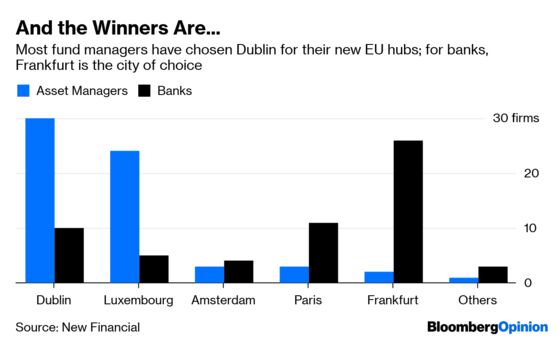

Asset managers have been the most proactive in establishing non-U.K. offices from which to do business, the report says. Moreover, the greatest number have chosen Dublin for their base in the bloc. Banks that have secured new EU licenses have overwhelmingly opted to locate their hubs in Frankfurt.

New Financial says that it identified 65 billion pounds ($85.2 billion) of portfolio funds that have been transferred out of the U.K. so far. But that’s based on publicly available information, which the think tank reckons underestimates the potential flows from the asset management community, as well as from banks. “We think the final numbers will be much larger,” the study says.

The European Securities Market Association and the Financial Conduct Authority have acted sensibly in minimizing the potential disturbance Brexit will cause and ensuring the continuation of so-called delegation rights that allow funds to be marketed and sold in one country and managed from another. Last month, EU and U.K. regulators agreed to two cooperation agreements to coordinate oversight of investment funds, in case Britain leaves the bloc without a deal.

But what the asset management industry has secured so far are “temporary fixes, not permanent solutions,” according to Sean Tuffy, the head of market and regulatory intelligence for Citigroup Inc. in Dublin. Most of the agreements have a two-year shelf life; the EU is likely to revisit how to create a third-country regime at its next review of regulations governing the sale and management of mutual funds across borders, which would threaten those delegation rights.

It’s not so much the jobs that move directly because of Brexit that will do the long-term damage to London’s role as Europe’s leading financial center. More important are the future roles that aren’t created in the U.K. that will slowly erode the capital’s status as other cities develop the pools of talent and the regulatory and legal architecture that the industry depends on.

And make no mistake: Dublin, Frankfurt, Paris and Luxembourg are keen to seize this one-time opportunity to win lucrative market share wherever they can. For example, London’s rivals are targeting the primacy of English law in financial contracts as a way of taking business away from the U.K., as my colleague Lionel Laurent detailed earlier this week.

Moreover, as the head of one of Britain’s largest asset managers told me last week, Brexit has forced the nation’s financial firms to spend money building new capabilities to create and distribute products from countries elsewhere in the EU. That’s a sunk cost, an expense that firms wouldn’t have undertaken if Brexit hadn’t forced them to shell out on new offices and alternative legal and regulatory arrangements.

So when decisions arise in the future about which location should create and market an investment product, that new infrastructure will compete directly with the existing setup at the U.K. head office for the new business and the associated headcount – and will win at least some of the time initially, and likely with increasing frequency over time. However Brexit plays out, the U.K. fund management industry will be a long-term loser from the fallout.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.