(Bloomberg Opinion) -- The U.K. Competition and Markets Authority has just published the results of its investigation into how company accounts are audited. Its proposals are an exercise in realpolitik that should succeed in improving the quality of scrutiny while acknowledging the conflict of interest posed by auditors being paid for more lucrative consultancy work.

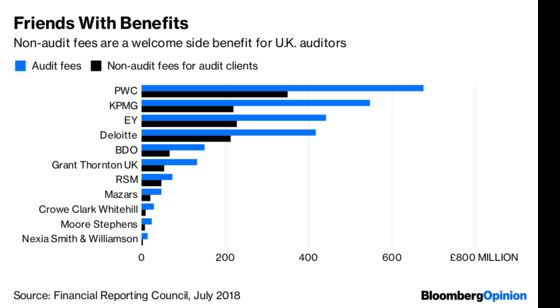

The issue is simple to elaborate but tricky to untangle. The so-called Big Four accountancy firms – PWC, KPMG, Ernst & Young, and Deloitte – audit 97 percent of the biggest U.K. companies. But at least 75 percent of their revenue comes from non-audit work, much of which is for the very same clients whose accounts they are responsible for scrutinizing.

The key remedy the CMA plans to impose is an operational split between audit and non-audit units. Rather than being paid out of the profits of the firm as a whole, auditors would be compensated only for their number crunching. That's a clever solution to reducing the temptation for an accountancy firm to go easy on its bookkeeping inspections to win other business from its clients.

The more radical step of forcing firms to separate their audit businesses from their consultancy work, as proposed by the opposition Labour Party, is almost certainly unworkable. Auditing is a low-margin business, and there's a risk that enforcing a bifurcation would reduce rather than enhance competition in the industry.

And there are the ancillary benefits from the two services sharing intelligence within a firm, something the CMA acknowledges would be lost by banning accountancy firms from doing consultancy work for the firms they audit.

The second key element of change is a requirement for the biggest 350 British companies to employ two auditors, one of which isn't a Big Four firm. It's less clear how successful this will be. The “cross-check on quality” the CMA envisages seems unlikely to happen, and the improved experience and credibility that the CMA says will accrue to the smaller accountants is nebulous at best.

The more damning element of the investigation comes in a separate report into the Financial Reporting Council by Sir John Kingman, chairman of Legal & General Group Plc. The picture he paints is of a cosy “trade association” masquerading as a regulator that “leaks and creaks, sometimes badly.”

Kingman has produced a laundry list of shortcomings, including a lack of engagement with the investment community that owns company shares, an absence of coordination with other regulators, and a “surprisingly, and inappropriately, informal” approach to recruiting board members. Only one of 21 vacancies between 2016 and 2018 was advertised nationally, and just six were filled by external recruitment consultants.

Funding the FRC through through a voluntary levy creates “a clear danger of blunting the FRC’s incentive to bite the hand that feeds,” the Kingman report says. His proposed solution is a new overseer funded by a mandatory contribution from the industry to pay for “staff of the caliber, expertise and seniority” to ensure the watchdog is “where necessary feared by those whom it regulates.” That has to be a more sensible approach than the current ramshackle set-up.

The short period allocated for the accounting profession to respond to the proposals – it has a bit more than a month to submit comments – suggests the CMA isn't expecting much pushback against its recommendations.

But the watchdog has also reserved the right to revisit what it deemed “drastic but harder to implement remedies” if the quality, transparency and reliability of company accounts doesn’t improve in the future. That will be comforting to investors who rely on auditors to make sure financial statements are accurate – and a potent threat that the Big Four should be wary of.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.