Two Billionaires Want to Restore the Glory of the U.S. Railroads

(Bloomberg Opinion) -- When American industrialist Henry Flagler decided to add Miami as a stop on his east coast Florida railway in the 1890s, the watery settlement had just a few hundred inhabitants. More than a century later, the city has flourished but the American public’s love affair with trains has soured. The country’s rail freight network is among the world’s best; its passenger rail services certainly aren’t.

Now, a couple of modern-day Flaglers — Wes Edens, co-founder of Fortress Investment Group LLC, and Virgin Group’s Richard Branson — aim to change that. They still need to persuade investors to come along for the ride.

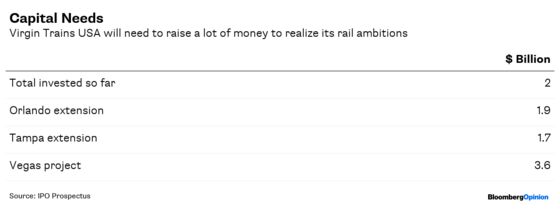

Virgin Trains USA LLC, operator of a new east coast Florida passenger express train, hopes to raise about $500 million in an initial public offering in coming weeks that would value the company at about $3 billion. Its line connecting Miami and West Palm Beach is the first major private intercity rail service built in more than a century (it was called Brightline until a recent rebranding). The company has already invested about $2 billion of debt and equity. Adding stops in Orlando and Tampa and funding a similar project connecting Las Vegas and southern California will require several billion more.

There was a time when raising that kind of money wouldn’t have been difficult. Modern equity markets were born out of the railroads’ need for capital. But today the economy is dominated by intangible technology assets that don’t need as much external funding. Equity markets have become a way to extract money from companies, rather than put it in, as economist John Kay has noted. So while railways are nothing new, Virgin Trains USA’s IPO pitch does feel refreshingly different.

Branson has lent the Virgin brand to the company in return for a fee and cross-selling opportunities and will take a modest equity stake. Perhaps his limited involvement is a good thing: Virgin’s rail track record in the U.K. is far from spotless. One of its services was re-nationalized last year. The Florida express train remains Edens’ pet project — he’s the chairman — and Fortress funds will still own a majority of it after the IPO.

One can only wish him well, even if this is a monumental challenge. Cheap gasoline and the interstate road system are all very well, but they’ve caused congestion, pollution, urban sprawl and many road deaths. In contrast, Florida railway passengers can sip champagne or beer and make use of the free Wi-Fi. Ticket prices are reasonable. Once constructed, the Miami to Orlando journey should be slightly more than three hours. In good traffic, driving takes a bit longer than that.

Edens’ idea to connect cities that are “too long to drive, too short to fly” also looks sensible. Federally subsidized Amtrak loses money, but its northeastern Washington-to-Boston route is profitable. The long-mooted Los Angeles to San Francisco high-speed train is expected to cost more than $75 billion and won’t open till 2033. But elsewhere, more modest ambitions have worked. Building on existing rail corridors where possible, and operating trains at slower speeds, has cut costs and overcome potential regulatory holdups in Florida.

Virgin’s sales pitch is still pretty racy, though, and I’m not sure whether all public market investors will have the stomach for it. Right now, the company burns through cash and may do so for a while. The Orlando connection should generate plenty of tourist traffic but it won’t be finished for three years. It’s reasonable to ask whether Americans can bear to leave their cars behind. In its present form, the Florida railway attracted just 239,000 passengers in the fourth quarter, a long way from the 9.5 million a year envisaged when the line’s complete.

The Fortress-owned parent has developed 1.5 million square feet of retail, residential and office space around the three existing Florida stations but unfortunately those assets aren’t part of the IPO. While there’s potential for other real-estate opportunities, for now the business depends on fares, food and drink, parking and sponsorship. After the IPO, it won’t be able to count on Fortress for financial handouts.

It’s also not clear on what terms it will be able to raise the extra $2.3 billion of debt needed for the next stage of expansion and whether the existing business can support that. The company already has $700 million of debt. Holdups are inevitable too in big infrastructure projects — the Miami station’s opening was delayed — and they tend to cause cash-flow problems. Just ask London’s Crossrail.

Indeed, the Virgin business had just $270,000 in unrestricted cash at the end of September, and its current liabilities were more than twice its current assets. It made an $87 million loss in the nine months to September on just $5 million of sales. In fairness, it was running a very limited service for most of that time, but the company’s five-year target of a combined $1.7 billion of yearly Florida and Las Vegas sales, and $1.2 billion of Ebitda, feels very ambitious. Construction on the Las Vegas railway hasn’t started yet, and Virgin still needs to acquire some land.

The risks aren’t just short-term, either. The prospectus notes ominously that Florida’s eastern seaboard is vulnerable to rising sea levels and the storms caused by climate change:

Any significant future rise in sea level near our Florida operations could result in flooding, which could damage our infrastructure, temporarily or permanently impair our ability to function near-coastal operations effectively, require us to incur costs to protect our assets or adversely impact our customer base.

It would be a bitter irony indeed if America’s first major private express railway in 100 years were sunk by the very vehicle emissions it should help curtail.

In 2017 Fortress sold Florida East Coast Railway Corp, which owns most of the railroad infrastructure, but Virgin Trains USA retains perpetual passenger rail use rights along the corridor.

The fourth and first quarters are expected to be the strongest due to the higher number of tourists visiting in those periods.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.