Twitter’s Recovery Looks Like the Real Thing

(Bloomberg Opinion) -- Last year, I wasn’t sure that Twitter Inc.’s recovery was real. Now, it looks as if it is.

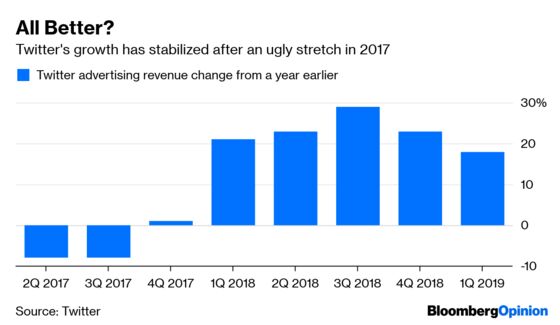

Twitter is not out of the woods, but it’s clear the company has stabilized financially after a long stretch of wobbles. Advertising sales rose 18 percent in the first quarter, the company reported on Tuesday. That was the fifth consecutive period of healthy gains. Twitter’s expenses have pulled back from its free-spending days, and the company now has genuine net income.

To be clear, Twitter still has a load of problems. Its base of users remains relatively small, and it’s not really growing. It may never. I’m still not confident that Chief Executive Officer Jack Dorsey — he of the dubious dietary habits and penchant for putting his hightop-clad foot in his mouth — is capable of making Twitter a responsible internet citizen.

Twitter will never be in the internet big leagues occupied by Facebook Inc. and Google, and everything could still fall apart. But being a healthy and growing business is a welcome condition for Twitter.

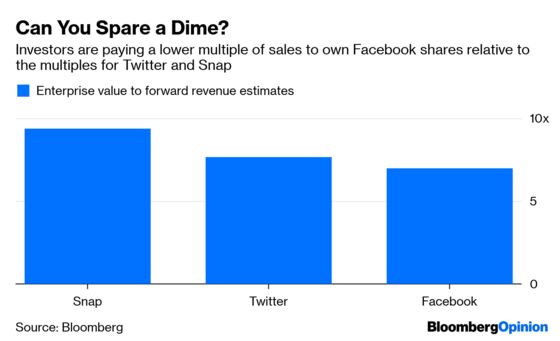

Investors, though, may be getting ahead of themselves. Twitter shares have already baked in the company’s recovery from what was a Superfund disaster zone for much of 2016 and 2017. Even before Tuesday’s 18 percent jump in Twitter’s share price, stock buyers were paying about 7 times estimated forward revenue for both Twitter and Facebook. For the moment, Twitter’s revenue multiple is higher than Facebook’s, which seems out of whack.

The two companies have always been compared with each other, by journalists, technologists and investors. Twitter has tended to chafe at the comparison, largely because it has long been in Facebook’s shadow and continues to be. For both Twitter and Snap Inc. — which also reports quarterly earnings on Tuesday — the Facebook yardstick is both a blessing and curse.

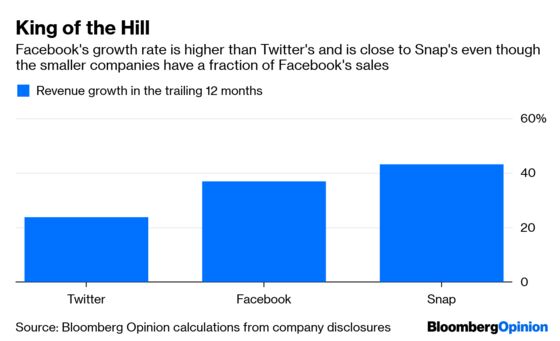

Consider Twitter. It has about 5 percent of Facebook’s annual revenue and yet Facebook — in the midst of an awkward business transition — is expected to grow faster than Twitter this year and next. Facebook’s operating margins are about 45 percent compared with Twitter’s 15 percent, and Twitter generates about two-thirds of Facebook’s average revenue from each daily user.

At Snap, its domestic revenue growth in the fourth quarter was slower than Facebook’s despite being a fraction of Facebook’s size. And the competitive pressure on Snapchat from Facebook-owned Instagram is well documented.

The young and promising Snap and a “fixed” Twitter still look meager compared with Facebook’s engine of growth and profits. That shows how remarkable Facebook is as a business despite — or possibly because of — its standing as the internet’s unholiest cesspool.

Does that mean we should pity Twitter and Snap for being constantly compared with the big bully of the internet? Nope. Yes, Facebook’s numbers make the two smaller companies look weak by comparison. But Facebook’s financial profile is also a blueprint for investors and advertising customers to gauge the upper limit for Twitter and particularly Snap, which remains immature both financially and in management expertise.

It must feel terrible for Twitter and Snap to constantly play little brother to an older, more successful and possibly unscrupulous relative. Investors should hope Twitter and Snap learn from the best of Facebook, without emulating the awful qualities.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.