(Bloomberg Opinion) -- The Turkish financial system appears to be returning to normal following last month's elections. This does not mean that international banks are ready to step back into the fray.

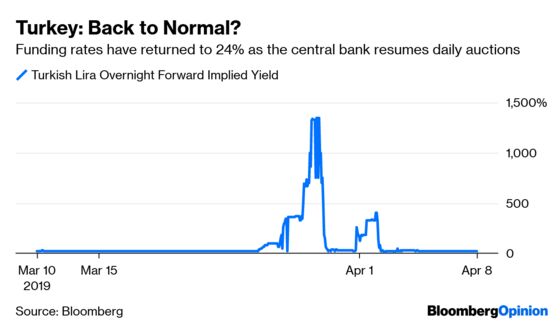

The central bank has resumed its daily auctions of one-week money at the standard 24 percent rate, and this is a welcome development. However, the lira fell more than one percent on Monday, as with the renewed ability to borrow comes the potential to short the currency again.

There’s still more to do. Full liquidity has not yet been restored, and it is still scarce for longer dates. That is a big problem coming in future.

But just as serious is the breakdown in trust between international banks and their Turkish counterparts. The failure of domestic lenders to provide liquidity or funding to foreign firms and their customers over recent weeks has created bad feelings that will take a long time to dissipate.

After an unexpected drop last month in official foreign currency reserves pummeled the lira, the central bank acted swiftly to support it by suspending its liquidity auctions. This caused a spike in short-term financing rates to as high as 1,300 percent, and all but closed the country's financial markets to foreigners.

The plunge in the lira last summer had already undermined the allure of Turkey for investors, and the recent crisis has made things worse. Foreign investors that had been trapped in the nation’s assets, unable to either buy or sell, may just liquidate their Turkish assets and retreat to other markets where they can be more certain they’ll get their capital back. They sold a net $602 million of Turkish equities in the week to March 29, the most in over a decade, and that is likely to worsen.

It’s hard to get a clear read on how Turkish banks have been affected by this shift in sentiment. For the past year, they’ve kept away from public markets. They rely heavily on international firms to provide much-needed dollar and euro liquidity, especially at longer maturities, and here the signs aren’t good. For a start, the number of banks participating in loans to domestic institutions has dropped.

One lender’s recent experience is worth noting. Akbank T.A.S. obtained a $900 million 367-day syndicated loan in March 2018 at a spread of 130 basis points more than Libor. However, it didn't refinance the full amount last month, and the yield premium it paid nearly doubled. Akbank's timing may prove fortunate as other banks may not receive much of an audience at all. It's an experience that may not encourage other banks to follow.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.