Turkey's in a Mess. Capital Controls Won't Help

What to do when your currency is in freefall? One simple answer is to slam on capital controls and hope it all goes away.

(Bloomberg Opinion) -- What to do when your currency is in freefall? One simple answer is to slam on capital controls and hope it all goes away.

There’s plenty of reason to think this strategy would appeal to Turkish President Recep Tayyip Erdogan. Given that he appears to have little interest in the rate increases that would stop the lira’s descent, some kind of capital control, such as a ban on converting it into foreign currency, might seem like a good solution.

And it might – if Turkey happened to be an insular, resource rich country whose economy is in dire need of protection. But Turkey is not one of these countries.

To be sure, Erdogan and Finance Minister Berat Albayrak, his son-in-law, seem to recognize this, and have recently ruled out applying capital controls or asking the International Monetary Fund for help. Erdogan also avoided them during the global financial crisis a decade ago – but the wise advisers he had then are no longer on the scene. Their absence is being felt. His demand for a boycott of U.S. electronic goods could provoke the Trump administration to retaliate in ways that further damage the Turkish economy.

Hence, emerging-markets investors and analysts such as Mark Mobius and AllianceBernstein continue to say capital controls could be on the menu of options to solve Turkey’s current crisis. There are two problems with this. They’d crush the economy, and they wouldn’t work.

Turkey has a lot of things going for it – a gross domestic product growth rate of 7.4 percent in in the first quarter, and pretty low public debt, at just 28 percent of GDP.

But its Achilles heel is the 6.3 percent current account deficit. Turkish non-financial companies' foreign currency liabilities were $337 billion as of the end of May, and were only partially offset by about $120 billion of assets, according to Bloomberg Intelligence. This $220 billion currency mismatch isn’t a problem, so long as foreign lenders are willing to keep funding it. That willingness looks fragile.

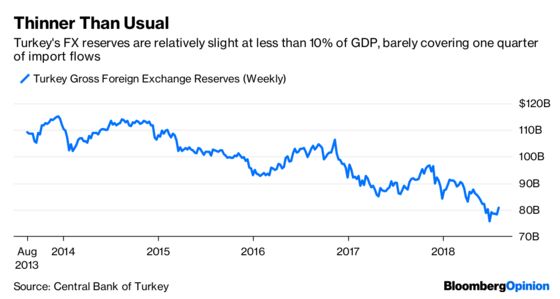

The country cannot rely on its foreign exchange reserves to shore up the currency – at $80 billion they’re an inadequate warchest, amounting to less than 10 percent of annual GDP.

Equally, with at least $20 billion of foreign currency debts coming due this year and next, a corporate or bank default is probably only a matter of time, despite the country's move on Tuesday to give lenders more flexibility. Such a crisis might be impossible to stop.

With trade flows, reserves and debts all relying on the faith of foreign creditors, it is understandable that investors fear a kneejerk response to shore up the currency might be taken.

The unintended consequences would be seismic.

Investors tend to value the return of their capital. Any sense the Turkish government will prevent the free flow of their financing will cause a stampede – and not just from foreigners, but from wealthy domestic players too. There are $159 billion of dollar deposits in the Turkish banking system, and Erdogan has already tried to encourage citizens to switch foreign currencies into lira. Forcing them would be a far graver matter.

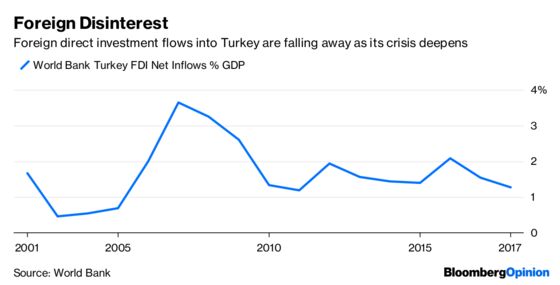

Slapping on capital controls usually goes hand-in-hand with reneging on foreign currency debt. This would provide some short-term solace. But it would also close off export markets for Turkish companies and destroy a banking system that has become reliant on foreign currency and swap lines. Foreign direct investment has been falling for a decade, but instead of reviving and becoming a major driver of growth in Turkey, it would be pretty much shut off for a generation.

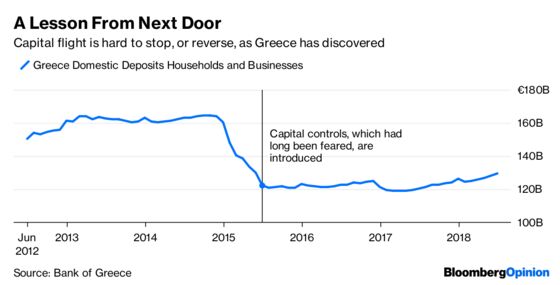

Turkey is an open trading nation that has infamously porous borders, so it is highly debatable how effective currency controls would be anyway. Capital controls only work when they can be rigidly enforced and the economy is somewhat self-supporting. Even so, the experience of countries that have tried this extreme route has been patchy at best – Greece, which is still recovering from the financial crisis, is a recent example. So, too, is Malaysia, which put them in place during the Asian financial crisis of the 1990s.

The solution lies within Erdogan’s control. His fierce rhetoric weakens the lira. It would help, too, if he undertook to restore orthodox economic policy by allowing the central bank to raise interest rates to control runaway inflation.

Turkey doesn’t need capital controls in the way that Malaysia or Greece did, and slapping them on would be a case of self-harm. The crisis plaguing the economy could be averted with a few small changes in policy – and one larger shift in tone.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.