(Bloomberg Opinion) -- Turkey’s central bank is again trying to shore up the lira. Its latest effort is unlikely to ease the pain for the worst-performing currency in emerging markets this quarter.

On Thursday, the monetary authority attempted to raise interest rates by the backdoor, suspending its one-week repo auctions and so making it costlier for commercial lenders to borrow money from the central bank.

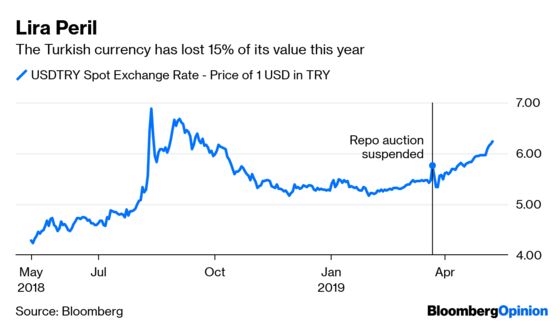

But traders who had been caught out when the bank tried the same maneuver just before the country’s March 31 municipal elections were this time prepared, and had largely covered their funding needs. This explains the lira’s muted gain on Thursday. By early afternoon, the currency had risen by only 0.8% against the dollar.

The daily auctions of one-week money are the central bank's main way of providing the financial system with liquidity. By stopping them, policymakers risk driving short-term borrowing costs skyward as banks race to secure funding.

That’s exactly what happened last month, when overnight rates soared to as much as 1,300% at one point. Then, the central bank was forced to resume the auctions to regain a semblance of order. Unless it does the same again by the end of next week, rates are almost certain to move inexorably higher again.

Jamming up the money markets is no way to revive confidence in a financial system already reeling from the country’s political turmoil. Inevitably, the main loser will be the currency, which will further undermine the allure of Turkey for investors.

In April, the impact on the currency was limited to a brief two-week rally – after which all the gains were unwound and more. This time is likely to be no different. Liquidity still hasn’t returned to Turkish markets. Investors are wary the government could, as it did last month, stop the country’s banks from offering any form of liquidity to non-domestic clients, effectively trapping foreign investors’ holdings.

If the central bank wants to make a real impact on the lira, it needs to raise its benchmark rate and show it is willing to tackle the country’s spiraling inflation. That looks unlikely, at least for now. Last month, the monetary policy committee removed a commitment to raise rates again from its statement. At an April 30 press conference, Governor Murat Cetinkaya was forced to insist another hike was still possible.

The currency’s subsequent weakening suggests investors take a different view. Until policymakers stop meddling in money markets and start raising benchmark rates, the lira looks set to return to the depths it plumbed during last year’s political crisis.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.