(Bloomberg Opinion) -- There are opportunistic financing deals, and then there’s Turkey. A $2 billion 10-year bond sale appeared out of nowhere for the country on Wednesday, with no roadshow and no prior announcement. But there was one big helping hand.

Saudi Arabia had just launched $7.5 billion of new 10- and 30-year notes and had elected for tighter pricing rather than raising a larger sum. This left a window for Turkey to present themselves to bond funds who were already looking at the Middle East, but who’d perhaps not been allocated enough from the heavily oversubscribed Saudi deal. Turkey’s timing was impeccable.

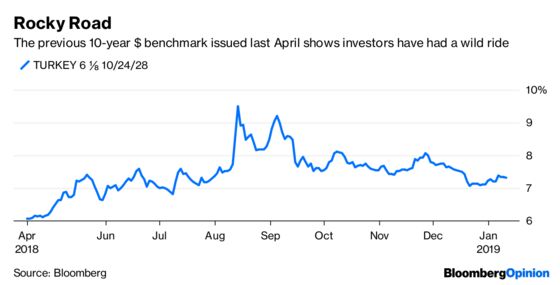

With a 7.625 percent coupon, its new 10-year paper looks generous to buyers on first glance, when you compare it to similar BB-rated sovereigns. But considering Turkey’s full-blown crisis in 2018, one might have expected it to be a lot higher. In the circumstances, it got this one one away easily and with a lower premium than you’d expect — even if there were a lot of Turkish buyers. Nearly 500 basis points over comparable 10-year U.S. Treasury debt may seem high, but credit spreads have widened everywhere recently.

The success of the Saudi sale, three months after the murder of columnist Jamal Khashoggi, showed how bond markets are happy to ignore the most unpleasant of political backdrops. But even if you set aside concerns about the administration of Recep Tayyip Erdogan, there are plenty of other things to worry about financially.

The country’s sovereign debt is respectably low at 30 percent of gross domestic product, and its currency has calmed down, but it is heading for an almost certain recession. Its corporate sector and banking system will bear the brunt of the government’s mismanagement of the economy. There’s still a danger that Erdogan pressurizes the central bank to cut rates before inflation, still running above 20 percent, has been properly curtailed.

So in the context of last year’s meltdown, which forced the central bank to raise domestic interest rates to 24 percent, being able to find funding at reasonable levels is quite an achievement. Turkey has $8 billion of external financing needs this year, so completing a quarter of that within the second week of the year is a good start. Given the financial risks for investors, you’d have to say its debt syndicate advisers have earned their fees.

That the sale was done in the dollar markets also tells a tale (Turkey immediately switched the proceeds back into euros). As Russia has shown, its not impossible for politically risky countries to sell euro-denominated bonds. But it’s much easier to do it in dollars, where there’s far greater liquidity. Moscow issued $4 billion in 10- and 30-year notes right at the height of the Skripal poisoning scandal. If capital market access is required, dollar bond funds will provide it.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.