Trump’s Trade War Has Cost Investors Up to $7 Trillion

(Bloomberg Opinion) -- If you thought President Donald Trump’s golf outings were expensive, wait until you see how much his trade war could cost investors and most likely already has.

A double dose of troubling trade news late last week sent stocks sliding on Friday. That brought the drop for the month to 6.6%, making it the worst May for the market since 2010 and the third worst if you go all the way back to early 1950s. And that’s saying a lot. May is, after all, according to the traders’ adage, the month where investors are supposed to go, and stay, away.

In the larger picture of the market of the Trump presidency, though, May’s drop doesn’t actually look so bad. Stock prices, as measured by the broad S&P 500 market index, are still up 27%, including nearly 10% in the first five months of this year. In fact, the S&P 500’s decline of 1.3% on Friday seemed kind of small in the wake of Trump’s demand that Mexico curb immigration or face 25% tariffs and China’s threat that it could essentially ban some U.S. companies from doing any business there. That’s led some to point to the market and make the case that a trade war with China and Mexico won’t be so bad.

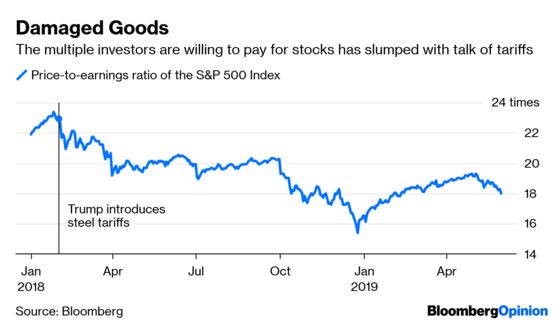

But that conclusion is short-sighted. The correct way to gauge how much economic damage the stock market thinks a trade war could inflict is to go back not a month but to when Trump really started talking tough on tariffs, first on steel and other metals, and then on China, in late January 2018. At that time, the Russell 3000, which captures more of the stock market than the S&P 500, was trading at a price-to-earnings multiple of 19.3 based on the next 12 months of earnings. At that point, analysts hadn’t fully factored into their estimates the corporate tax cut that had passed the month before. But by May, expected earnings for the Russell 3000 for 2019 had risen to nearly $103 a share. Based on those expected earnings, and if the index had maintained its pre-trade war fears multiple, the Russell 3000 would be at 1,986, with a market cap for all the stocks in the index of $36.2 trillion.

But that’s not what happened. Instead, earnings estimates for the next 12 months have come down to $98 a share, and the multiple has slumped to 16.6, giving the Russell — which is at 1,619 — a market capitalization of $29.5 trillion. It is impossible to know if that nearly $7 trillion difference can be attributed entirely to the trade war, and more than likely it cannot. Earnings estimates might have slumped anyway. Earlier this year, it looked as if interest rates were going to rise, which was also weighing on the stock market. Interest rates have instead dropped. And while the global economy has slowed, that could be trade-related as well. Bankim Chadha, the chief U.S. strategist at Deutsche Bank, put his estimate for the damage caused by the trade war at $5 trillion.

The market could also be overstating the potential damage from a trade war. The U.S. imports $550 billion in goods from China. A 25% tariff on those goods would raise prices by $138 billion. Mexico imports total an additional $400 billion, and a 25% tariff on those goods, which is how far Trump has said he would go to curb immigration, would equal another $90 billion, for a total of $228 billion. That is, of course, only the cost of higher goods to consumers and for only one year. Trade wars have far-reaching effects. But still, that’s a lot less than $5 trillion or $7 trillion. Nonetheless, the collective wisdom of investors has a better track record at predicting the future than most economists. And even if the true number is somewhere in between, Trump’s effort to reorient the U.S.’s place in world trade could end up being much more costly than most people think.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.