Trump's China Strategy Isn't Working

(Bloomberg Opinion) -- The Trump administration’s willingness to push the Chinese harder on trade has struck a bilateral chord. Beijing is listening. So far, so good. Now the question is what the U.S. wants to achieve. Answer: the total destruction of China as a competitor.

That isn't a trade goal, and the demands being made contradict one another. This aim also unnecessarily awakens Beijing’s deepest nationalist fears.

Unsure what to offer next – and convinced that the U.S. effectively persuaded Canada to take an executive at Huawei Technologies Co. hostage – China is falling back on familiar jingoistic strategies and rhetoric. Things are likely to get much worse from here.

Meanwhile, the U.S. economy is incurring pain that the Trump administration seeks to alleviate with a $12 billion bailout program to aid farmers. Pain may be worth enduring if something is being accomplished. But the only likely outcome is a reduction in trade and more expensive Chinese products. In other words, fat taxes on the American consumer.

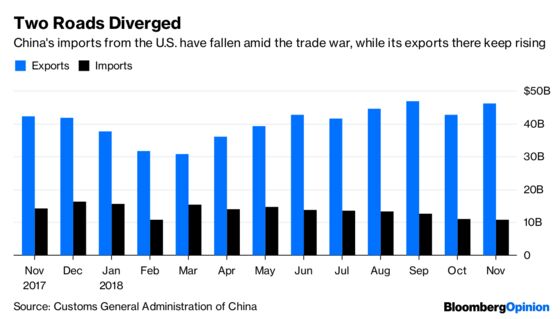

Over the past few months, Chinese imports from the U.S. have dropped sharply, declining 25 percent in November, even as its exports to the U.S. continued to rise. The big falloff started in July, after Washington implemented the first list of China-specific tariffs.

The majority of U.S. firms polled by the American Chamber of Commerce in Shanghai reported that the trade war has hurt their profits and that non-trade barriers have increased. The policies, if anything, have supported more offshoring: 31 percent of the respondents said they were looking to assemble or source components outside the U.S. There is no evidence that cybersecurity or intellectual-property protections have improved for U.S. companies.

That's a big turnaround in sentiment from years past. So why the change of heart?

China started its economic opening with an all-fronts offensive to charm foreign businesses. Politburo members were told to doff Mao suits and put on ties and jackets. Beijing and Shanghai built luxurious hotels at the end of highways that led straight from their airports: Foreign investors never needed to encounter the inconveniences of China proper.

By the 1990s, every third-string corporate delegation from the U.S. hoping to manufacture ball bearings or Barbie dolls in China was given an audience with the top political leadership, and those of us working there met constantly with government representatives. It's no wonder that American corporations believed the country was on a trajectory toward better market access, more transparency and fairer competition.

A key turning point came when China discovered public markets. The decade between 2000 and 2010 was a heyday for Chinese IPOs – especially for state-owned enterprises, for which public markets seemed like a bottomless and benevolent well of cash. After Hu Jintao assumed leadership in 2003, he dispensed with all the government meetings for foreigners.

Another decisive moment was 2008, when the nation’s measures to secure an optically triumphant Olympics established the machinery for tighter information control. That came in handy as the global financial crisis hit. With infrastructure stimulus appearing to rescue the economy, Beijing became convinced of the country's exceptionalism – a hubris that only affirmed the success of China’s authoritarian model, and led to a new era of assertiveness.

In this way, China lost the support of foreign businesspeople, who have become disillusioned with the market, tired of the pollution, and now fear for their physical safety. (The detention of three Canadians in retaliation for the Huawei arrest looks like pure thuggery.)

Initially, it was startling and encouraging that a U.S. administration was finally willing to call China’s bluff. Problems in bilateral trade genuinely run deep, and Beijing has a coordinated strategy of stealing U.S. technology and evading American export-control laws. Market access has in many ways deteriorated since the country joined the World Trade Organization in 2001 and made sweeping commitments to open up. The country subsidizes industries that then gain unfair advantages against competing foreign products.

But the Trump administration’s attempt to address these problems isn't working. Its trade positions conflict with one another, and despite various theories, no one is entirely sure who speaks for the U.S. President Donald Trump started off by demanding that China reduce its trade surplus with the U.S. by $200 billion and threatened a series of tariffs on its goods. The U.S. trade representative is pushing forward a Section 301 action to address intellectual-property theft, while also claiming to be working to encourage “reshoring” by U.S. firms. The Department of Defense is focused on cyber-strategy; the Department of Commerce on export controls; the FBI on non-traditional espionage. In other words, there is a litany of complaints whose basic target is the whole Chinese economic and political system.

Many of these goals are incompatible. Enforcing U.S. export controls will necessarily decrease its shipments to China and therefore increase the trade deficit. U.S. tariffs, and the inevitable retaliation, are a disincentive to reshoring, as they raise costs. Enforcing intellectual-property laws promotes import substitution. None of this is to say that the laws shouldn't be enforced; the administration just needs to be clear on its goals.

There are a few ways the U.S. could adopt a constructive approach without relinquishing (most of) its goals.

- Focus on intellectual-property theft: Drop demands about the trade deficit and firmly pursue IP enforcement and market-access demands. U.S. Trade Representative Robert Lighthizer is by far the most experienced and capable negotiator on the U.S. side. Treasury Secretary Steven Mnuchin, Commerce Secretary Wilbur Ross, and Trump should step out of the process.

- Go after China's red aristocracy: The high-alarm reaction to Huawei Chief Financial Officer Meng Wanzhou’s arrest is a clear sign that the country’s blooded elite are the third rail of diplomacy. A more active Treasury Department focus on Chinese money laundering; more stringent enforcement of export controls; and swift sanctions on the country’s sales to Iran and North Korea are important pressure points.

- Strengthen CFIUS: The U.S. needs to trade access to its own market for entry to China's, especially in financial services. More stringent investment reviews via the Committee on Foreign Investment in the U.S. can be used as leverage.

China’s political leadership rules at the pleasure of its military and security forces, a fact poorly appreciated in the U.S. Beijing's more regressive and nativist powers are held at bay when the country demonstrates strength, and even bellicosity. The Trump stance could easily trigger a backlash for which the U.S. is ill-prepared.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anne Stevenson-Yang is co-founder and research director of J Capital Research Ltd., a provider of investment advisory services.

©2019 Bloomberg L.P.