This Market Sweet Spot Is Shrinking Beneath Our Feet

(Bloomberg Opinion) -- For all the fears that the U.S. and China are unwinding the economic ties that drove decades of global prosperity, it's striking how much recent optimism depends upon the two countries.

Just months ago, all the talk was about recession, stocks were tanking and tariffs flew back and forth across the Pacific. Now the S&P 500 is reaching record highs, global growth outlooks have steadied and pessimism among manufacturers appears to be abating. Expectations for a worldwide economic recovery soared in November compared with the previous month, according to a survey of fund managers by Bank of America Corp. “The bulls are back,” its strategists wrote.

What changed? Two things. First, the world’s most important central bank delivered, and we’re starting to see the results. The Federal Reserve eased more aggressively than anyone dared hope at the dawn of 2019. Initially, there was some skepticism that Chairman Jerome Powell could pull off what he called a “mid-cycle adjustment” — that is, cutting rates enough to stave off the worst recession fears but not so much as to stoke asset bubbles. Yet markets appear satiated and U.S. employment, housing, retail and consumer-sentiment indicators have stabilized. All this was done against the backdrop of slow, steady easing in China, where the central bank started cutting reserve requirements well before the Fed moved, and trimmed borrowing costs further as the year wore on.

Another factor is the prospect of trade detente between Washington and Beijing. Officials say they are discussing a “phase one” deal that would have both sides making concessions on agriculture, intellectual property and technology. While few expect a comprehensive pact to cease economic hostilities, confidence that some kind of agreement will be reached underpins the mildly positive case for the economy. After all, few things are as important to global growth as how the world’s two biggest economies interact with each other.

To be sure, nobody is talking about a boom. Prospects for 2020 are looking decent because of reduced negatives rather than increased positives: Rates were too high and had been lifted too quickly, especially considering the fact that inflation hasn't come close to most major central banks’ 2% target. The Fed's key gauge of inflation rose a microscopic 1.3% in September, and China's factory-gate prices are falling, which exports lower prices to the rest of the world.

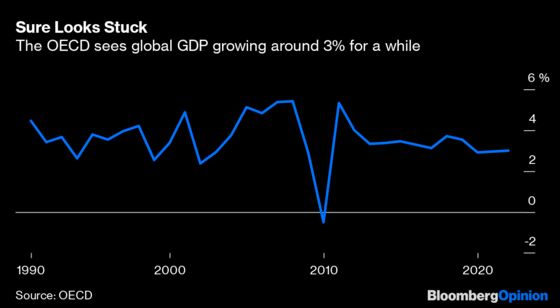

Unlike the synchronized upswing that characterized 2017, a sort of synchronized stability might best describe 2020. The Organization for Economic Cooperation and Development last week said global growth is stuck at 2.9% this year and next. The expansion will pick up to a hardly inspiring 3% in 2021. Recent market ebullience speaks to how desperate investors have become for not-utterly-terrible news.

Look closer, though, and this year’s rate cuts may not be as promising as investors hope. The Fed's moves reflected a deteriorating environment and manufacturing downturn as much as anemic inflation. The outlook could darken further, forcing Powell to cut again. Remember, a year ago the Fed was about to hike again and flagged multiple increases for 2019 — that didn’t last long.

China, meanwhile, hasn’t delivered as much easing as many market participants would like. The cut in the benchmark rate that some predicted earlier this year hasn’t arrived. Beijing seems intent on minding its own garden, keeping the expansion from slowing too much and watching leverage.

Trade optimists may be ripe for disappointment as well. Presidents Donald Trump and Xi Jinping came close to deal earlier in the year only to see relations sour and tariffs increase. China says it’s “cautiously optimistic,” but the lack of a deadline and Trump's predilection to blow up diplomacy on Twitter makes this a dicey bet. Not to mention the contours of any agreement could shift quickly as the 2020 election draws closer.

So let's keep the merriment in perspective. The global economy is still a shadow of its former self, and neither of its two main drivers look too sturdy. The optimism blessing the final months of this year mainly comes down to the fact that both China and the U.S. are trying to avert disaster. Those investors humming a digitally remastered version of “Happy Days are Here Again” may wind up whistling past the grave.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.