(Bloomberg Opinion) -- Thomas Cook Plc is on a trip it would rather forget.

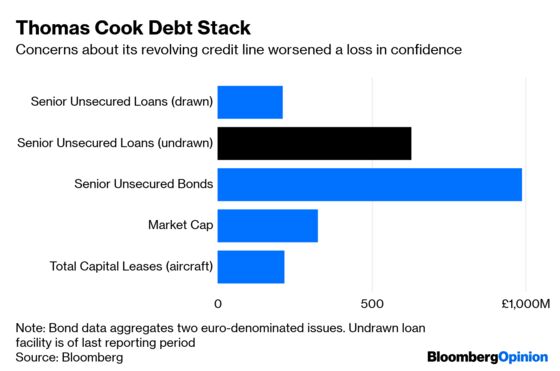

The company is battling a crisis of investor confidence. A rough 2018 for bookings hammered the share price and leverage has soared. At the latest seasonal peak, net debt of 1.6 billion pounds ($2.1 billion) dwarfed its market capitalization of 330 million pounds.

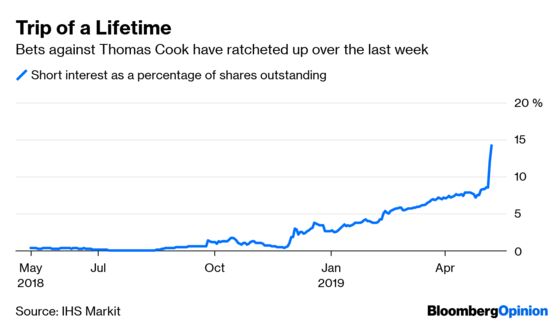

Sentiment worsened after reports on May 2 that some members of the syndicate of banks underwriting its working capital may have liquidated their exposure. This drove the value of the company’s 650 million-pound revolving-credit briefly below that of its two corporate bonds. It’s unusual for a credit line to trade; that Thomas Cook’s was marked at a discount to its more-liquid instruments points to a worrying loss of faith. Standard & Poor’s exacerbated matters by cutting its credit rating further into junk territory.

Restoring stability means ensuring financial flexibility. Thomas Cook needs to secure some near-term funding, sell its airline and have a decent summer season. If it can manage all of this, and show progress on tackling its longer-term obligations, a return to normal may be possible.

The company said last week it was in talks with its banks to arrange funding to see it through the difficult winter period, when suppliers have been paid for the previous summer’s holidays but payments for next year’s vacations haven’t arrived. Sky News reported it was seeking up to 400 million pounds, and new facilities may be announced when officials present interim results next week.

A new loan makes Thomas Cook less of a distressed seller when it comes to the airline. There are a wide range of estimates of the unit’s value – analyst James Ainley at Citigroup puts the enterprise value of the division at 640 million pounds. Although the timing is good since demand for planes has been bolstered by the grounding of Boeing Co.’s 737 Max jets, and the company’s airport slots have value, a disposal may not be straightforward.

Deutsche Lufthansa AG has tabled a bid for Condor, the German arm of the division. This could leave the U.K. unit still in need of a buyer. However, the field of bidders will be limited by European Union rules requiring airlines to be majority-owned by European investors.

Another hurdle is that the the average age of the fleet is 15 years, according to analysts at Citigroup and Ascend. Those planes would need to be replaced not long after they’d been purchased, so any buyer would need to make a significant investment.

These difficulties mean the pressure is on for Thomas Cook to have a better summer season than it did last year. The outlook isn’t great, given the continuing uncertainty over Brexit.

An extra round of funding should offset worries about poor sales. But even if this is achieved, and even if the airline gets sold, for investors and customers to be reassured Thomas Cook needs to find a longer-term solution to its borrowing burden.

That’s possible but not guaranteed. There’s logic to distressed debt investors taking a position now so they can have an advantage in any possible restructuring. This could explain the recent interest in the revolving credit line.

With all this drama, it’s easy to forget that the company has some attractive assets. The tour operator has a strong brand and a distribution network, which could be a useful addition to a big hotel group or online booking service. Citigroup puts the enterprise value of this division at 534 million pounds.

The wild card is Fosun International Ltd., which has been increasing its stake in in the group. If the airline is sold, that may pave the way for it to take control of the tour operator.

That’s another reason for Thomas Cook to get moving toward a solution, and bid farewell to its current ugly holiday spot.

--With assistance from Chris Bryant.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.