(Bloomberg Opinion) -- The global iron ore market is quivering in the shadow of a mountain of rust building up in China. Investors should put that in a bit of perspective.

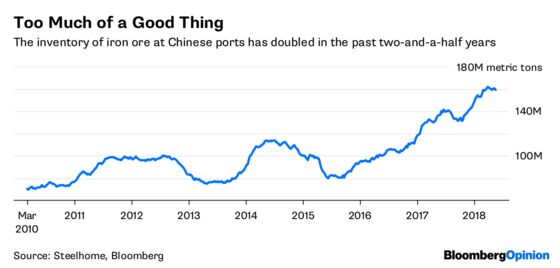

Since the end of 2015, the inventory of iron ore at Chinese ports and tracked by consultancy Shanghai Steelhome Information Technology Co. has roughly doubled, from 80 million metric tons to about 160 million tons. Even compared to the period in 2011 and 2012 when the market was running red-hot, the stockpile is up by 50 percent or so.

That looks like bad news for the state of Chinese steel production and ore demand: If all that ore is sitting around unused, surely consumption at steel mills must be headed for a fall?

Start breaking down what’s actually in those piles of oxidized iron, though, and the numbers look much more manageable.

First of all, you need to compare the absolute volumes to the amount being imported. Chinese iron-ore imports have risen by almost half over the past five years. If the nation’s steel industry consistently stockpiles about 0.5 percent of imports, the quantity left in inventories will increase by an equivalent amount.

Sure enough, if you compare the monthly change in iron-ore stockpiles to the volumes imported, you end up with a chart that’s nearly flat:

Nearly, but not quite. The period up to mid-2015 showed regular interludes where inventories fell, with a tendency toward destocking in some years and only gradual restocking in others. Since then, there’s been a more consistent build: In 2016, on average about 0.2 percent of imports were diverted into stockpiles, rising to 0.3 percent in 2017 and 0.5 percent so far this year.

That suggests there’s something else going on.

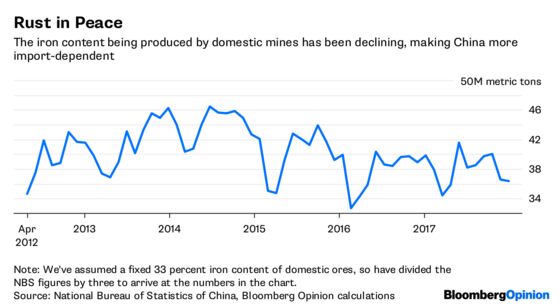

One factor is probably China’s growing import-dependence. Ore imports aren’t just going up because China’s producing more steel: They’re rising because it’s producing less iron ore as well. Assuming that domestic ore grades are unchanged, there’s about six million tons a month less elemental iron being produced from local pits relative to where we were in 2015, suggesting that around 10 million tons of the import total is needed just to supplement declining Chinese output.

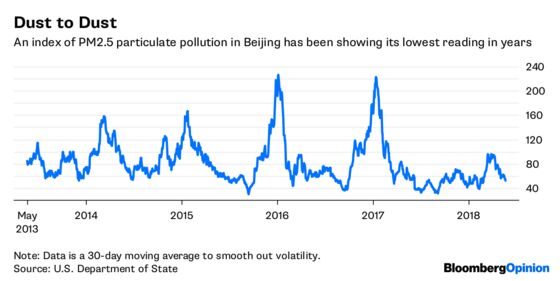

Another factor is pollution. Beijing sits in the middle of the country’s metal belt, concentrated on the province of Hebei that encircles the capital and produces about a quarter of the country’s crude steel.

The winter just ended has been the first in many that didn’t see a dramatic spike in Beijing’s particulate pollution. Part of that is the general decline in industrial activity to meet government anti-pollution mandates – but there’s another way that it’s affected stockpiles, according to Lachlan Shaw, a Melbourne-based commodities strategist at UBS Group AG.

Stockpiled iron-ore imports are mostly a gritty material known as fines. Iron ore producers spend considerable sums spraying these with water and other additives to stop them being converted into inhalable dust, and Chinese steel mills faced by tightening pollution rules have a similar problem. One solution is to concentrate inventory in the small number of port stockyards, rather than the myriad mills scattered throughout the country.

Blending of different grades of ore to produce the right mixes to feed into blast furnaces – another messy, polluting activity – is likewise moving toward ports, where the greater volumes being processed allow particulates to be controlled more consistently.

Put together, those factors probably account for about 30 million tons to 40 million tons of the 160 million ton port inventory, according to Shaw – enough, when combined with the change in volumes, to make the mountain all but go away.

There’s a further issue to consider, too.

China’s Dalian Commodity Exchange earlier this month opened its iron ore contract to international investors. The contract is a physically delivered one, meaning that a trader with a 10,000-ton long position needs to be able to actually receive that amount of ore somewhere if they’re still holding the contract at the end of the month.

That means rising open interest in futures contracts should put upward pressure on port stockpiles. Assuming more international traders start participating in the market, the ability to fulfil contracts and keep trading will depend increasingly on the availability of deliverable ore in bonded warehouses connected to the Dalian exchange. Ensuring liquidity in the futures market will require a pile of ore separate from the existing iron mountains that steel mills use to manage their own needs.

There are reasons to fret about the future of iron ore prices. (Will Vale SA flood the market? Will China’s credit-fueled construction boom grind to a halt?) But ore stockpiling isn’t one of them. From the right angle, this mountain looks more like a molehill.

To contact the editor responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net

©2018 Bloomberg L.P.