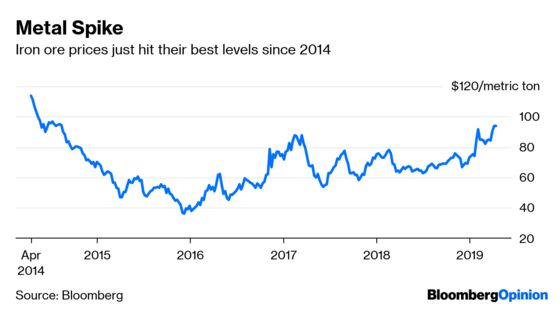

(Bloomberg Opinion) -- Iron ore’s glory days seem to be back.

Singapore-traded rust climbed to its highest level since 2014 as it hit $93.83 a metric ton Friday, while port inventories in China suffered their sharpest weekly decline since 2015 – a typically bullish sign.

Prices will rise further thanks to mine closures following a January tailings dam disaster in Brazil and Chinese steel mills don’t realize how tight ore supply could get, Shanghai Steelhome Information Technology Co. founder Wu Wenzhang told Bloomberg News in an interview. Rio Tinto Group on Tuesday likewise reported output will fall short of previous forecasts.

With credit conditions sharply easing and fueling fresh economic stimulus, that’s reason to believe the picture for the rest of the year will be bright.

For one thing, prices for cement – an early-stage building material that can be used as a forward indicator for other construction goods such as steel – hit their highest level in at least four years in December. At 446.5 yuan a metric ton, medium-grade cement is now double what it cost three years ago, on the eve of the current building boom.

The floor space of apartment buildings under construction is similarly increasing at its fastest pace in more than four years, with an 8.3 percent rebound from a year earlier in February. In Beijing, Tianjin and the eastern provinces of Shandong, Zhejiang, Fujian and Guangdong, real estate fixed-asset investment is rising at double-digit rates, more than enough to offset signs of weakness in neighboring Shanghai, Jiangsu and Hebei.

While those numbers indicate strength, there’s still some cause for doubt, though.

Parts of the property market are still looking dicey. In China’s biggest and wealthiest coastal cities, real estate prices are hardly increasing for pre-owned homes. In the prime first-tier cities they were up just 0.3 percent from a year earlier in February, with prices falling in Beijing and Shanghai. While new homes in second-tier cities and first-tier Guangzhou have seen double-digit growth rates, even Shenzhen seems to have lost some of its sheen:

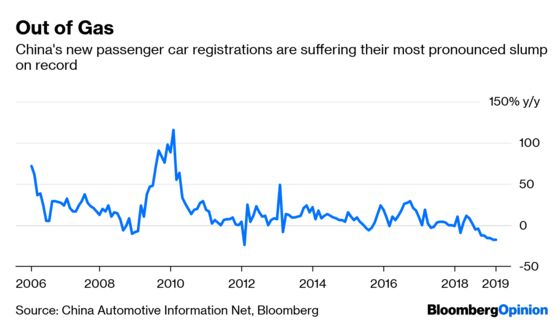

The auto industry, another big consumer, is even frailer. Monthly car sales fell more than 17 percent from a year earlier in February, continuing the worst performance on record barring a one-month blip around Lunar New Year in 2012:

The weakness also appears to be showing up in futures markets. Typically, near-term deliveries of steel reinforcement bar and hot-rolled coil cost several hundred yuan a ton more than longer-dated supplies, as builders and manufacturers try to get their hands on product as soon as they can. These premiums have been narrowing: The spread between front-month and three-month coil almost disappeared earlier this month, and gaps are sharply narrowing for rebar, too:

No wonder many observers are still painting a dismal picture of output this year. Steel production will fall about 2.5 percent to 900 million metric tons in 2019, Mu Wenxin, an analyst at Jiangsu Yonggang Group Co., told a coal industry conference in Shanghai last week. That would represent only the second decline in recent decades, following China’s last brush with aggressive deleveraging in 2015.

Yet all those indicators, barring Jiangsu Yonggang’s forecast, are backward-looking. The more telling hints will come from the stimulus currently working its way through the system. With aggregate financing coming in more than 50 percent above estimates at 2.86 trillion yuan ($426.5 billion) in March, it’s hard to believe the rest of the year won’t prove stronger than currently expected.

Another 2016-style building boom doesn’t look a lot like the consumer-focused, small-scale stimulus that China has been promising, but it seems to be the one we’re getting. The government is facing a range of good and bad anniversaries this year, from the founding of the People’s Republic and the Chinese Communist Party to the Tiananmen Square protests. The temptation to juice the economy to ride out those events will be hard to resist.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.