(Bloomberg Opinion) -- In a luxury market as fickle as the latest handbag trend, Richemont has added to nervousness about the Chinese consumer.

It wasn’t just that the owner of Cartier and Chloe suffered a sharp slowdown in underlying sales in September. The company didn’t report the actual figure alongside its first half report on Friday, but analysts at Morgan Stanley estimated it had virtually no growth that month, compared with a 10 percent gain from April to the end of August.

Richemont also warned that 18 months of elevated demand in China, which had boosted sales growth to a percentage in the double digits, had decelerated to a more normal level: a figure in the high single digits. Meanwhile, a trade war that hurt the country's currency could inflict further damage.

The shares fell as much as 6.9 percent, the most in three years, and dragged down the broader luxury market with it.

As I have argued, investors are right to be cautious about a slowdown in China, and the company seems to be confirming that the turbo-charged buying there over the past two years or so is running out of steam. Nevertheless, Richemont's punishment looks severe.

Some of the factors that hurt sales in September were one-time hits, such as typhoons that shut stores in Hong Kong and discouraged tourism, and an adverse impact from foreign exchange. October sales excluding currency movements and the online businesses have now recovered to around the 8 percent pace seen in the first half of the year.

What's more, some of the pain in watches is self-inflicted. Richemont has been buying back unsold stock from third party retailers for the past few years, and is still reducing the models it sends into the market.

It wants to get to a position where its supply is in line with the watches being sold, and ideally is just below that level, so that there is a slight shortfall to boost desirability. It’s a sensible strategy, but one that can be painful to execute.

Richemont is also building a powerful online operation. Sales made via the internet accounted for 14 percent of the total in the first half, which is promising given that online is expected to become a much bigger part of the luxury market over the next decade.

Although costs related to the acquisitions of the shares in Yoox Net-A-Porter Group it didn’t already own and the whole of Watchfinder took their toll on first-half operating profit, they have the potential to increase sales and profits going forward.

And while delivering to top-end shoppers produces lower margins than Richemont achieves in its traditional luxury divisions, the scope to eventually bypass wholesalers, and sell more watches directly to consumers via these online channels, could bolster profitability over the long-term.

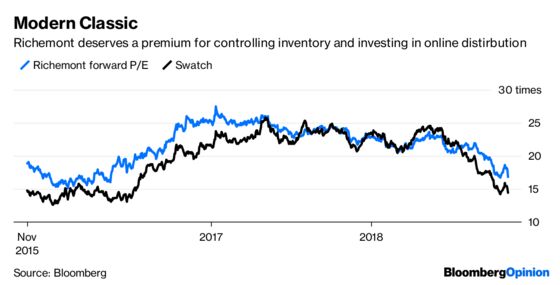

With Friday's fall, shares in Richemont are down 30 percent from their 2018 high in May. They trade on a forward price earnings ratio of just under 17 times, a deserved premium to Swatch's 14.5 times.

Richemont, like the other luxury brands, is exposed to the vagaries of Chinese demand.

But its strong jewelry labels, together with the actions it has taken to control watch supply and the strong foundation it is building online, offer some useful defenses. Investors should hold their nerve.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2018 Bloomberg L.P.