The Stock Market Can Be a Humbling Place

A week of disappointments leads market commentary. Plus, smart-money signals, a default jaw-dropper and more.

(Bloomberg Opinion) -- It was only last week that the S&P 500 Index was near its highest levels since July after recovering from its August sell-off. The thinking was that better-than-forecast data on housing, factory orders and industrial production meant talk of a looming recession was overdone. This week showed that those signs of resilience may have been little more than a mirage.

On Thursday, two days after a factory index from the Institute for Supply Management indicated a deepening contraction for manufacturing, the group said its services gauge for September fell to its lowest level since August 2016, well below the most pessimistic forecast in a Bloomberg survey. While the S&P 500 did erase an intraday decline of as much as 1.1% to end the day up 0.80% in its biggest gain since Sept. 5, there’s a simple explanation. In short, it’s a sign that investors expect the Federal Reserve may get more aggressive in its response to the slowdown (also note, the market is still down for the week). As FTN Financial economist Chris Low figures, the Fed will look at this week’s data, especially those that suggest the consumer is losing strength, and figure that it has no choice but to finally get ahead of the problem with a powerful policy response that may mean a 50-basis-point cut in interest rates later this month. After all, equities fell after the Fed cut rates only by 25 basis points in July 31 and Sept. 18. “The Fed missed their September opportunity, but it is not necessarily too late to act forcefully in October,” Low wrote in a note to clients Thursday. “Keep kicking the can with timid policy responses for too long, however, and there will be a recession.” To be sure, even if the Fed decided to go that route and cut rates by 50 basis points, it would need to do so in a manner that calmed rather than spooked markets.

“The Fed is walking a delicate line now,” Low added. “On one side, they do not want to risk sparking fear by talking up economic risks and acting precipitously. On the other hand, they risk further undermining confidence if they appear oblivious of risks and fail to act aggressively enough. It’s a tough line to walk, but some reassurance the Fed cares enough to act forcefully would be welcome now.”

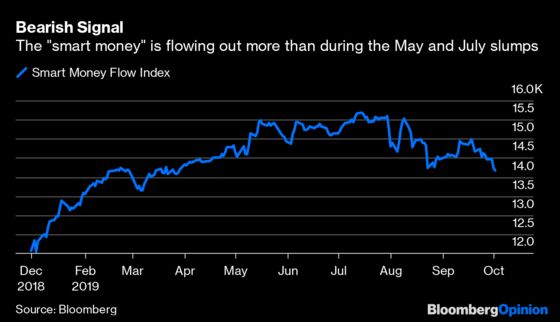

THE SMART MONEY WANTS TO STAY THAT WAY

In terms of magnitude, the 3.56% drop in the S&P 500 from last month’s high on Sept. 12 isn’t alarming. It’s milder than the two previous prolonged declines this year that raised alarm bells: the 6% slump between July 26 and Aug. 5, and the 6.83% tumble between May 3 and June 3. What’s different this time is that the so-called smart money isn’t as confident that equities will bounce back. That can be seen in the Smart Money Flow Index, which tracks action in the Dow Jones Industrial Average during the first half hour of trading and the last hour. The idea is that trading in the first 30 minutes represents emotional buying, driven by greed and fear of the crowd based on good and bad news, as well as a lot of buying on market orders and short-covering. The “smart money,” though, waits until the end of trading to place big bets, when there is less “noise.” That index on Wednesday dropped to its lowest since March, a sign of caution. “Stock investors don’t like that the doom and gloom in the manufacturing sector is starting to infect the bigger part of the economy that employs millions of workers in services industries including health care, retailing, business administration, accounting, computer services on and on,” said Chris Rupkey, the chief financial economist at MUFG Union Bank.

WHY ARE BANKS SO JITTERY?

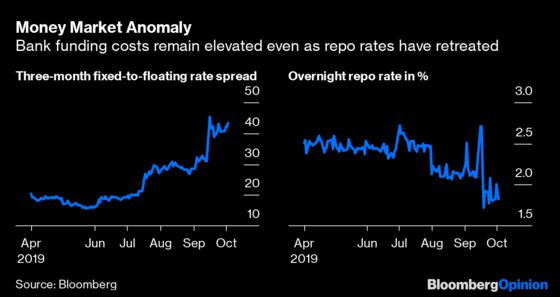

The CBOE Volatility Index, commonly known as the “VIX,” is nicknamed “the fear gauge.” The measure tracks implied volatility in the stock market, and the higher it goes, the more “fear” there is perceived to be among investors. But there are many other “fear” gauges in markets, and one that looks particularly troubling right now is overnight bank funding costs. Those have been slowly rising from a recent low of 15.6 basis points in May, but spiked higher to 45.2 basis points in mid-September during the turmoil in the repo, or repurchase agreement, market. That put them at about the highest since the European sovereign debt crisis in 2011 and 2012. The initial speculation was that the jump higher in bank funding costs was related to what was happening in the repo market. But repo rates have since come back down, and yet bank funding costs have remained elevated. On the face of it, this suggests banks, which have more insight into the economy and financial system than any other sector, are more wary of lending to each other. Nobody is predicting a banking crisis, but with the Fed likely to continue cutting rates and the economy slowing, it’s clear that the outlook for the industry isn’t getting any brighter. On Thursday, the analysts at Keefe, Bruyette & Woods Inc., which specializes in financial firms, lowered their earnings-per-share estimates for Citigroup Inc., Goldman Sachs Group Inc., JPMorgan Chase & Co., Morgan Stanley and Wells Fargo & Co.

S&P MAKES SHOCKING FORECAST

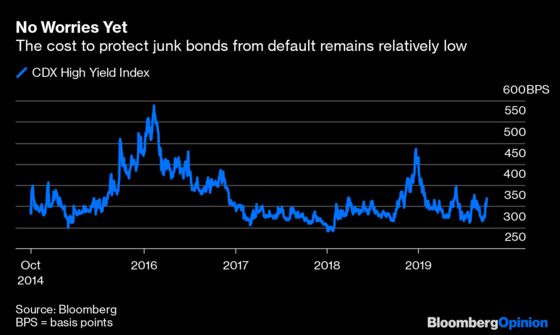

In his 1926 novel “The Sun Also Rises,” author Ernest Hemingway wrote an exchange between two characters, with the first asking, “How did you go bankrupt?” The second character answers, “Gradually and then suddenly.” The same scenario may be about to play out in the corporate bond market. Thanks to the easy-money polices of central banks, corporate default rates have been well contained since the financial crisis. But that may be changing in a rather sudden manner. S&P Global Ratings said in a report Thursday that it currently forecast the speculative-grade default rate will rise to 3.4% by mid-2020 from about 3% currently. That certainly would be manageable. But S&P says it may then spike to 10% or higher by late 2020 through 2022. “Past the first half of 2020, growing risks are laying the groundwork for a greater potential uptick,” the ratings firm wrote in the report. “The credit deterioration and corresponding debt buildup of recent years have been made possible by an extended period of ultra-low borrowing costs for corporations. However, the current favorable credit cycle is showing signs of age and may have already turned.” The potential for a spike in defaults among high yield issuers to pose a systemic risk has never been higher. The Bloomberg Barclays U.S. Corporate High Yield Bond Index currently tracks $1.24 trillion of junk bonds, more than double from before the financial crisis. That’s not including the $1.2 trillion of leveraged loans outstanding.

NICKEL MARKET GETS A JOLT

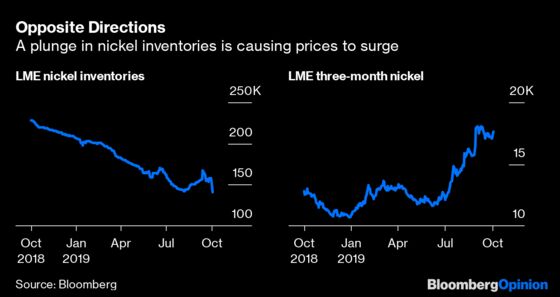

As an economic indicator, nickel doesn’t have the same reputation as copper, which has widespread industrial and consumer applications. Nevertheless, the metal is still a fairly integral part of the global economy, used mostly in producing stainless steel. It is also plays a key role in the production of batteries. So the decision by Indonesia to ban nickel-ore exports starting in 2020 is worth watching to see how it ripples not only through the commodities market, but also through the global manufacturing sector, squeezing margins in a slowing economy as prices jump. Already, inventories tracked by the London Metal Exchange have plunged, falling by a record on a tonnage basis Thursday to a six-year low as traders scrambled for material before the ban goes into effect, according to Mark Burton. Prices, meanwhile, have spiked, and forward spreads indicate buyers on the exchange are close to facing the biggest squeeze in more than a decade. Nickel prices jumped 0.8% Thursday to settle at $17,625 a ton in London. Prices are now up 65% this year, on course for the biggest gain since 2006. “The whole nickel market is tightening,” Xiao Fu, head of commodities research at BOCI Global Commodities, told Bloomberg News. “Even with all the macro headwinds and demand worries, any supply-side shocks can still support a strong rally when stocks are low.”

TEA LEAVES

Not only did the overall ISM non-manufacturing index come in weaker than forecast, but the component tracking employment fell to its lowest since 2014. Naturally, that raised a lot of questions about the monthly U.S. jobs report due to be released Friday. The report was not expected to be great, with the median estimate of economist surveyed by Bloomberg calling for an increase of 145,000 jobs in September, below the monthly average of 207,000 over the past five years. But following the poor ISM services index, as well as the equally disappointing ISM manufacturing report on Tuesday, the betting is that the number of jobs created will fall below expectations. The so-called whisper number is for a gain of 125,000 jobs, according to data compiled by Bloomberg. That has dropped from about 140,000 jobs being whispered about at the start of the month. Even if the headline number comes in fairly strong relative to expectations, it still pays to dig in to the reports details. That’s because employers rarely trim their work forces at the first sign of trouble. Instead, they cut back on hours and raises. Economists are expecting average weekly hours worked to come in flat at 34.4, and for hourly earnings to increase 0.3% after a gain of 0.4% in August.

DON’T MISS

Stock Markets Have Long Tails and Tiny Brains: John Authers

China Won't Save the World Economy This Time: Daniel Moss

Confessions of a Reformed Cryptocurrency Doubter: Jared Dillian

Socialism Can Work if It's Done Properly: Ferdinando Giugliano

Schwab’s Next Target? Your Financial Adviser: Nir Kaissar

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.