The Stock Market Bandwagon Is Filling Up Quickly

(Bloomberg Opinion) -- The U.S. stock market as measured by the MSCI USA Index just posted its best two-day performance since February, rising 1.58 percent Tuesday and 1.13 percent Wednesday. What’s notable is that the gains, in the wake of a nasty sell-off that left equities on the cusp of a correction, aren’t coming with the usual caution from prominent Wall Street strategists about “dead cat bounces.” Instead, they are expressing a remarkable sense of enthusiasm.

First, JPMorgan Chase & Co.’s all-world analyst Marko “Gandalf” Kolanovic issued a report Tuesday talking up the possibility that the October “rolling bear market” turns into a “rolling squeeze higher” into the end of the year. Then on Wednesday, Fundstrat Global Advisors’ Tom Lee — another analyst known for making exceptionally timely calls — went even further. He wrote in a research note that “the potential for a violent upside rally is substantial.” While a big part of Kolanovic’s thesis focused on fundamentals such as a likely surge in stock buybacks by companies, Lee honed in on the technicals. The percentage of stocks in the S&P 500 and Russell 2000 that are above their 50- and 200-day moving averages is “unusually low,” and that has often signaled a bottom when it has happened outside of a bear market but in a correction, reports Bloomberg News’s Kriti Gupta. As Lee points out, returns over the following three and six months — when the markets have become as “oversold” as they are now — have averaged 13 percent and 19 percent, with positive gains in eight of nine cases. Cynics might say that now would be the perfect time to sell given such unbridled optimism among strategists.

But there are signs that all those who wanted to sell have already done so. State Street Global Markets came out Wednesday with its monthly index of global institutional investor confidence. The measure has some authority because unlike survey-based gauges, it uses actual trades and covers 15 percent of the world’s tradeable assets. For October, the index dropped to 84.4, the lowest in almost six years. The index has been this low in only two other periods in the history of the series going back to 1998 — late 2012 and late 2008, and each time stocks went on to rally. Who wants to play those odds?

CHINA TO THE RESCUE. MAYBE.

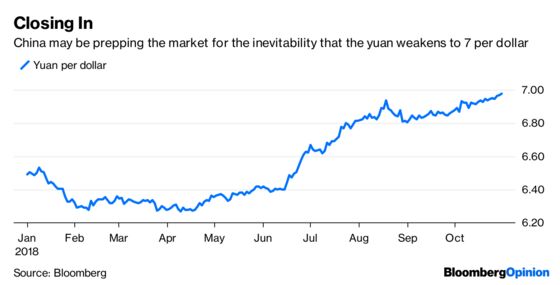

I would be remiss to talk about the good feelings that have suddenly permeated equities markets not only in the U.S. but globally without mentioning China’s role. As the world’s second-largest economy, significant fiscal and monetary announcements there tend to ripple through global markets. There have been countless times in the past few years when China’s stock and bond markets looked to be in freefall only for the authorities to announce plans to stimulate the economy, bolstering risk assets worldwide. Well, it just so happens that on Wednesday a statement from a Politburo meeting chaired by President Xi Jinping said that the nation’s economic situation is changing, that downward pressure is increasing, and that the government needs to take timely steps to counter all this. “In recent years the balancing act has been addressing risks in the financial system against pressure to stabilize economic growth,” Katrina Ell, an economist at Moody’s Analytics in Sydney, told Bloomberg News. “It appears the latter is again more of a priority.” The statement could also be a signal that China’s leaders are trying to soften the blow if, or more like when, the yuan weakens to the widely watched 7 per dollar level. The yuan was at 6.9757 per dollar Wednesday, steadily depreciating from 6.2690 in April amid an escalating trade war with the U.S. Some market participants worry that if the yuan does weaken beyond 7 per dollar, it could spark a flight of capital that causes the yuan to fall even more and turn into a full-blown currency crisis that officials can’t contain and infects global assets.

DEBT’S ‘THREAT TO SOCIETY’

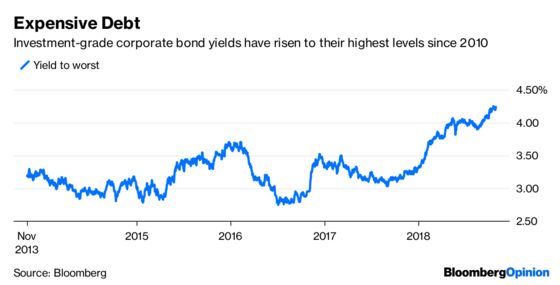

Perhaps the equity bulls wouldn’t be so, well, bullish if they looked at the deteriorating U.S. debt situation. The Treasury Department on Wednesday announced planned debt sales that will surpass levels last seen when the country was digging out of its worst economic crisis since the Great Depression, according to Bloomberg News’s Saleha Mohsin and Liz Capo McCormick. A ballooning budget deficit — fueled by tax cuts, spending hikes and an aging population — is driving the Treasury to raise its long-term debt issuance at its quarterly refunding auctions to $83 billion from $78 billion three months ago. Already, total marketable U.S. government debt stands at $15.3 trillion, up from $13.9 trillion when Donald Trump took office in January 2017. The debt situation has become so bad that even a prominent Trump administration official on Wednesday called it a “threat to the society” that requires significant cuts to the government’s discretionary spending. That’s not what stock bulls want to hear, especially since it was a surge in discretionary spending that came along with hefty corporate tax cuts that spurred on equities in 2017 and for much of this year before October’s downdraft. The concern is that all this government borrowing will “crowd out” companies, making it more expensive for them to sell debt and squeeze their profit margins. Already, yields on investment-grade bonds have risen to 4.24 percent on average, the highest since 2010 and up from 2.75 percent in mid-2016, data compiled by Bloomberg show.

CURRENCY TRADERS ARE HAPPY — FOR ONCE

About the only thing that made investors any money in October was currencies. While the MSCI All-Country World Index of equities, the Bloomberg Barclays Global Aggregate Bond Index and the Bloomberg Commodity Index were all headed toward losses, the Citi Parker Global Currency Index was poised for its best — and first — winning month since May. The measure, which tracks nine distinct foreign-exchange investment styles, was up 0.95 percent for the month through Tuesday. Currency traders are notoriously bad at making money. The Citi Parker Index has fallen in seven of the past nine years and is on track to drop again in 2018 even with October’s gains. But much of the good fortune of late was likely due to the big rally in the U.S. greenback, with the Bloomberg Dollar Spot Index up 2.40 percent in October for its best showing since soaring 3.91 percent in November 2016. Hedge funds and other large speculators have 242,000 contracts betting on dollar gains, Commodity Futures Trading Commission data show. That’s about seven times more than the average over the past 10 years and shows just how optimistic currency traders are on the outlook for the U.S. economy and higher interest rates. But maybe the dollar, which by the Bloomberg index is the highest since May 2017, is becoming too strong. Officials at conglomerate 3M Co. said on the company’s earnings conference call last week that “foreign currency, net of hedging, reduced per-share earnings by $0.08 as the U.S. dollar strengthened against many currencies throughout the quarter.”

COMMODITIES SEND NEGATIVE SIGNALS

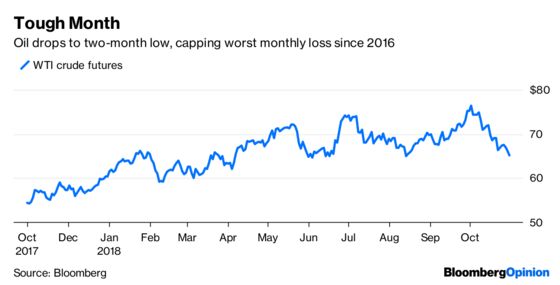

Here’s another thing that the stock bulls might want to consider: The Bloomberg Commodity Index fell in October, bringing its year-to-date loss to 5.65 percent and increasing the odds that the market will have a losing year for the first time since 2015. That’s usually not the type of performance that would signal an up arrow for the global economy. Consider the oil market. West Texas Intermediate prices fell on Wednesday to their lowest level since mid-August at about $65 a barrel and are headed for the biggest monthly loss since 2016. “There’s a sense that the global economy goes into a bit of a slowdown and demand in 2019 isn’t quite as robust as it has been over the past couple years,” Brian Kessens, who helps manage $16 billion in energy assets at Tortoise Capital Advisors, told Bloomberg News. “We are still in more of a risk-off sentiment.” U.S. supply data released Wednesday also showed a sixth consecutive increase in domestic crude inventories, a sign that perhaps demand is softening. The flip side is that consumers will see some relief at the pump. Gasoline futures fell 2.10 percent Wednesday to their lowest levels since April. One commodity that has bucked the softening trend lately is sugar, with prices up 18 percent in October — just in time for Halloween. And despite the first increase in candy prices three years, Americans were expected to boost spending on sweet treats this October by 4.2 percent from a year ago, according to Bloomberg News’s Sophie Caronello. As candy is a comfort food, the increase in spending makes sense if it helps investors reduce the pain from the broad losses in markets in October.

TEA LEAVES

So, is all this renewed optimism in the stock market warranted? The answer to that question may unfold in coming days. First up will be the Institute for Supply Management’s manufacturing report for October on Thursday. The median estimate of economists surveyed by Bloomberg News is for a reading of 59, which will keep the gauge at about its highest level since 2004. The measure is a diffusion index, meaning readings above 50 denote expansion and those below 50 signal contraction. Within the index, economists will be zeroing in on the new orders component for signs that the escalating trade war may be having a negative effect. Then on Friday, the U.S. Labor Department releases its monthly employment report, with economists expecting the government to say that 200,000 jobs were created in October, up from September’s storm-depressed 134,000 figure. The downside is that average hour wage growth is expected to slow to 2 percent from 3 percent. Those two reports will be a prelude to next week’s midterm elections, which have the potential to roil markets depending on how they shake out. In short, it may not be time to signal the all clear in equities just yet.

DON’T MISS

Five Reasons Why the Stock Market Has Declined: Barry Ritholtz

Foreigners Like U.S. Debt as Much as They Ever Have: David Ader

The Slowdown in Europe Should Give the Fed Pause: Karl W. Smith

Draghi Gets Some Breathing Room from Inflation: Marcus Ashworth

Even Wedding Planning Involves Leveraged Loans: Brian Chappatta

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.