(Bloomberg Opinion) -- Markets hate uncertainty, and Brexit has it in spades. Leaving the European Union seems to present the U.K. with an unappealing choice of either a lot of economic harm via crashing out without a deal, or slightly less damage via Theresa May’s withdrawal agreement. But there are reasons why investors might start thinking about more blue-sky scenarios: Either a Brexit so benign that the British economy beats expectations, or a second referendum that keeps the country in the EU.

Right now, markets are reflecting Prime Minister Theresa May’s pitch to her truculent party: There is her deal, or there’s no deal. Her agreement with Brussels offers an orderly two-year transition and an amicable split, as well as a base from which to agree a future trade relationship. But it will be an almighty task to get it past the House of Commons. If it's rejected, the U.K. faces the grim scenario of a chaotic no-deal Brexit, which the Bank of England says might cause an economic crisis.

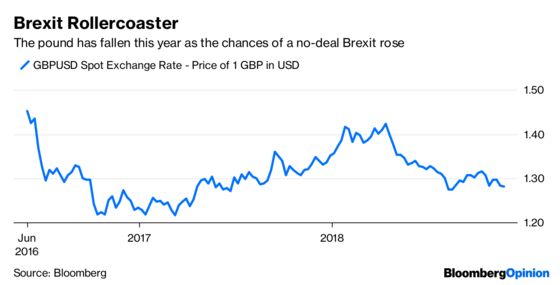

That’s why the pound trades between $1.20 and $1.30, reflecting some of the possible upside from May’s deal but still weighed down by the potentially cataclysmic no-deal scenario. Traders are naturally focused on the next fork in the road – the parliamentary vote –and until lawmakers have their say on May’s deal, it’s hard to take a clear view on investing in Britain.

But there’s an argument to make that traders are being too pessimistic. Public opinion is warming to May’s deal, according to a Survation poll this week, and that might help its chances in parliament. Lawmakers have a duty to act in the interests of the nation, not just their constituents, and the risk of plunging the country into recession may see cooler heads prevail. If it passed, there’s a very good chance that the pound’s relief rally would surpass the $1.30 level last seen when May first announced her deal. Avoiding a cliff-edge exit would probably boost investment and the economy, and would improve the chances of delivering a reasonable trade deal.

That’s not to get carried away. Given the parliamentary arithmetic and the decades-old obstinacy of the Brexiter wing of May’s Conservative Party, her task still looks pretty impossible. If her deal does fail, it will be a negative sign and a trigger for more volatility. But it might also build momentum behind another soft-Brexit solution that’s winning support from her ministers: The so-called “Norway Plus" option.

This wouldn’t stop freedom of movement (a bugbear for many voters), but it would keep Britain attached to the EU single market and would preserve ties on a par with the “close economic partnership” scenario outlined by the Bank of England this week. That was the only Brexit outcome in which the central bank said GDP trend growth would be better than current expectations. An emergency immigration brake might help it squeak through parliament.

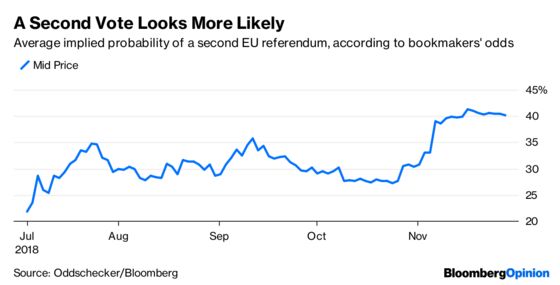

Nor should we ignore the chance of a second referendum, which the public increasingly supports. The implied probability of a new vote has jumped to about 40 percent, according to Bloomberg data based on bookmakers’ odds. It’s a long shot, but if May is replaced as prime minister, and if her successor fails to deliver any real improvement on the departure terms, a referendum might be offered as a way to avoid an election or a no-deal Brexit.

There are obvious risks to consider here, as fund managers have noted. Anything that brings Labour’s hard-left leader Jeremy Corbyn closer to power, such as a collapse of Theresa May’s wafer-thin majority, would hit sterling. Another referendum could be won by the leavers again. Even if the remain side prevailed, it might well entrench the national divisions that were laid bare in the first vote. The bitterness of disappointed leave voters would be hard to dislodge.

Still, from an investor perspective, the upside scenarios – the passing of May’s deal or something like it, an alternative such as Norway-Plus, or a second referendum – outnumber the negatives: a no deal Brexit or a Corbyn government. It’s a brave bet but there are ways for sterling to get back to between $1.40 and pre-2016 levels of $1.50, and for domestic equities to get a bump after a couple of years of being shunned. There’s room for some blue-sky thinking on Brexit.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.