The Grim Logic of Trump’s Trade War With China

Geopolitical primacy, not maximum prosperity for Americans, might be the US president’s true objective.

(Bloomberg Opinion) -- A month ago, I declared that President Donald Trump’s trade war against China looked like it might be winding down. I was wrong. Instead of capitulating in exchange for some agricultural purchases and other minor concessions, Trump is doubling down. He’s raising tariffs on $200 billion worth of Chinese imports from 10 percent to 25 percent, and imposing new tariffs on almost all of the remaining $325 billion or so. China today said it would retaliate and starting next month would impose tariffs on $60 billion of U.S. goods. This is the biggest trade war in modern American history.

There were several reasons it looked as if Trump might back off. First, it’s very hard to verify whether Chinese theft of intellectual property — one of the biggest and most justified complaints from the U.S. side — is still happening. Even if Chinese companies and the Chinese military were to stop appropriating the fruits of U.S. research and development, they would still be able to make some progress by cleverly reverse-engineering American-made products, raising accusations of continued espionage. A similar enforceability problem applies to Chinese non-tariff trade barriers; for example, Chinese local governments quietly and unofficially helping Chinese companies outcompete American companies in the domestic market. So even if China acceded to U.S. demands, ensuring compliance would be hard. The difficulty of establishing a credible enforcement mechanism is probably a big reason trade talks have broken down.

Second, the trade war has cost the U.S. Economists have shown that the actual burden of tariffs has fallen mostly on American consumers — in other words, the prices consumers pay for imported goods has risen, while the prices Chinese sellers receive hasn’t changed very much. And higher prices on capital goods and intermediate goods is raising expenses for U.S. manufacturers, making them less competitive. Meanwhile, Chinese retaliation has hurt U.S. farmers.

So with victory hard to verify and losses mounting, it looked like there was little reason to continue the trade war. Yet Trump is doubling down. Why?

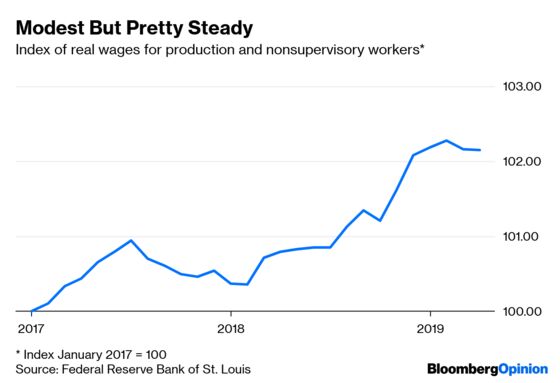

Trump may be calculating that the strong U.S. economy and resilient stock markets mean that there is little downside to continuing the trade war. Despite higher import prices, real wages have generally continued to rise at a modest rate:

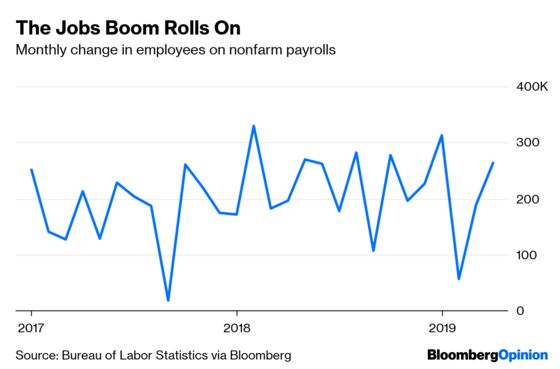

The economy also continues to add jobs at a strong pace, despite a historically low unemployment rate:

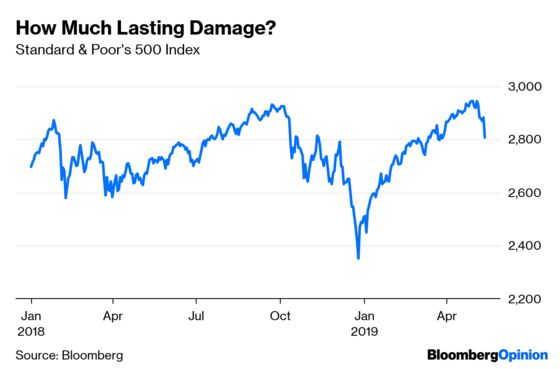

Meanwhile, U.S. stock markets are not all that much below record highs, having largely recovered from a tumble in late 2018. China’s announcement of retaliatory tariffs has put a modest dent in equity markets, though that may well be temporary:

With the economy doing well enough for many Americans not to notice the pinch from the trade war, losses on the U.S. side have been concentrated among farmers. And it seems that Trump is betting that a combination of government payouts and cultural affinity will mean few farmers desert him at the ballot box.

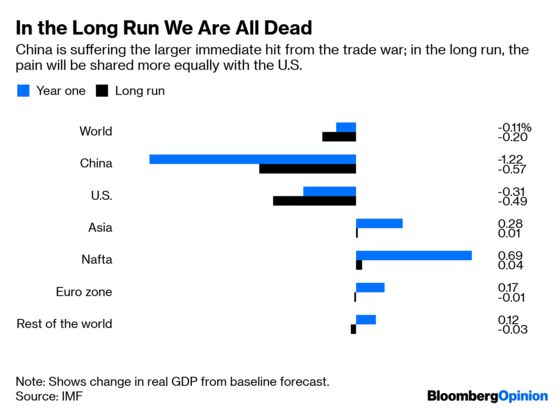

Meanwhile, the trade war appears to be hurting China’s economy. It’s hard to isolate the affect of the dispute from other factors, like Chinese government attempts to crack down on the shadow-banking system. But the International Monetary Fund forecasts that the immediate blow from the trade war is hitting China much harder:

Chinese exports, fixed-asset investment, consumption and industrial production may already have taken a hit. In the long term, both U.S. tariffs and Chinese retaliation may deter multinational companies from producing goods in China; some already are blaming the trade war for a slowdown in foreign direct investment. And by forcing China to shift from exports to investment in order to sustain growth, the trade war might push the country toward a less productive growth model.

There may be a grim sort of logic to this approach. So far, China’s ascent in the 21st century has looked unstoppable, as it gobbled up one manufacturing industry after another, shouldered the U.S. aside as the world’s biggest exporter, and became the beating heart of an East Asian economic supercluster. In addition to threatening to relegate North America to the global economy’s periphery, this trend directly imperils U.S. military dominance, as economic and technological supremacy tends to translate into military supremacy.

If Trump wants to slow China’s ascent as a superpower, a trade war might be an effective way to do it. If the harm to the U.S. is modest and the costs for China are severe and lasting, Trump might conclude that the former are acceptable losses. Geopolitical primacy, not maximum prosperity for Americans, might be the president’s true objective.

It’s also possible, of course, that the trade war is a purely populist endeavor, and that maintaining tariffs is simply a way for Trump to look tough. If he calculates that there is less to be gained from striking a deal than from continuing the tariffs, or if weakening China really is the goal, then this could be just the opening rounds of a long and grinding trade war.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2019 Bloomberg L.P.