(Bloomberg Opinion) -- Hargreaves Lansdown Plc, Britain’s equivalent of Charles Schwab Corp., is embroiled in a dispute with Terry Smith, one of the country’s best-known fund managers. The spat illustrates the difficulty – the folly, even - of trying to choose a winning stockpicker to swell your retirement savings.

HL has whittled down its Wealth 150 list of recommended funds to a more exclusive Wealth 50 selection, though the initial roster actually features 60 funds. All those featured have agreed to discount their fees for HL customers, by an average of 30 percent.

That prompted Smith, the founder and chief executive officer of Fundsmith LLP whose offerings didn’t make the list, to allege the platform selects funds that maximize its own profit potential rather than focusing on potential returns for its customers, according to the Times newspaper.

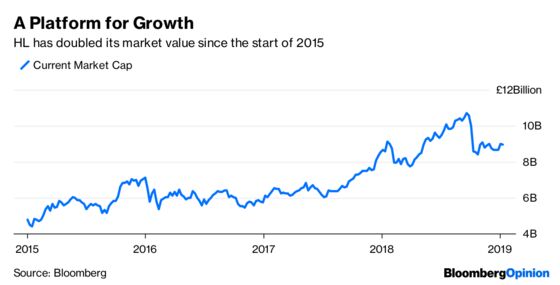

There’s no question that HL has profited from the shifting investment landscape as individuals have taken more control of their retirement savings. It services more than 1.1 million clients and controls assets of more than 94 billion pounds. The company’s market value has doubled since the start of 2015.

HL has grown its active client base by 50 percent and its assets by 70 percent since 2015 by building a better mousetrap for customers. But it’s also prone to using the kind of hyperbolic marketing that gives the investment industry a bad name. In 2017, for example, its Twitter account extolled the virtues of fund manager Nick Train as “the U.K.’s answer to Warren Buffett.”

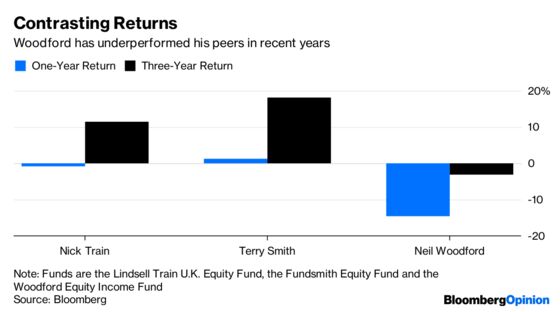

Train, as you might expect, makes the trimmed-down list of funds recommended by HL. Perhaps more surprising is the inclusion of Neil Woodford, whose recent performance has cost his investors dearly. Both have lagged behind Smith.

Mark Dampier, HL’s research director, told the Telegraph newspaper that 90 percent of the 2,500 or so funds available to U.K. investors “are useless anyway,” which is quite a damning verdict on the industry as a whole. He defended Woodford’s selection, saying the manager had been through worse periods in his time and had come back strongly.

Now, I have no idea whether Woodford will recover his mojo, or whether Train’s future picks will stumble, or whether Smith’s equity selections will continue to shine. But neither does HL.

Despite the disclaimer attached to the investment fund industry’s marketing brochures that past performance is no guarantee of future returns, the halo of historical success still counts for more than it should in the business of selling investment products.

The one factor investors can control for is fees. And while HL uses its clout to secure a discount from the funds it recommends, it in turn levies a 0.45 percent annual charge, driving the average cost of investing in an active fund through its platform to a bit more than 1 percent. No wonder the flood of money into low-cost passive strategies continues unabated.

Given the vagaries of the returns delivered by the active crowd in recent years, retail investors should be wary of buying whatever active products brokers like HL are selling. And the sooner the zero-fee index tracking products pioneered in the U.S. by Fidelity Investments make it to other countries, the better.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.