(Bloomberg Opinion) -- Should we just give up now?

The world’s electrical utilities need to reduce coal consumption by at least 60 percent over the two decades through 2030 to avoid the worst effects of climate change that could occur with more than 1.5 degrees Celsius(2.7 degrees Fahrenheit) of warming, the Intergovernmental Panel on Climate Change announced Monday.

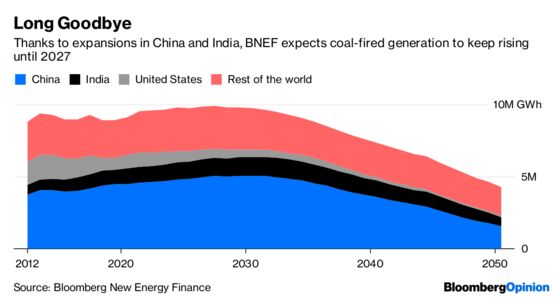

Such a target seems wildly ambitious: Even Bloomberg New Energy Finance, which tends to be more optimistic than other analysts (and more accurate) about the speed of energy transition, expects coal-fired generation to increase by 10 percent over the period. Hold on though. Is it really such a stretch?

After all, U.S. coal-power generation decreased by about a third in the seven years through 2017, to 12.7 billion British thermal units from 18.5 billion, based on data from energy-market consultancy Genscape Inc. In the European Union, black-coal generation fell by about the same proportion over just four years through 2016, according to Eurostat, to 385,925 gigawatt-hours from 544,279 GWh.

Across Europe and the U.S., the decline in coal output recently has averaged close to 5 percent a year. If the world as a whole can reach 7 percent a year, it would be on track to meet the IPCC's 2030 target.

The conventional wisdom is that this isn’t possible, as rising demand from emerging economies, led by China and India, overwhelms the switch from fossil fuels in richer countries. That may underestimate the changing economics of energy generation, though.

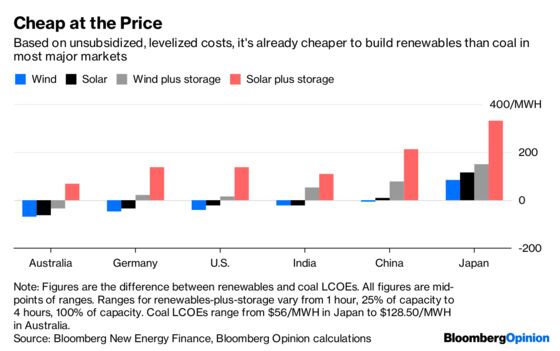

For one thing, it assumes that Asian countries will continue to build new coal-fired plants at a rapid rate, even though renewables are already the cheaper option in India and heading that way in China and Southeast Asia. For another, the falling cost and rising penetration of wind and solar is so recent that we’re only just starting to see how they damage the business models of conventional generators.

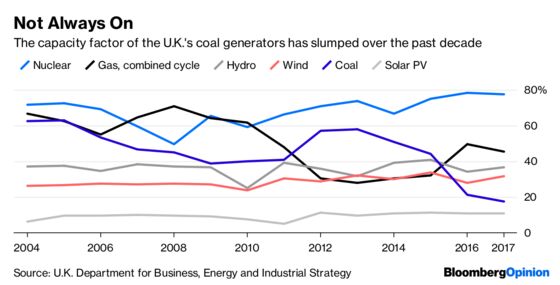

Thanks to the deflation of recent years, renewables already produce energy at a lower cost than thermal power plants. That causes the overall price of wholesale electricity to fall, reducing a conventional plant’s revenue per megawatt-hour. When this drops below the generator’s operating costs, the only away to avoid losing money is to switch off altogether. As a result, capacity factors — the share of time when the plant is on and producing electricity — decline as well, further undermining returns.

The shift from an always-on “baseload” demand profile to a peaks-and-troughs one like this carries its own problems. The act of ramping up and down consumes fuel and causes the physical plant to wear out faster. Absent expensive refurbishments, that could take a decade off the 40- to 50-year life of a coal plant — and banks will get progressively less likely to fund long-term refurbs as wind and solar further damage the economics of fossil power.

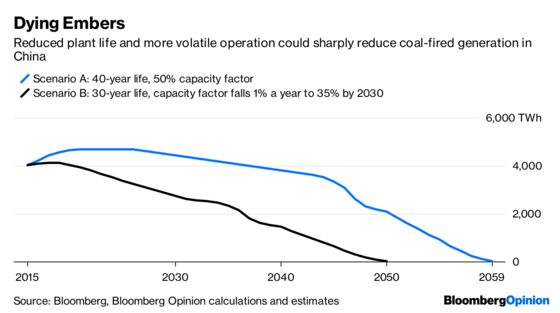

Researchers at the Australian National University this year modeled the effect of this sort of scenario on that country’s generation mix. Assuming that the cost of renewables continues to evolve in line with current trends, they found the average retirement age of coal plants falls to 30 years from 50 years. As a result, coal-powered generation drops by about 70 percent between 2020 and 2030.

It’s not hard to produce comparable results for China’s more modern coal fleet, whose fate will be the decisive influence over electricity-related emissions in the coming decades. Let’s assume the addition of net new generation stops in 2020; that plant life reduces to 30 years from 40 years; and that capacity factors gradually fall from the current 50 percent to 35 percent, still well above the levels of the U.K.’s coal generators in recent years. The effect of those operating changes alone reduces coal-fired electricity output in 2030 by about 40 percent relative to the higher scenario.

Of course, that’s not enough — but it’s also not an outrageously challenging scenario. Factor in a price on carbon (the European Union’s emissions certificates are one of the best-performing commodities this year) or other robust government intervention and the decline would be much faster.

It also assumes that renewables penetration in China a decade from now won’t be much more disruptive than in developed countries right now — and there’s reason to think that’s too pessimistic.

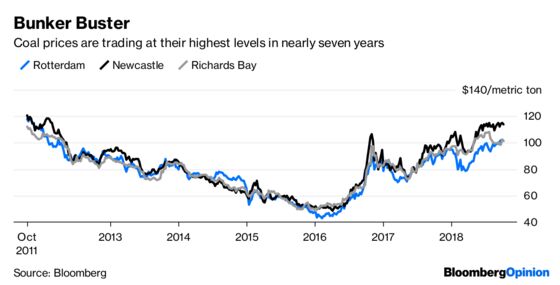

After all, about half the cost of coal-fired power is the fuel itself, which is currently trading at six-year highs. At present, while new renewables are cheaper than new coal almost everywhere in the world, it’s still usually more profitable to run existing thermal generators than to decommission them and build replacement wind and solar instead.

The mainstream view is still that we can’t decarbonize our electricity system fast enough to meet the IPCC’s targets. But a decade ago, the current situation of plateauing demand for coal and car fuel and cratering renewables costs looked equally outlandish. Given the way the world’s energy market has changed in recent years, it’s a good idea to never say never.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.