This Bond Giant Still Has $15 Billion to Play With

(Bloomberg Opinion) -- This year heralds a brave new world for euro credit spreads. The continent’s biggest buyer of corporate debt is calling a halt after amassing a 180 billion euro ($206 billion) portfolio in just two and a half years. The European Central Bank’s Corporate Sector Purchasing Program (CSPP for short) is ending net new buys after gorging on investment grade euro corporate bonds. But the party isn’t completely over – just slowing down a lot.

The ECB has forged a different post-crisis path than other central banks, pushing QE stimulus more directly into the real economy by buying company debt. The Bank of England briefly followed, but stopped at just 10 billion pounds. The U.S. Federal Reserve chose another route, buying mortgage-backed bonds to breathe life back into its hardest hit sector: Real estate. Horses for courses.

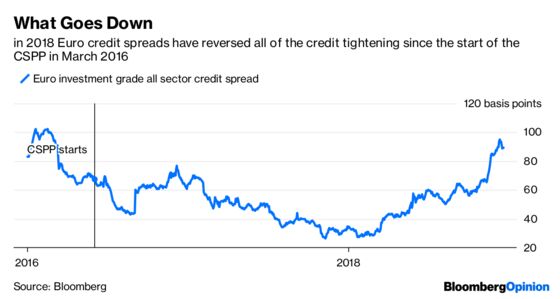

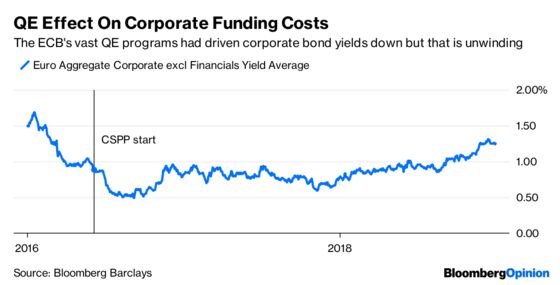

At first glance, it’s tempting to ask what the ECB achieved, given that corporate spreads are back above where they were when it first put on its buying boots in June 2016.

But it’s fairer to look at just how much European companies have benefited from super-cheap financing. The stimulus effect has penetrated deeper into the real economy than ever would have been the case with just buying government bonds. With cheap long-term finance locked in for many years to come, that should underpin the economy.

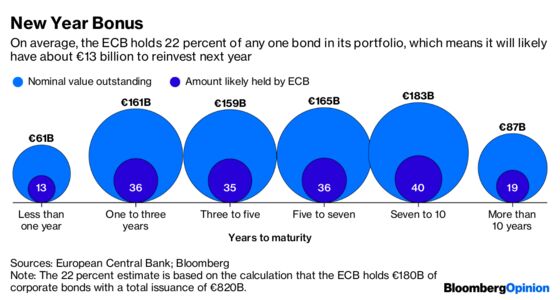

While net new additions to the ECB’s program will cease this year, it has committed to reinvest maturing bonds to maintain the portfolio’s stock at 180 billion euros. So it will still play a critical role in underpinning investment-grade corporate bonds.

The ECB is vague on the exact breakdown of its holdings (it does declare which bonds its owns, just not how much). Nonetheless, using some educated guesswork, my assumption is that the CSPP may have as much as 13 billion euros ($15 billion) of redeeming maturities to invest in 2019. So as much as 1 billion euros per month – that’s still a lot of bonds.

These purchases can be spread out across the year or bunched as it sees fit. This isn’t quite the 6 billion-euro monthly pace that was kept up during most of the program’s existence. But there won’t be a sudden end to support for corporate credits.

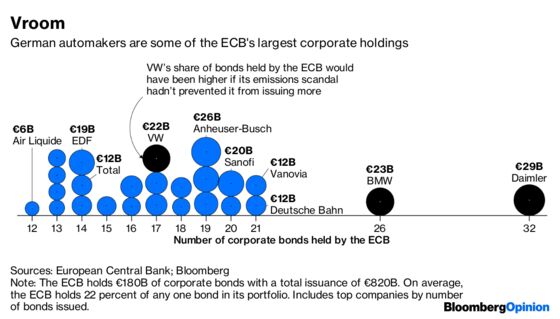

The ECB tends to take advantage of market liquidity when it can – 17.5 percent of its holdings are direct from new issues – and it understandably favors big issuers to be able to get the size of holdings it needs. Otherwise, it’s fairly agnostic. It goes where the paper is.

Take German automakers. Volkswagen AG’s bond issuance is ramping back up again, with 4.25 billion euros sold in November after a relative drought after the diesel emissions scandal. BMW AG and Daimler AG have been more frequent tappers of the market, so the ECB holds more of their issues. Both are expected to issue large bond deals early in the new year. It’s a shame for them that their timing wasn’t sooner as it precludes the ECB from investing as heavily.

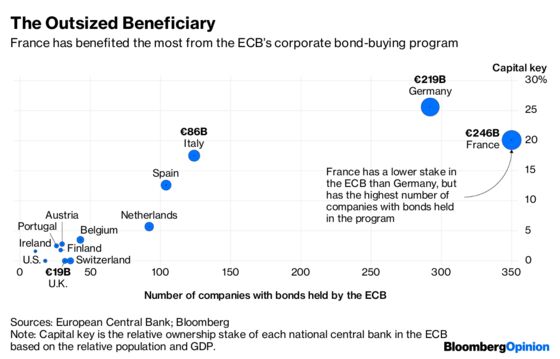

French companies might suffer the most from the CSPP halting new purchases as they’ve been outsized beneficiaries. But even U.S. and U.K. companies have benefited. So long as the issuing entity is domiciled in the euro area, it doesn’t matter if the parent isn’t.

With the European credit landscape shifting so profoundly, it will be interesting to see whether the program’s proceeds are reinvested into similar industries and countries – or whether the new issuance available will alter the Franco-German industrial dominance. The CSPP will remain crucial for credit watchers even if the program is no longer growing. It’s still the main actor in the euro credit show.

Elaine He provided graphics; Paul Cohen data.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.