(Bloomberg Opinion) -- The Dow Jones Industrial Average rose to a record Tuesday, and the S&P 500 Index was on the verge of doing the same. Those would surely be good signs, as President Donald Trump’s Twitter feed has pointed out whenever the benchmarks reach new highs, except that cracks are starting to develop in some significant parts of the equities market.

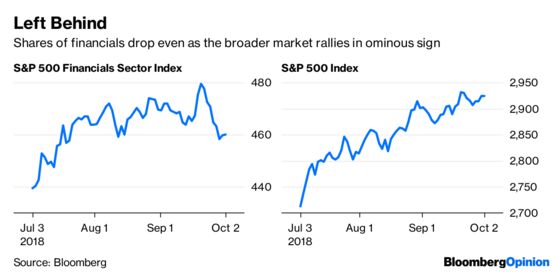

First, the Russell 2000 Index that tracks the shares of smaller companies, which theoretically should be the prime beneficiaries of the White House’s “America First” agenda because they mainly have a domestic focus, has fallen off a cliff. The gauge is down 4.87 percent since August while the S&P 500, which is stuffed with large multinationals, has gained about 0.76 percent. Second, and perhaps more concerning, shares of financial companies are sliding, falling in seven out of the eight trading days. After all, if investors are losing confidence in the all-important financial sector, how can they have confidence in the market more broadly? “This is a classic late-cycle canary in the coal mine indicator,” longtime Wall Street strategist and current Gluskin Sheff & Associates chief economist David Rosenberg wrote in a Twitter post. Maybe, but you have to wonder whether such moves may be an early sign that investors are setting up for the possibility that the Democrats regain control of the House — and possibly the Senate — from Republicans in the midterm elections a little more than one month away. If that were to happen, there’s a chance that the Trump pro-business policies that have helped small businesses and financial firms, such as reduced regulations and lower taxes, may be blocked.

“An unexpected Blue Tsunami, where the GOP loses control of the House and Senate, may not be taken well on the Street, as headline risks could surge with Democrats seeing that kind of a tectonic shift as a mandate to oppose the president across many areas,” Citigroup Inc. strategists wrote in a Monday report. “Given large budget deficits it would seem that any major new stimulus to generate faster GDP is improbable, thereby limiting any need to bump up (earnings) forecasts.”

JUNK BOND MILESTONE

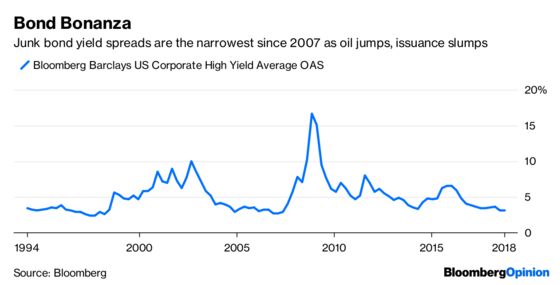

Any angst being expressed by stock traders is failing to show up in the market for corporate bonds. Comcast Corp. had no trouble selling $27 billion of bonds to finance its $39 billion purchase of Sky Plc. The longest portion of the offering, a 40-year security, may yield 1.75 percentage points above Treasuries after initially expected in a range of 1.95 percentage points to 2 percentage points. As amazing as that is, it pales in comparison to what is happening in the market for corporate debt with speculative-grade, or junk, ratings. The extra yield investors demand to own the securities instead of risk-free Treasuries has shrunk to 3.09 percentage points, the least since July 2007, which, by the way, was before the financial crisis. The narrowing in the spread is, in part, a reflection of rising oil prices that have bolstered energy companies and lack of new supply. Issuance of new junk bonds is down 30 percent this year from the same period in 2017, according to Bloomberg News’s Gowri Gurumurthy. Times are so good for junk bonds that S&P Global Ratings on Monday said it expects the 12-month trailing default rate, which fell from 3.9 percent in mid-2017 to 2.9 percent in June, to keep dropping and reach 2.25 percent by mid-2019. The Bloomberg Barclays U.S. Corporate High Yield Bond Index has gained 2.76 percent this year, compared with a loss of 2.58 percent for the global debt market.

CIAO, ITALY?

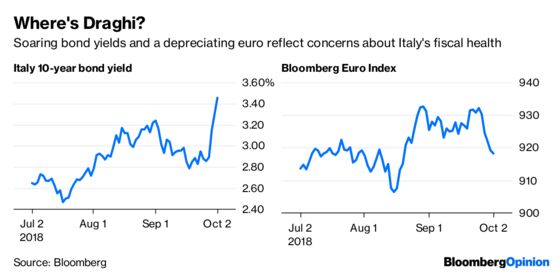

In 2012, with Greece on the precipice and the euro in jeopardy of breaking up, European Central Bank President Mario Draghi was credited with calming global nerves by pledging to do “whatever it takes” to save the currency union. Could Draghi be called upon again to make a similar pronouncement? It’s certainly possible with things getting worse by the day in Italy. The yield on the nation’s 10-year bonds touched the highest level in more than four years after Claudio Borghi, head of the lower house budget committee, said the euro was “not sufficient” to solve Italy’s fiscal issues, according to Bloomberg News’s John Ainger. Though Borghi later played down the comments, they were sufficient enough to get investors talking about the odds of Italy ditching the euro and resurrecting the lira. “European risky assets remain vulnerable, and there is potential for negative spillovers to the euro area given the high trade exposure to Italy,” Goldman Sachs Group Inc. strategists led by Alessio Rizzi wrote in a research note. “While our economists do not expect systemic implications for the global economy, contagion risks have risen.” The Bloomberg Euro Index fell for a fifth consecutive day, its longest slump since December. The FTSE MIB Index of shares fell as much as 2 percent to the lowest level since April 2017, before paring losses. Jean-Claude Juncker, president of the European Commission, said that “we have to do everything to avoid a new Greece.” Italy’s credit rating is due for review by Moody’s Investors Service and S&P Global Ratings later this month. Both have the nation two levels above what is considered junk.

BRAZIL REBOUNDS

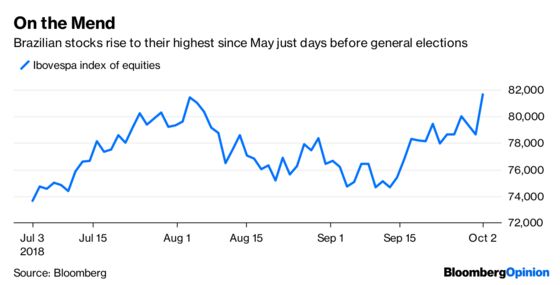

Things are looking up for markets in Brazil as far-right presidential candidate Jair Bolsonaro received a big boost in the latest opinion poll published just days ahead of Sunday’s general elections. The former Army captain rose four points to 31 percent in the Ibope survey released Monday evening, compared with 27 percent in the last poll Sept. 26, according to Bloomberg News’s Bruce Douglas. His nearest rival, Fernando Haddad, from the left-wing Workers’ Party, remained at 21 percent. “Bolsonaro is and remains the preferred candidate by the market,” Bernd Berg, a strategist at Woodman Asset Management AG in Zug, Switzerland, told Bloomberg News. If the conservative wins, he said, Brazilian assets will post a “staggering rally of more than 10 percent.” Although the broader market for emerging-market equities and currencies fell on Tuesday, Brazil staged an impressive rally. The benchmark Ibovespa index of equities surged as much as 4 percent in its biggest gain since May 2016. The real appreciated as much as 2.81 percent to its strongest level since August. Given Brazil’s size and influence — it’s the “B” in the BRIC acronym that also includes Russia, India and China — it’s hard to see emerging markets staging any meaningful rebound without the South American nation.

COMMODITIES CATCH A TAILWIND

The commodities market is rebounding, and it’s not all because of surging oil prices. The Bloomberg Commodity Index jumped about 1 percent on Tuesday to its highest since June even though prices for West Texas Intermediate crude oil finally took a breather to end the day little changed. The gauge has risen in 10 of the last 11 trading days. Tuesday’s gains were unusually broad-based, with everything from gold to aluminum and wheat to sugar advancing. It’s hard not to tie the strength in commodities to the notion that the trade dispute between the U.S., Mexico and Canada was resolved without much actual change. “This is a potential stoppage of the bearish trade narrative that U.S. agriculture has seen,” Rich Nelson, the chief strategist for Allendale Inc., told Bloomberg News. The thinking, or rather hope, is that maybe the U.S. and China will end their trade dispute similarly. Regardless, the fact is that most don't see these trade skirmishes having much impact on worldwide output. The Organization for Economic Cooperation and Development said last week that it was trimming its estimates for global economic growth this year by just 0.1 percentage point to 3.7 percent and by just 0.2 percentage point in 2019 to 3.7 percent.

TEA LEAVES

You may want to strap yourself in. Over the next few days, market participants will get a slew of high-level economic data in the U.S. that will go a long way toward determining whether the Federal Reserve was justified in taking such a hawkish stance at its monetary policy meeting last week. First up on Wednesday will be the monthly ADP Employment report, which is forecast to show that American businesses added more workers in September than in August. Also, the ISM’s nonmanufacturing index for September is expected to be little changed at levels that signal strong growth. The avalanche continues Thursday, with the release of factory orders for August. And finally on Friday, the government will release data on the trade balance for August and the all-important September jobs report. “This historically rare pairing of steady, low inflation and very low unemployment is testament to the fact that we remain in extraordinary times,” Fed Chairman Jerome Powell said Tuesday.

DON’T MISS

Meet Wall Street’s Latest Frankenstein Creation: Stephen Gandel

Emerging Markets’ Oil Shock Has Already Started: David Fickling

The Gentlemen of the Spread Vote No on Italy: Marcus Ashworth

What Booming Sioux Falls Tells Us About the Economy: Justin Fox

Pew Got It Wrong. Pension Funds Need Alternatives: Aaron Brown

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.