The Sooner the BOE Hikes Rates, the Sooner It Can Stop

Does it matter if the Bank of England’s Monetary Policy Committee decides to hike its rate this Thursday?

(Bloomberg Opinion) -- Does it matter if the Bank of England’s Monetary Policy Committee decides to hike its rate this Thursday? Or if it instead waits for more data on the labor market and raise instead at the Dec. 16 meeting? Not so much.

But it really does matter what the MPC does after that. It won't do anything for the central bank's reputation if it dithers and delays. So the BOE had better get its communication strategy right for once or else it will allow inflationary expectations to rip.

The central bank has kept the stimulus hosepipe on too long. In order to avoid a massive policy error, it has to admit it’s been asleep at the wheel and raise rates. Unfortunately, correcting mishaps is never that simple and by reacting too sharply it risks crushing the recovery and compounding its missteps. It’s a situation all of the BOE’s own making.

Governor Andrew Bailey has marched us up this hill with repeated signals to expect more than one rise in the bank rate in the near term. This quarterly MPC meeting should get on with tweaking the current 0.1% to 0.25% — and then give us an idea of when it will be raised more substantively. And there’s an even more important message to impart: How the BOE will quell the inflationary beast for the foreseeable future.

Vague platitudes on waiting for more data will not be accepted. We deserve clarity after seeing the central bank effectively tear up its long-held forward guidance of near-zero interest rates on Sep. 23. This must come across at the press conference, which also needs to be of a substantially higher quality than any so far in Bailey’s tenure. But make no mistake, as a rate hike is fully priced in — and the bank has not pushed back against that — a failure to act will weigh Bailey down with a reputation for inconsistency.

One question is the handling of the remaining 20 billion pounds ($28 billion) of the BOE’s 150 billion-pound pandemic stimulus program. It looks ridiculous to be ploughing on with quantitative easing while simultaneously raising rates. The MPC might think this a trifling matter: After all, there’s just six weeks before the program expires. Sadly not so inconsequential for the gilt market, which is seeing what little net supply there is left vanish for the rest of the financial year to April.

The Oct. 27 Budget from Chancellor Rishi Sunak, courtesy of revised estimates from the Office for Budgetary Responsibility, reduced the amount the government intends to borrow this year by about 58 billion pounds. Nineteen carefully planned gilt auctions have been cancelled leaving, as it stands, just 3 billion pounds of net supply for investors over the next five months. This mess could be neatly alleviated by the BOE stopping pointless QE immediately and not draining the gilt market of a further 20 billion pounds of gilts.

Short-term imbalances aside, what’s of fundamental importance is when the MPC decides to let its 875 billion-pound QE balance sheet naturally reduce — the proper definition of tapering — as its holdings mature and it doesn’t reinvest the proceeds. Otherwise, it would be a twin-tightening maneuver. Then-Governor Mark Carney outlined in a January 2020 speech that the BOE viewed every 25 billion pounds of QE bond buying as the equivalent of 25 basis points of rate cuts. It might not work exactly in reverse, but letting the balance sheet reduce is absolutely a version of tightening policy.

A combination of interest-rate hikes — if a second increase to 0.5% follows at the February MPC as is widely expected — and an automatic reduction in the stock of QE could have an impact in early March. That’s when the BOE’s 28 billion pound stake in the 4% 2022 gilt matures. Policymakers ought to monitor the impact of that dual-tightening on the economy before contemplating a swift, third rate rise to 0.75%.

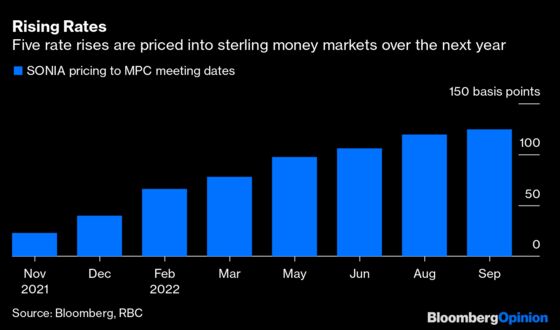

The money markets are already pricing this in by May, with a further two hikes to 1.25% by September. It’s time for rational forward guidance. The MPC badly needs to put some perspective on how aggressive it intends to be. Doing nothing this week will lead the market to irrationally run away, further hedging in exposure that risks slamming the brakes on the fragile pandemic recovery.

Moreover, with the bulk of recent price surges being the “wrong type” — the BOE needs to be careful as it sends a much-needed message on tamping down inflationary expectations. As Bailey commented in September, raising interest rates will have minimal effect in controlling global natural gas prices, computer chip supply or providing more truck drivers. Bloomberg Economics, using its new SHOK model, estimates higher U.K. interest rates will lower growth more pro rata than any concomitant reduction in inflation. So the Bank's sudden inflationary-fighting zeal needs to be constrained if the spillover into higher corporate borrowing and household financing costs isn't to cause unnecessary damage. The bank rate can have a much bigger spillover effect into the interest rates that are charged in the real economy.

There needs to be some clarity in what the central bank actually wants to achieve after spending the past year preparing the banking system for negative interest rates. Although there is likely to be dissension over timing among the nine-member committee there has to be a consistent message sent. In short: Get a grip.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.