(Bloomberg Opinion) -- Money manager Steve Eisman famously predicted the 2007-2008 blowup of the mortgage debt bubble, one of the few to believe that such a “black swan” event was possible. A decade on, the “Big Short” star is back with a bearish bet against two unnamed British banks that he thinks would suffer from a no-deal Brexit.

While this is hardly black swan territory, given how many other people are preparing for Britain and the EU to fail to agree departure terms, it’s still worth paying attention to Eisman.

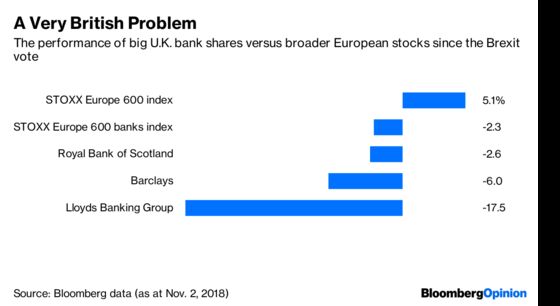

His warning, at a conference in Dubai over the weekend, is preaching to the converted in many ways. The U.K. is shaping up to be the world’s least popular country for equity investors over the next 12 months, according to surveys by Bank of America Corp. Shares of Royal Bank of Scotland Group, Barclays Plc and Lloyds Bank Plc have fallen by between 2 and 18 percent since the Brexit vote.

Even so, there may still be some complacency in the European financial markets — both in Britain and elsewhere — that hasn’t been adequately priced in.

First off is the “no deal” question. Hopes have been increasing over the past few days for some kind of deal between the U.K. and Europe that would cement future trade ties and somehow answer the question about how to avoid a hard border between Ireland and Northern Ireland. But these might yet be dashed.

While getting Brussels and Westminster to agree is hard enough, getting a deal past a fractious and rebellious U.K. parliament may well prove impossible. That’s the eventuality that Eisman is betting on, and it’s not a crazy wager. Analysts at UBS Group AG, the Swiss bank, also describe the chances of British lawmakers rejecting an agreed deal as “non-zero.”

And while Eisman has chosen to home in on two banks, the threat to the broader financial industry is considerable, too. Banks reliant on the smooth running of exchanges, clearing-houses and cross-border derivatives trades will attest to that, hence their expensive planning for the worst-case scenario. And this is taking place at a difficult time for the once dull world of derivatives clearing, which has become a flashpoint between the U.S. and the EU as Brussels tries to increase its global oversight.

Plus there’s the risk to Britain’s lenders of what monetary policy the Bank of England might follow — whether we end up with a no-deal Brexit or an amicable divorce. There will be pressure to keep the money taps open to counteract any economic damage. If history is a guide, lower interest rates would lead inevitably to more margin erosion for U.K. banks.

It’s important to note that Eisman is not predicting systemic chaos. Big British banks have financial cushions such as revenues earned abroad in U.S. dollars, as well as balance sheets that can protect market share and absorb loan losses. Perhaps he has smaller listed banks in mind that are less well-prepared. As he says, the prospect of a hard-left Labour government winning power under Jeremy Corbyn is even more alarming. But as a corrective against this week’s bout of political optimism in the U.K., it’s a useful intervention.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering finance and markets. He previously worked at Reuters and Forbes.

©2018 Bloomberg L.P.