A Tesla Rival’s ‘Funding Secured’ Moment Is an Omen

(Bloomberg Opinion) -- Monday’s big news in electric vehicles: Lucid Motors Inc. secured some funding, and from Saudi Arabia’s sovereign wealth fund, no less. That may sound like a cheap joke at rival Tesla Inc.’s expense; and, yes, that can happen when your CEO conducts corporate finance over Twitter. But few seemed to be laughing Monday morning, with Tesla’s stock dropping at first.

Superficially, Monday’s announcement of Saudi money going to a rival raises uncomfortable memories of Tesla’s bizarre take-private episode. But that fiasco is almost a month old, and we already suspected the sovereign wealth fund might invest $1 billion in Lucid.

More importantly, Lucid’s funding is a reminder that Tesla has a target on its back. Tesla is still a company that — despite the drama, lack of profits, and relatively puny vehicle production — is valued at almost $50 billion. That sort of thing tends to attract competition; indeed, realizing the electrified future Tesla foresees demands it.

Lucid has an impressive pedigree. Peter Rawlinson, its CTO, was chief engineer on Tesla’s Model S, the sedan that won plaudits and turbocharged the company’s prospects back in 2012. The Lucid Air, due for release in 2020, is aimed squarely at the luxury end of the market, with an emphasis on clever design, especially in terms of using the space freed up by taking out the internal combustion engine and drive-train.

Is Lucid guaranteed to succeed? Of course not. A billion dollars certainly makes Lucid a contender; but, as Tesla’s cash burn and operational difficulties shows, launching a new car company, with a new type of car, is a tricky and expensive proposition. Still, besides Tesla and an army of Chinese manufacturers, incumbents such as General Motors Co., Volkswagen AG and Daimler AG are also either producing or developing a range of electric vehicles:

Right now, Tesla’s models face little direct competition in the U.S. from other electric vehicles in the same price range, in part because the Model 3 is still priced at a premium rather than as the $35,000 mass-market car it was originally marketed as.

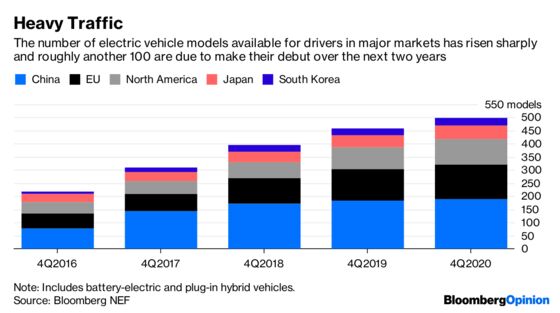

This is less comforting than it should be, though. First, the biggest growth market for electric vehicles is China, and while Tesla apparently has plans to expand there — although this sits oddly with a falling capex budget — it is a relatively minor force today.

And Tesla’s operational snafus mean it isn’t capitalizing on the current window of opportunity the way it was supposed to. Over the weekend, responding to reports of delayed deliveries and repairs, Musk declared via Twitter that Tesla had gone from “production hell” to “delivery logistics hell.” Remember, this is a company that boasted of an “exponential” increase in Model 3 output and sales. Given that production hasn’t actually lived up to that pace, how is it possible that the delivery channel isn’t able to cope with even these volumes?

If anything, that disconnect was the more pertinent thing for investors to digest on Monday. Within a couple of years, Tesla will face a much more crowded field of rivals, competing not merely for customers but also capital. Lucid’s billion-dollar check is a harbinger of what’s coming.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.