Tesla's ‘Game of Thrones’ Approach Leaves Its Audience Cold

(Bloomberg Opinion) -- At the close of trading on August 7 of last year, Tesla Inc.’s market value was $64.8 billion, its highest ever. Not coincidentally, that was also the day CEO Elon Musk claimed on Twitter that he had lined up a take-private deal worth almost $72 billion (he hadn’t). A lot has happened in the nine months or so since then, and the stock has dropped by almost half: Tesla kicked off Monday worth $29 billion less than it was at the end of that frenetic day.

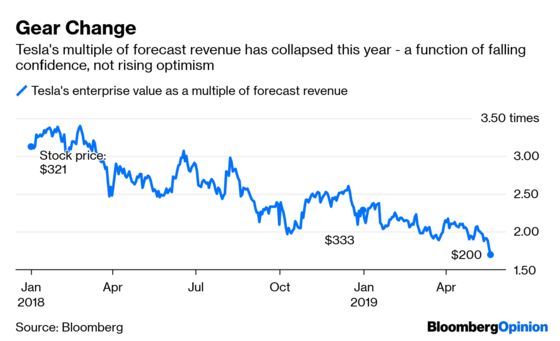

It seems weird to think a stock trading at 108 times forward earnings is suffering a crisis of confidence, but how else to characterize what’s happened in the past few months? Monday morning’s drop, taking the stock below $200 initially and to its lowest level since late 2016, was touched off by another analyst cutting their price target. Granted, it’s best not to set too much store by a target, now at $230, that was $365 as recently as 25 days ago. The consensus target is about $295, according to data compiled by Bloomberg, meaning it’s still at its richest level relative to the stock in more than three years:

What makes this especially pernicious is the timing. Tesla has spent a good deal of 2019 unveiling what ought to be zingers, only for them to be ignored. We have had the unveiling of the Model Y, the long-awaited $35,000 Model 3 going on sale, the launch of Model 3 shipments in Europe and China, plus a whole analyst day dedicated to Tesla’s ambitions in robo-taxis. Tesla even raised more cash via new equity and a convertible issue, alleviating any acute concerns on liquidity.

Part of the problem here is that, a bit like that final season of “Game of Thrones,” Tesla’s plot suddenly sped up, squeezing a lot of dramatic moves into a short period. Coming against a backdrop of repeated job cuts, zig-zagging vehicle pricing, senior people leaving, and the spectacle of Musk’s tussle with the Securities and Exchange Commission about his tweets, the effect has been jarring rather than thrilling. It is tough to maintain the image of a well-funded growth company when a company raises billions of dollars of fresh money and then tells its staff every payment going out the door will be reviewed.

High multiples on growth stocks are supposed to eventually compress as the company’s financials catch up to the hype. This actually happened for Tesla in 2018. It began that year priced at about 3.1 times forward sales (using enterprise value). It ended the year at 2.3 times, despite the stock being relatively flat, as the big increase in Model 3 sales stoked higher forecasts. Now, it trades at just 1.7 times – but that is all about falling confidence, not rising estimates.

The bull case for Tesla has rested on the assumption that Model 3 sales, especially, would rise quickly enough to let the company become self-funding. Hopes for this reached an apogee late last year. But that was before dreadful first-quarter figures made clear the growth, cash flow and profits of the second half of 2018 rested largely on pulling forward demand for the highest-priced versions of the Model 3 and slashing spending. Had Tesla sold new equity six months ago, it might have really assuaged concerns about the balance sheet and injected renewed vigor into the growth narrative. Now, it looks more like a patch for holes in that narrative.

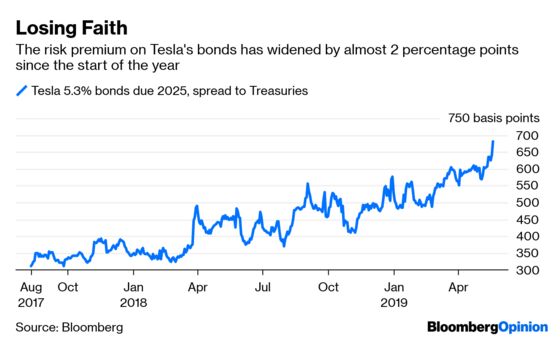

It is telling that, despite an extra $2.3 billion or so in the bank, Tesla’s bonds maturing in 2025 have sunk to their lowest price ever. Their spread to Treasuries was 603 basis points the day before the capital raise was announced. As of Monday morning, just 19 days later, that has blown out to 682 points. A bond priced at about 5.3% less than two years ago now yields a shade over 9%.

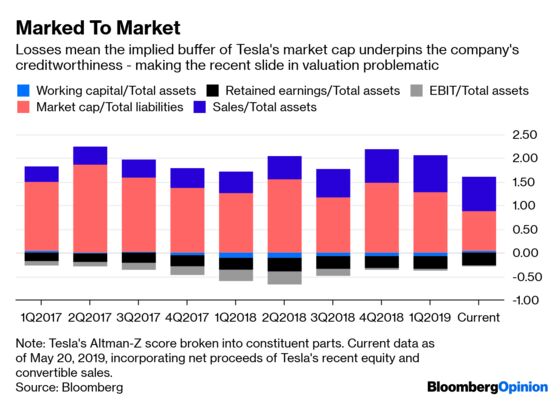

Those bonds have always been underpinned chiefly by Tesla’s high stock price, the ATM that would always give more if bondholders got nervous. You can see this in Tesla’s Altman-Z score, a weighted average of five ratios used to assess bankruptcy risk (a score of less than 1.8 is not good). Tesla’s score edged above 1.8 in the final quarter of 2018, but was back below at the end of March. Adjusted for the new funding, it is now at about 1.3 times. Breaking down the components, it’s easy to see Tesla’s market cap has been the dominant factor in keeping it even that high:

With Tesla’s financial performance and funding yet to reach escape velocity, restoring faith in the stock is critical. With so many blockbusters unveiled already, though, it’s hard to see what might turn sentiment around. As it stands, we’re about six weeks from the end of a quarter for which Tesla has ambitious sales targets already. Not too long ago, meeting these would have probably spurred even higher estimates and multiples on top of them. Now, that looks like the bare minimum to stop further selling.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.