(Bloomberg Opinion) -- Selling Tesco Plc’s operations in Thailand and Malaysia for about 7 billion pounds ($9.2 billion) would be a nice parting present from outgoing Chief Executive Officer Dave Lewis to his successor Ken Murphy. But there could be a sting in the tail from such a lavish gift. Tesco would be even more focused on its home turf in the U.K., where it’s in a merciless battle with discounters from Germany.

Tesco said on Sunday that it was carrying out a strategic review of the business, after receiving interest from potential buyers. Britain’s biggest supermarket is right to consider whether its remaining Asian operations might be worth more to a rival. Analysts at Bernstein estimate the Thai and Malay businesses could fetch between 6.5 billion pounds and 7.2 billion pounds. What’s more, with Bernstein estimating of typical transaction multiples in the region of about 13 times Ebitda, and Tesco currently trading on an enterprise value to Ebitda multiple of 7.6 times, then this unit isn’t being adequately reflected in Tesco’s valuation.

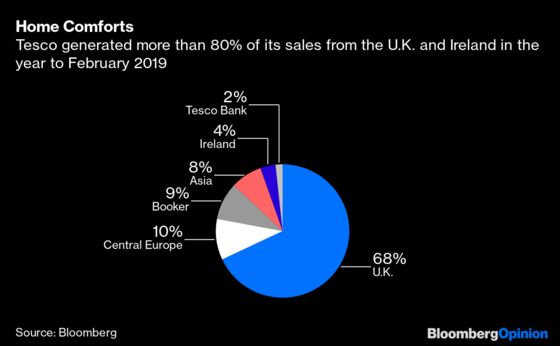

The Asian business is a highly profitable one, with an underlying operating margin of 5.87% in the year to February 2019, close to twice that at both Tesco’s U.K. and central European divisions. Selling this arm would be a further retrenchment from Tesco’s international assault of the 1990s, and leave the company focused on its core retail operations in the U.K. as well as its bank in its home market. Its only overseas outpost would be central Europe, a business it would most likely love to sell if a buyer could be found.

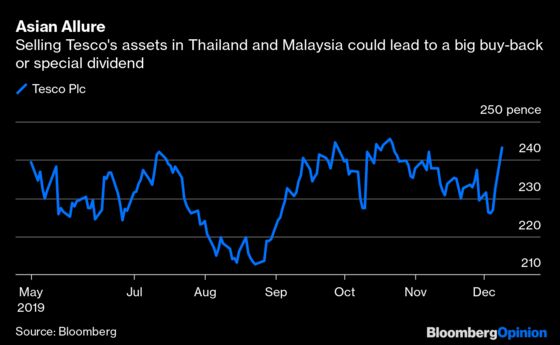

Tesco doesn’t need to offload assets to strengthen its balance sheet, in contrast to when it parted company with its South Korean business in 2015. It has been bringing down debt, enabling it to raise its dividend and generating hopes that it may soon begin returning cash to shareholders. A chunky price for the Thai and Malay units would make this even more likely. Indeed, the shares rose about 5% on Monday as investors salivated over a sizable buy-back or special dividend.

It would also provide Murphy with a war chest to slash prices. He joins Tesco from Walgreens Boots Alliance Inc., where he spearheaded an expansion in China. However he has no direct experience of the cutthroat U.K. grocery sector. Pricing is one area where Lewis could have done more. Although he made Tesco more competitive with its suite of cheaper exclusive brands, he could have tackled the problem earlier in his tenure.

With the disposal proceeds, Murphy would be able to move quickly. He needs to. The U.K. arms of the German discounters Aldi and Lidl continue to go from strength to strength, improving their premium offerings and moving into high-margin areas for the mainstream supermarkets, such as vegan food. Being able to more effectively fight the no-frills supermarkets would be helpful to the new CEO.

He would also be able to put pressure on traditional supermarket rivals, such as as J Sainsbury Plc, Wm Morrison Supermarkets Plc and Walmart Inc.’s Asda, at a time when the grocery market is sluggish. Meanwhile, some of the proceeds could be used to beef up other areas of Tesco, such as its online operations and its cash and carry arm Booker.

But prices on the shelves of its domestic supermarkets are the key driver of the retailer’s fortunes. And with an attractive Thai and Malay deal, it might just be able to get them right.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.