Elliott Has a Rocky Path to Telecom Italia Victory

(Bloomberg Opinion) -- Vivendi SA’s plans for Telecom Italia SpA haven’t quite been dealt a sucker punch by Italian regulators. But they – and billionaire Vincent Bollore, who controls the firm – certainly received a blow. The focus should now shift to the carrier’s underlying business, and it needs to do so soon.

The communications regulator said the plan, proposed by then-CEO Amos Genish last year, to separate the landline network legally didn’t go far enough to justify giving the firm an easier ride when it comes to issues like pricing. But as much as Elliott Management Corp., the second biggest investor, jumped on the decision to advocate a further-reaching divestment, the activist still has a lot to do to convince shareholders its plan is sustainable.

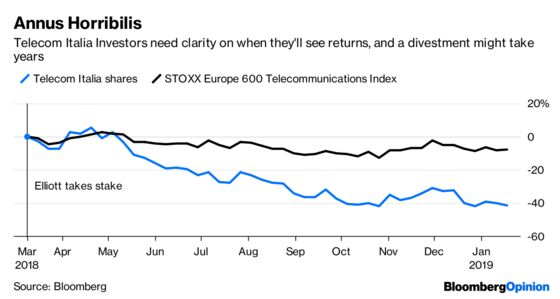

Since it built up a shareholding in the carrier almost a year ago, Elliott has been pushing for the sale of a majority stake in the network, with the expectation that at least some of the proceeds are returned to shareholders. The American firm then succeeded in getting investors to elect a board controlled by directors it nominated, who in turn pushed out Genish in December in favor of former banker Luigi Gubitosi.

Regulator Agcom said that separating the network while retaining majority control would mean Telecom Italia would still have a “significant competitive advantage.”

Team Elliott took that as ammunition – and quickly followed the announcement by declaring that Telecom Italia should separate the landline network without any further delay. The Italian state has already said it supports the hedge fund’s approach, which will combine the business with upstart rival Open Fiber SpA to create a single national network. But this would not be a panacea for all the company’s problems.

Investors can justifiably be concerned that forgoing a bidding war in favor of a single prospective partner doesn’t get them the best deal. There could be some cause for optimism that an alternative is possible: Altice Europe NV agreed to sell just under half of its French fiber network business to infrastructure investors for 1.8 billion euros ($2.1 billion) in November. While the Telecom Italia business is more complicated and unlikely to secure such generous terms, the deal shows that there are buyers for this type of asset. Whether the government would look so kindly on a different plan is another matter.

Ultimately the spinoff risks becoming a red herring. The board level fights have hurt the day-to-day business, as demonstrated by a weak set of fourth-quarter results and a 2019 outlook that fell short of analyst expectations. The focus now must turn to the operations.

During his tenure Genish was adamant that control of the network was key to Telecom Italia’s future prospects. At the shareholder meeting in March, Gubitosi will need to demonstrate he has the chops to make a success of the company without it. That should be the metric investors focus on when deciding to back the Elliott board or to revert to control by Vivendi.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.