Can Peace Break Out After This Italian Board Brawl?

(Bloomberg Opinion) -- Another chief executive officer, another strategy announcement, another pledge to focus on execution.

New CEO Luigi Gubitosi unveiled his turnaround plan for Telecom Italia SpA on Friday, less than a year after predecessor Amos Genish did the same. You could forgive shareholders for thinking they’ve heard this song before.

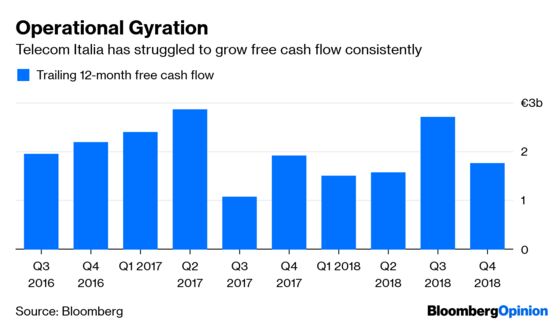

But there are some key differences which might make Gubitosi’s plan more achievable. For one, it’s less ambitious. He’s targeting cumulative equity free cash flow of 3.5 billion euros ($4 billion) over the next three years. Genish, who was ousted in November after allies of activist investor Elliott Management Corp. secured control of the board from Vivendi SA, had sought 4.5 billion euros between 2018 and 2020.

He’s also forging an alliance with Vodafone Group Plc to build next-generation 5G networks. This may include a combination of its cellphone towers arm, Inwit, with Vodafone. That seems an astute move which will curb operational and capital expenditures. In short, it's a concrete step to improve execution.

It’s nonetheless tough to assess whether Genish was indeed on track to execute his plan soundly. Elliott started building its stake in Telecom Italia just before he announced the strategy, setting off a months-long fight for control with Vivendi, the biggest shareholder, that cumulated in his ouster. That struggle was undeniably a huge distraction, and Genish was able to make little progress on one key promise: to reduce net debt. Even excluding expenditure on spectrum rights, it fell by just 2.2 percent last year.

Gubitosi aims to reduce net debt by about 13 percent over the next three years to 22 billion euros. Crucially, divestments are not needed to realize that goal – it will be funded entirely by free cash flow. That should help ease tensions with Vivendi, which opposes giving up control of its networks business.

The Italian firm is in talks to combine that business with Open Fiber SpA. Selling control of the fiber business would be a mistake, as I’ve written before, and shareholders should be wary about the valuation they are able to secure, given that pressure from the Italian government might force the firm into accepting an unfavorable deal. Ruling out any combination would nonetheless also be foolish. It could prove another way of combining efforts to save costs.

The March annual shareholder meeting looks like it will be a referendum on that deal – a vote for the Elliott slate of directors would indicate support for the divestment, and for Vivendi’s team, opposition. By excluding the deal from his financial targets, Gubitosi has taken a sensible step to placate Vivendi, and also ensured that the vote doesn’t become a referendum on his job. Given the impediments Genish faced, further management turbulence would have been detrimental for shareholders.

After a lost year, where the stock fell by a quarter, investors’ patience has already been sorely tested. Let’s hope the CEO’s plan means the company has turned the corner.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.