Taper Tantrum? Avoided. We’ll Miss You, Mario Draghi

(Bloomberg Opinion) -- European Central Bank President Mario Draghi was at the top of his game at Thursday’s governing council meeting. His performance on a communications tightrope was just enough for markets to cling to. Europe will miss him when he leaves next year.

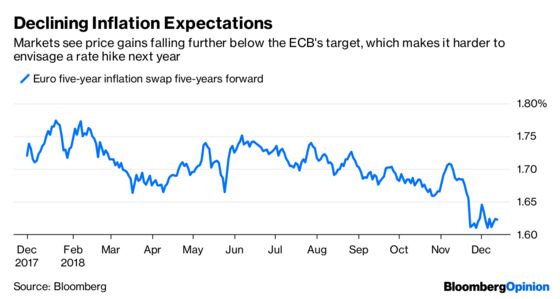

The affair was a festival of apparent contradictions. He managed to both confirm that quantitative easing would stop this year and highlight the weakening economic environment, not least from financial-market volatility, emerging-market stresses and protectionism. Officials presented downward revisions to both growth forecasts and near-term inflation projections, and the president described risks as “broadly balanced” while “moving to the downside.”

And yet, the euro weakened only modestly and German bund yields fell just slightly. Investors have faith that officials have options to ease policy were conditions were to change.

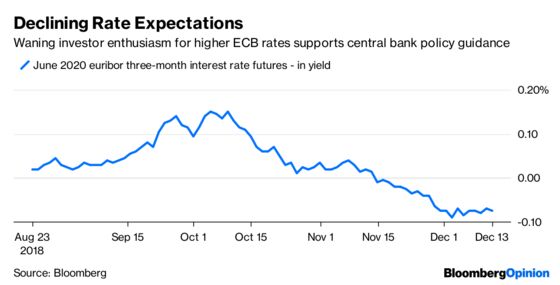

Most intriguing was Draghi’s comment that investor expectations for a rate increase in 2020 show that investors understand the central bank’s reaction function, and accept that tightening sooner could weaken the economy: “They make financing conditions easier, so we may well never get there.” He seems to be sending the message he is content with investors’ outlook, as that keeps conditions loose enough so that officials won’t have to backpedal on their decision to end QE.

It also helps that the ECB literally bought itself some more time, extending from three months to one year its window for reinvesting maturing debt. And even the insistence on sticking to the capital key — a formula which weights QE funds according to each country’s size and next year, worryingly, seems to mandate a modest reduction in redemptions getting plowed back into Italy and Spain — is already priced in.

More broadly, the 200 billion euros of European government bonds maturing over 2019 gives the council a big club to wield to tame any untoward bond yield volatility. This amounts to a significant deterrent for yields to swing around too wildly. Overall, the outlook for the region’s debt is surprisingly steady.

The president’s term expires at the end of October next year, and it is still far from certain that he will ever raise rates during his tenure. His ability to keep the markets believing that holding firm is his most powerful weapon is impressive given that he’s stopping a 2.6 trillion-euro QE program at the same time.

On Thursday, Draghi managed to avoid a taper tantrum. Investors around the world should be grateful.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.