Swiss Giant ABB Finally Does What the Hedge Fund Wants

(Bloomberg Opinion) -- ABB Ltd, the sprawling Swiss industrial giant, is lopping off its biggest limb to try to help simplify its conglomerate structure.

CEO Ulrich Spiesshofer had previously resisted demands from the activist investor Cevian Capital to separate its power grids unit, which contributes a quarter of ABB’s sales but comparatively little profit.

On Monday he capitulated, with the company saying it will sell a majority stake in the unit to Japan’s Hitachi Ltd and return roughly $7.7 billion of net proceeds to shareholders. ABB will also overhaul its complicated organization to devolve more power to its four remaining business units. That’s a significant step for a company that’s rightly accused of being too bureaucratic. Still, the shares barely budged on the news, suggesting that Spiesshofer has plenty more convincing to do.

The sale price for the power grids assets is roughly in line with what analysts had assumed. So effectively ABB investors are swapping an uncertain earnings stream for the surety of cash in 2020, when the deal closes. Because ABB isn’t very indebted, it thinks it can maintain the same level of dividend payments and its investment grade credit rating, even though the company will now be three-quarters of its previous size.

Spiesshofer is right that selling the power grids earlier would have destroyed value. Thanks to some portfolio pruning and fewer one-off financial charges, the unit’s margins have more than doubled in four years, giving ABB more bargaining power in the negotiations. It’s still the Swiss giant’s lowest margin business, though, so selling it will boost the parent’s financial return metrics.

Despite all this, ABB’s decision to sell up is a bit depressing. If the world is really going to abandon fossil fuels to tackle catastrophic climate change, it will need a massive expansion and overhaul of electricity grids in coming years. The trouble is that capital markets aren’t fond of businesses with inherently lumpy order profiles and which need lots of project financing from the parent company to win contracts.

With deep-pocked Chinese companies such as China’s State Grid hunting for business overseas, competition will probably increase too. ABB management now has one less problem to worry about. Spiesshofer thinks the leaner corporate setup should help generate $500 million in annual cost savings, implying several billion dollars of value creation. So why aren’t shareholders impressed?

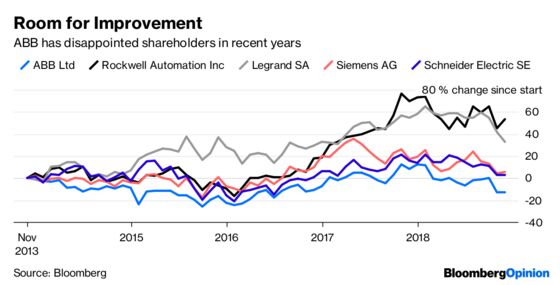

With practically every asset class in a funk right now, this isn’t a good time to be telling investors that the sun will come out tomorrow — as Spiesshofer is promising. ABB’s share price has dropped by a quarter this year, outpacing declines in the European industrial sector. Even with the structural changes, investors have many reasons to remain mistrustful.

In theory, ABB should be perfectly placed to profit from a world with more electric cars and robots. But growth has remained well below its goal of about 4.5 percent a year, and profitability isn’t best in class either. Operating margins at America’s Rockwell Automation Inc. and France’s Legrand SA are almost double those of ABB.

Spiesshofer is right that he can do better. But investors won’t believe it until they see it.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2018 Bloomberg L.P.