Surge of Inflation Isn’t a Guaranteed Portfolio Wrecker

(Bloomberg Opinion) -- Alan Greenspan, chairman of the Federal Reserve from 1987 to 2006, sent a shiver through investors last week.

In an interview on “The David Rubenstein Show: Peer-to-Peer Conversations” on Bloomberg TV, Greenspan warned that the U.S. may be poised for a period of stagflation, a rare combination of high inflation and high unemployment.

The U.S. last experienced such an episode in the 1970s and early 1980s, and the memory still haunts those who lived through it. The annual inflation rate jumped to 9.8 percent in 1980 from 2.9 percent in 1972, according to the core PCE price index, a measure of personal consumption expenditures excluding food and energy and the Fed’s preferred inflation gauge. Meanwhile, the unemployment rate swelled to 10.8 percent in 1982 from 3.5 percent in 1969, according to the Bureau of Labor Statistics.

For members of Generation X — which includes me — and subsequent generations, stagflation is ancient history. Annual inflation hasn’t topped 3 percent since 1993 and has averaged just 1.8 percent since then. And the current unemployment rate of 3.7 percent is the lowest since 1969.

Still, the implications for investors of skyrocketing inflation and unemployment come quickly to mind. According to lore, a surge in inflation would lift interest rates, causing bond prices to decline and thereby wrecking bond portfolios. Higher interest rates would also thump stock prices because future corporate earnings would be worth less when discounted at higher rates. And all of that would come when many investors would lean on their savings to offset higher living costs and possible bouts of unemployment.

It’s not clear, however, how much of that received wisdom is reliable. Yes, when inflation creeps up, interest rates tend to follow. The correlation between annual inflation and the yield on 10-year Treasuries has been strongly positive (0.76) since 1959, the first year for which numbers are available for the core CPE price index. (A correlation of 1 implies that two variables move perfectly in the same direction, whereas a correlation of negative 1 implies that two variables move perfectly in the opposite direction.)

But that hasn’t translated into any meaningful relationship between inflation and returns from long-term government bonds over the last six decades. The correlation between the two was weak over rolling one-year (-0.07), three-year (-0.11), five-year (-0.08) and 10-year periods (-0.10). In other words, when inflation picks up, it’s anyone’s guess how bonds will perform.

Stocks were no different. The relationship between inflation and total returns for the S&P 500 Index has also been tenuous. Here again, the correlation was weak over one-year (-0.06), three-year (-0.04), five-year (-0.02) and 10-year periods (0.12). It’s not safe to assume that rising inflation will rattle stocks.

It’s not even clear that stocks and bonds fare meaningfully worse after adjusting for inflation. The correlation between inflation and real returns for the S&P 500 was slightly stronger but still weak over one-year (-0.19), three-year (-0.26), five-year (-0.29) and 10-year periods (-0.24).

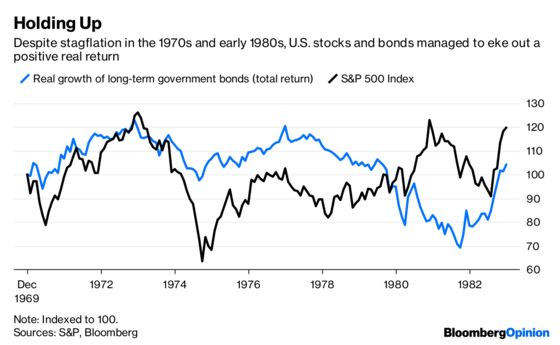

So even if inflation were to rise to alarming levels, that doesn’t necessarily mean stocks wouldn’t keep up. In fact, as stagflation intensified from 1973 to 1982, real returns for the S&P 500 averaged a negative 0.2 percent over rolling one-year periods, 0.4 percent annually over three years and negative 0.4 percent annually over five years. Not bad, considering that the period includes the 1973-1974 stock market crash, one of the worst on record.

Real returns from bonds have had more trouble keeping up with rising inflation, but here, too, heartburn is far from certain. The correlation between inflation and real returns from long-term government bonds was weak over one-year periods (-0.26), although it strengthened over three-year (-0.43), five-year (-0.45) and 10-year periods (-0.53).

It makes sense that bonds have a harder time fighting off inflation than stocks. Inflation means that the prices of many companies’ goods and services are rising, along with the cost of producing them. Corporate earnings — and by extension stock prices — should therefore reflect changes in inflation. Bonds lack that flexibility, particularly longer-term bonds with fixed rates.

Even so, the period from 1973 to 1982 was not disastrous for bond investors. The real return from long-term government bonds averaged a negative 2.3 percent over one-year periods, negative 2.6 percent annually over three years and negative 1.9 percent annually over five years.

There are lots of reasons to worry about stagflation and do everything possible to avoid a replay of the 1970s. But a sure meltdown of investors’ portfolios isn’t one of them.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2018 Bloomberg L.P.