(Bloomberg Opinion) -- The beginning of 2019 has seen a “risk-off” flight into high-quality government bonds. But the resulting super-low yields probably won’t stay like this for long. They’ll make it too tempting for governments to issue as much paper as possible. And this won’t just apply to large-scale syndicated bond deals, but to higher-risk longer maturities as well.

This yield collapse is a global phenomenon driven by a 40 basis point shift lower in U.S. Treasuries over the past quarter. Europe has followed, although not quite in lockstep. The 10-year bund yield is sitting near its April 2017 level of 15.6 basis points. Going below that would portend a shift back into the negative territory seen between June and October 2016.

Germany is far from alone. The rest of the core European countries have followed suit — especially U.K. gilts. While Italy is the standout performer, that’s largely due to the resolution of its budget spat with the EU.

But the flood of long-maturity supply coming down the pipeline may well turn the tide. At these rates, it’s almost inevitable that European countries would want to take advantage and get a head-start on their annual issuance needs.

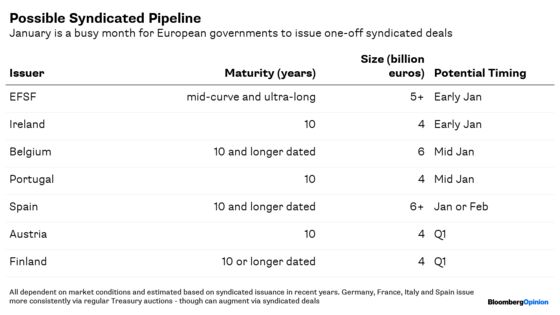

Ireland is normally first off the mark in January, with a 10-year syndicated deal for about 4 billion euros. Portugal, the Netherlands, Austria, Belgium and Finland are pretty sure to be close behind on one-off syndicated deals, and some may even take a chance on getting ultra-long maturities away. The European Financial Stability Facility, Europe’s bailout vehicle, has already signaled plans for a new bond next week.

And with yields this compressed, why not? In January alone, Germany is scheduled to issue 7 billion euros of 10-year notes (in two slugs) and 1.5 billion euros of 30-years. France, Spain and Italy aren’t going to miss out on the action. They all have plenty of regular auctioned supply on the calendar this month, and the temptation will be to sell more than usual if demand is sustained. One-off syndicated deals — particularly for longer-dated maturities — are also quite likely over the first quarter.

It looks like a lively start to the New Year as lower yields meet their match in bumper supply.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.