(Bloomberg Opinion) -- Nik Storonsky, the Russian-born co-founder of Revolut Ltd, has been setting the record straight on a lot of things lately. His $1.7 billion money-transfer app has been hitting the headlines for all the wrong reasons: Regulatory scrutiny over an alleged compliance lapse; the departure of its finance director; suspicions of Russian political interference; and a toxic work culture.

The famously blunt executive, a champion swimmer who boxed as a child, has reassured customers and staff that there was no compliance lapse, that the CFO’s exit was to make way for someone more experienced in global banking, and that any corporate-culture issues are firmly in the past. And that his ties to Russia are irrelevant and inaccurate.

Yet there are more fires to fight. Revolut on Tuesday rebuffed a report in the Financial Times that said London’s Metropolitan Police force was conducting a fraud investigation into an apparently botched money transfer. A company spokesman said the police weren’t investigating any fraud case involving Revolut and that it had never been in control of the funds concerned.

Still, the report wasn’t a great advertisement for Revolut’s service for business customers, a division that has grown at breakneck speed and is seen by Storonsky as a central plank of the app’s “money-making” product range — alongside cryptocurrency trading and premium cards.

Revolut seems to be suffering from the consequences of what happens when investors throw large amounts of money at a crop of startups in a high-risk industry with lots of red tape. The expectation is for super-charged growth, but it’s a challenge to keep regulators happy when you’re going this quickly.

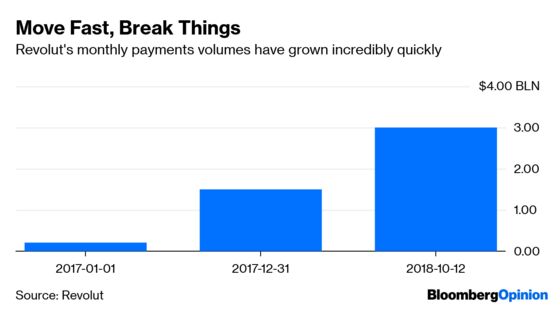

Revolut is certainly delivering the growth. In 2017, its customer numbers trebled to 1.2 million, revenues increased five times to 12.8 million pounds ($16.8 million), and monthly transaction volumes jumped to $1.5 billion from $200 million. But the cost of that expansion still isn’t clear. High staff turnover and a business model reliant on “process-driven machines” is potentially a dangerous mix.

A tool aimed at enforcing regulatory compliance resulted in too many false positives, and annoyed customers, so Revolut dropped it. But that has brought attention from the U.K.’s Financial Conduct Authority. Storonsky insists no regulation was breached, but the episode raises questions about the company’s priorities.

Despite the high values of fintech startups, there are still concerns about the sustainability of their business model. They need to undercut the big banks on price, while trying to make sure they provide the same level of security to customers.

Storonsky told Bloomberg Television last year that Revolut was targeting the U.S., India, Australia, Canada, Singapore and Hong Kong. That will require more money, more staff and more regulatory boxes to tick. It’s the latter that poses particular concern. Revolut is now a licensed bank in Europe, via a license granted in Lithuania, a country that is trying to take extra measures to cope with the very real threat of money-laundering. Revolut may be small still, but it’s already a part of the global system of money transfers, so compliance is crucial.

The co-founder’s focus has long been about driving fast. “If you want a product to be sold in huge quantities with zero marketing it has to be 10 times cheaper and 10 times better,” Storonsky said last year. Now it should be about driving safe.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering Brussels. He previously worked at Reuters and Forbes.

©2019 Bloomberg L.P.