(The Bloomberg View) -- Of all the much-debated causes of the 2008 financial crisis, there’s one on which almost everyone agrees: U.S. homeowners took on debts that would have been affordable only in an improbably benign world. Ten years later, according to a recent report by Bloomberg News, many of the largest U.S. corporations are getting into a similar predicament.

It’s too early to say whether the rising indebtedness will lead to another financial disaster. But one thing is certain: There’s no good reason for the government to encourage it.

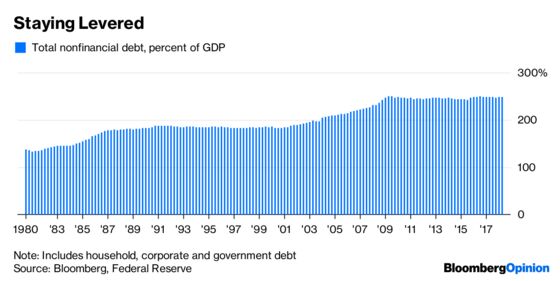

Debt has played a central role in just about every financial debacle in history, from the Dutch tulip mania to the euro crisis that, judging from developments in Italy and Greece, has yet to reach its denouement. It’s thus troubling to see that total U.S. nonfinancial obligations, and their corporate part in particular, are larger as a share of economic output than they were in December 2007, just ahead of the last crisis.

A Bloomberg analysis of the 50 largest corporate acquisitions of the past five years offers ominous detail. It found that more than half the companies ended up with levels of debt — or leverage — that would put their credit ratings in junk territory, were it not for the optimistic assumptions of ratings firms. In other words, if things don’t go as well as expected, some $1 trillion in debt could drop into a junk market that is already overextended in its pursuit of yield. The potential result: a freeze that could force many businesses to fold as they fail to pay or refinance their debts.

To some extent, debt follows a cycle of optimism and pessimism rooted in human nature. But the government abets it. The tax code pushes homeowners and businesses to take on more debt by providing breaks on interest payments. Lenders get additional subsidies in the form of deposit insurance and other government support, and regulators encourage them to take advantage by allowing banks to operate with thin layers of equity capital. The Trump administration has made the problem worse by reversing regulators’ efforts to curb some of the riskiest lending.

The answer is simple: Stop subsidizing debt. Last year’s tax reform (for all its flaws) took a step in the right direction by limiting the mortgage-interest deduction. Congress should go further by eliminating it, along with the preferential treatment of corporate debt. Also, requiring banks to operate with more equity — particularly at this point in the credit cycle — would curb subsidies and reduce incentives to lend indiscriminately. At the very least, regulators should refrain from giving the green light to excessive leverage.

Given the Trump administration’s own fondness for debt — witness the government’s surging budget deficits — don’t expect decisive action any time soon. But you can count on one thing. The more leverage there is, the more fragile the economy will be when the next downturn comes.

Editorials are written by the Bloomberg View editorial board.

©2018 Bloomberg L.P.