Stop Blaming the Trade War for Everything

The catch-all excuse for the global economy’s ills has merely amplified or accelerated existing trends.

(Bloomberg Opinion) -- The trade war needs to fire its PR team.

The tussle between the U.S. and China is being blamed for all manner of economic and financial developments. Some of these are only vaguely related to the tariff spat, or they reflect trends underway before U.S. President Donald Trump ever heard of his Chinese counterpart Xi Jinping. In other areas, like monetary policy, the conflict alters timing, not outcomes.

The latest demon is the prospect of a recession, which was said to be responsible for sliding stocks and diving bond yields Wednesday. The culprit? You guessed it: the trade war. But handicapping a recession has been a favorite game of market commentary every few months for the past two years. America’s expansion is almost 10 years old; it’s long in the tooth, tariffs or not.

China's economy was already in a long-term slowdown, exacerbated by a crackdown on debt that's been driven by domestic policy choices, not the White House. The country is shifting to an economic model less dependent on exports and cheap low-end manufacturing. By 2016, incomes in China had already reached the level where Japan, South Korea and Taiwan started shifting production abroad decades earlier, according to an International Monetary Fund report.

The general vibe at the 31st Singapore Economic Roundtable this week was that discord between Washington and Beijing was amplifying existing phenomena or underscoring transformations already in train. Rarely was the clash seen as the sole catalyst. (My Bloomberg Opinion colleague Tim Culpan recently argued that some firms are using tariffs as a long-sought excuse to reduce their China footprint.)

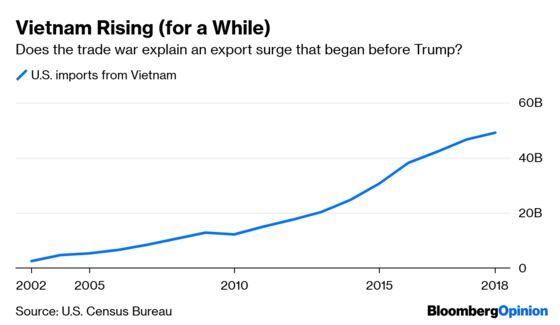

One place that’s shown some trade-war PR wizardry is Vietnam. The country continues to get buzz as the next great U.S. trading partner, having been declared at least a relative winner from the tariff conflict. Exports to the U.S. have increased, but it's hard to determine how much of this reflects the vibrancy of the American economy and how much the ballyhooed upending of the supply chain.

I'm skeptical that many manufacturing operations have shifted outright from China. More likely, as one former Western diplomat in Asia related to me, Vietnamese factories will get extra shifts and possibly some additional capacity. Shutting plants in China and moving all that stuff to Vietnam, purely in response to tariffs, is a big call. To the extent that anyone is doing that, few want to talk about it. Beijing's enmity isn't worth it.

In the arena of central banking, the erosion of investor confidence and risk-off mentality may delay some decisions to cut interest rates. It won't thwart reductions indefinitely. The same trend toward too-low inflation that preoccupies Western thinking is present in Asia. Two countries where cheaper money looks like a given are South Korea and Indonesia.

In the former, whose economy shrank last quarter and which shows zero upward price pressures, rates should have been cut already. A tumble in the won makes the Bank of Korea more hesitant to proceed, but it’s sure to do so before year end. The country's slowdown is too steep to credibly argue otherwise.

Indonesian policy makers have walked back their hawkish language, after following the Federal Reserve higher in 2018. The one hurdle in Bank Indonesia's way is its commitment to stability. In reality, the central bank means the current-account deficit is too great to risk a run on the currency. Officials aren't saying there will be no cuts. The stance has evolved to “cautious neutral.” Most economists see reductions before year-end.

Not even tariffs will prevent that rendezvous with reality.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.