Fears Are Overtaking Facts in Market Sell-Off

Investors seem to be searching for a reason to sell. That’s a big sentiment shift from just a few months ago.

(Bloomberg Opinion) -- Putting your finger on what’s spooking the market in the past week or so has been difficult.

The recent sell-off appeared to be launched by fears of rising interest rates. When rates stopped rising, trade tensions were the new No. 1 concern. But on Tuesday morning, the announcement that Donald Trump would meet with China’s Xi Jinping at the upcoming G-20 summit to discus trade didn’t calm markets. Instead, worry appears to have settled on the idea that we have hit peak profits, fueled by a warning from Caterpillar Inc. on Tuesday morning. A low unemployment rate and resurgent inflation, along with price-raising tariffs, will slice into bottom lines even if the economy continues to expand, is how the theory goes.

The problem with proffering a profit pinnacle is proof. For the third quarter, 70 percent of all companies that have reported so far have announced higher profit margins than a year ago, according to FactSet. Even after adjusting for lower tax rates, profits margins are up again. That’s led to reports of higher-than-expected earnings for the third quarter, once again, with earnings-per-share for the S&P 500 now on track to increase 22 percent from a year ago. And this isn’t the first time Caterpillar has warned about peak profits. They did after the first quarter and margins have continued to rise since.

What’s more, worrying that profit margins are historically high and have to revert is a fear that goes back to the early days of this bull market. More recently, even some top investors like Jeremy Grantham, who is typically bearish, have argued that a combination of factors — including globalization and consolidation — may keep profit margins from being squeezed. Indeed, current analysts’ expectations based on the profit projections of the companies in the S&P 500 envision stable margins through next year. That might not be great for workers looking for raises, but it shouldn’t worry investors.

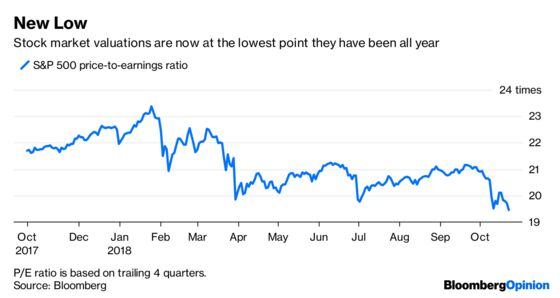

What is worrying is that investors seem to be searching for a reason to sell. That’s a big sentiment shift from just a few months ago, when even bad news didn’t seem to dent the market that much or for that long. And a falling stock market itself can do some real economic damage. Earlier this week, Goldman Sachs warned that a falling market could soon be a drag on the economy. But the two things that usually sink the market, recessions and overly rich stock valuations, don’t appear to be something investors should be concerned about. The price-to-earnings ratio of the S&P 500 has fallen to 16.5 based on this year’s earnings, below its five-year average.

Here’s the thing, though: In every sell-off, eventually fears are replaced with facts. The facts suggest that should happen well before any real damage to the economy is done.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.