(Bloomberg Opinion) -- The market for initial public offerings had been giving off warning signals long before this week’s rout in global stocks. The two are connected — and the human investors had a lead over the robot traders.

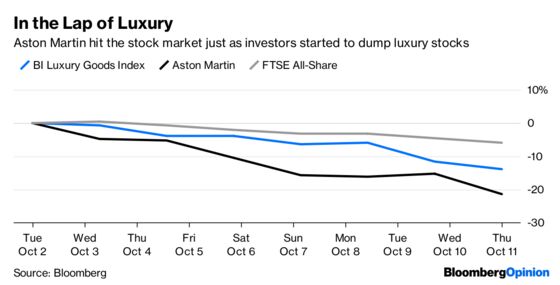

London saw two big IPO disappointments which happened to be divisive stocks with strong bear cases. Online lender Funding Circle Holdings Plc, down nearly 15 percent since going public, is untested in an economic downturn. The valuation of Aston Martin Lagonda Global Holdings Plc assumes the carmaker can flawlessly deliver on its promise to ramp of volumes without losing its luxury cachet. Just as a car plummets in value the moment it’s driven out of the showroom, the stock has sunk around 20 percent.

The vulnerabilities in the two deals only exacerbated an underlying sense of unease about the market. Aston drove full speed into a broader sell-off in the global luxury sector. There were investors in both IPOs who had zero staying power and got out as soon as they started losing money. That probably says something about the character of the London new issues market. But even now, low trading volume suggests buyers for Aston are few and far between.

LeasePlan Group NV, a fleet car operator, announced its plan to list in Amsterdam with great confidence the day after Aston’s poor debut. This week it pulled the deal, blaming market conditions.

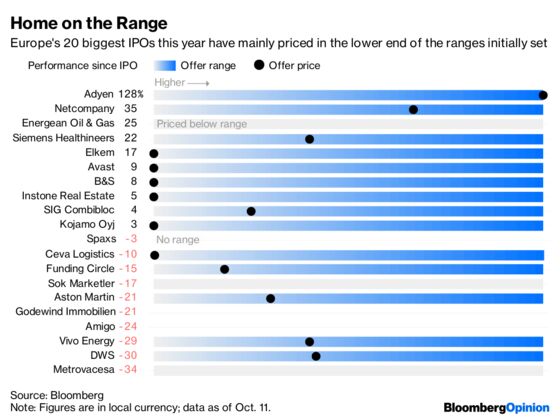

It has been a tricky year for European IPOs. Among the region’s 20 largest deals, most priced in the lower part of their price ranges. Half are underwater (most of the U.S. top 20 are up). Of those that have fared well, a majority priced right at the bottom of the range. Several of those that priced above the floor got punished later.

IPO price ranges are set according to very early feedback. The recent trend suggests that when investors indicate their generosity threshold, they really aren’t bluffing.

Against that backdrop, German train brake maker Knorr-Bremse AG looks brave to have priced its shares at about the middle of its range on Wednesday ahead of its debut today. It is a unique European play on Chinese rail growth, and U.S. peers provide a comforting valuation benchmark. Knorr looks like it could be the exception. We’ll see.

The stock market comprises different groups — machines, passive and exchange-traded funds, hedge funds and long-term, long-only shareholders. Not all of them are human: some just latch on to the prevailing trend in the market. IPOs are where real investors show their appetite for risk. The new issues window appears to be slamming shut and wasn’t open very long. A deeper malaise may be setting in.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2018 Bloomberg L.P.