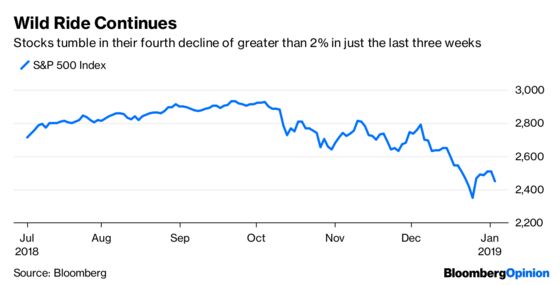

(Bloomberg Opinion) -- When Apple Inc. dropped a bomb after the official close of trading Wednesday that its revenue would fall short of estimates because of softness in China, many cynics snickered. Everyone knew China’s economy was slowing, so blaming the Asian nation for a setback was just a convenient excuse to mask a deteriorating business, like when retailers blame the weather for a slump in sales. Now, 24 hours later, Apple’s explanation looks a little more plausible in a distressing sign for equities, with the S&P 500 Index tumbling 2.48 percent Thursday.

Apple’s announcement probably would have had only a short-term negative impact on equities, with traders coming around to the idea that Apple’s problems were of its own making if not for a disappointing manufacturing report Thursday morning from the Institute for Supply Management. Its December index of new orders — a key leading indicator of future activity — fell to a level that barely registered as growth. Furthermore, many survey respondents noted tariffs and the resulting higher prices were hurting their businesses. In other words, the headwinds challenging markets are both macro and micro in nature. That’s disconcerting because it takes a major leg out from under the bull case for stocks, which was that the economy may be slowing but at least earnings growth for 2019, forecast to be just more than 8 percent, would still be respectable. Even the ever-optimistic Trump administration is beginning to doubt the outlook for earnings. Kevin Hassett, the chairman of the White House Council of Economic Advisers, basically advised investors to go to the mattresses when he told CNN Thursday that “It’s not going to be just Apple” and that “there are a heck of a lot of U.S. companies that have sales in China that are going to be watching their earnings being downgraded next year until we get a deal with China.”

Although markets may be signaling that a recession hits the U.S. this year rather than 2020 as expected, it’s hard to believe that any slowdown will be that severe given the actions of consumers, who account for two-thirds of the economy. Despite the S&P 500 plunging 9.18 percent in December for its worst month since 2009, analysts are saying retail spending during the holiday season was the most robust in 13 years as Americans basked in a hot jobs market. Also, given how pessimistic investors have turned toward the outlook for corporate earnings, anything close to companies meeting expectations when they begin to report fourth-quarter results could be a boon for equities.

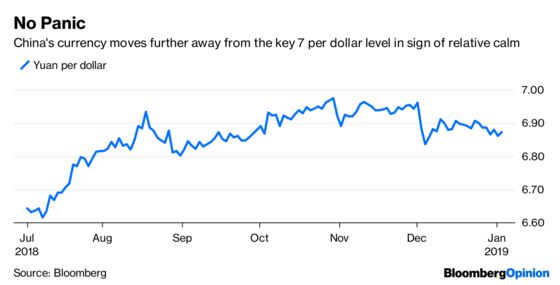

CHINA’S YUAN SHRUGS

Given the reaction to Apple’s announcement, one might think that China’s economy was about to collapse. And while growth is rapidly decelerating, and one recent measure showed that its manufacturing sector is contracting, one key indicator is sending a rather benign signal. The yuan was little changed Thursday at 6.8721 per dollar, comfortably below its weakest level of last year of 6.9799 per dollar in late October and moving further away from the psychologically important 7 per dollar level, which many investors and strategists said would most likely spark a flight of capital from China when breached and throw global markets into a tailspin. Overall, currency markets are relatively calm despite several “flash crash” type moves in key crosses immediately after Apple’s warning. At 9.40, the JPMorgan Global FX Volatility Index may be at its highest since April 2017; it was well above 12 in 2016 and above 16 in both 2010 and 2011. It’s not that far off its five-year average of 8.91. To put that in context, the CBOE Volatility Index, or VIX, of U.S. stocks was 24.50 on Thursday, far above its average of 14.90 over the past five years. The relative calmness among currency traders may be a sign that they don’t believe that leading central banks will be able to extricate themselves from global financial markets as quickly as thought because of the economic slowdown.

GOLD’S NOT SO IMPRESSIVE RALLY

Many market participants are pointing to the gold market as proof that anxiety over the global economy is justified. After all, prices for one of the ultimate market havens spiked 5.08 percent in December in their biggest monthly rally since November 2016. But taking a step back, at about $1,300 an ounce, prices for the precious metal are only at their highest since June. Over the past five years, prices have ranged from as high as almost $1,400 an ounce in March 2014 to as low as about $1,050 in December 2015. Such a muted move in gold suggests that perhaps its recent popularity may not be due solely to investors seeking a haven from lasting global market turmoil. The thinking here is that because gold pays no interest, its appeal diminishes when interest rates are rising, and that’s why bullion had tumbled from almost $1,400 as recently as April to less than $1,175 in August as the Federal Reserve was raising rates. But with the Fed sending some dovish signals of late and the market pricing in the possibility of a rate cut by the end of the year, bullion’s appeal has been rising. Recent data from the U.S. Commodity Futures Trading Commission show money managers’ bullish bets on gold outnumbered their bearish wagers for the first time in five months. A survey by Bloomberg News found that traders and analysts remained bullish for an eighth week, with nine forecasting further gains, three expecting declines and three being neutral. “2019 is already getting off to a volatile start and we expect to see the political and economic uncertainty of 2018 continue and deepen,” Mark O’Byrne, a research director at GoldCore Ltd., told Bloomberg News.

BOND TRADERS GO WILD

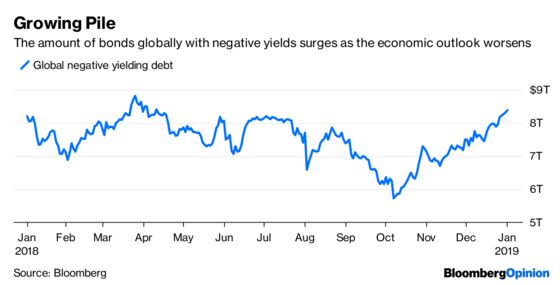

It looks as if the last of the bond bears is capitulating. Yields on two-year Treasuries cratered Thursday, falling about 10 basis points as prices of the securities soared. At 2.38 percent, the yield is not only down from last year’s high of 2.97 percent in early November, the yield is even below the Fed’s target of 2.50 percent for the federal funds rate. That’s a sure sign that bond traders expect the central bank to cut rates sooner rather than later as economic growth slows, with some saying a reduction could come late this year. “The market is pricing in recession no matter what — the market has priced it in,” Jeff Carbone, managing partner at Cornerstone Wealth, told Bloomberg News. “Now to what extent and when? That history hasn’t been written yet.” The move isn’t just a U.S. phenomenon. The yield on the Bloomberg Barclays Global Aggregate Treasuries Index, which tracks $21.2 trillion of sovereign government debt worldwide, has fallen to 1.32 percent, the lowest since May. “It’s the proverbial ‘Don’t step in front of the moving trend’ environment,” Marty Mitchell, an independent strategist who’s been charting Treasuries since the 1980s, told Bloomberg News. “You’d be jumping in front of it at your own peril” if you wanted to bet against bonds at the moment, he added. Investor demand is so great that the amount of debt with negative yields has grown to $8.29 trillion from $5.73 trillion in October, a separate Bloomberg Barclays index shows.

MEXICO’S CREDIT RATING IN DOUBT

Citigroup Inc. on Thursday released the results of its survey of clients on their outlook for emerging markets in the first quarter, and the news isn’t good for Mexico. The big takeaway is that 40 percent of respondents expect Mexico may lose its investment-grade credit rating by next year. They also rank Mexico as their biggest “underweight” in emerging markets, followed by Russia and China. Even officials in Mexico are worried, with a central bank board member saying Thursday that the nation’s credit rating is at risk, which “would lead to higher financial costs for public debt,” according to Bloomberg News’s Nacha Cattan. Newly implemented austerity measures, which will lower public spending and result in the departure of experienced government officials, are other risks being monitored by the bank, added the unidentified board member in minutes of the latest interest-rate decision. Mexico’s stock market significantly underperformed the broader emerging market last quarter, with the benchmark Bolsa IPC index falling 16.5 percent compared with a decline of 7.72 percent for the MSCI EM Index. Mexico is rated three levels above speculative grade, or junk, by both S&P and Fitch, and four levels above junk by Moody’s.

TEA LEAVES

Friday brings two events that have the potential to drive markets for the next few weeks. First, the government will release its monthly employment report for December. The median estimate of economists surveyed by Bloomberg is for a gain of 181,000 of nonfarm jobs, up from the 155,000 that were created in November. The top-ranked interest rates strategists at BMO Capital Markets pointed out in a research note Thursday that 12 proxies they track are slightly positive, with six suggesting an upbeat report and five flagging a downbeat report. That’s the opposite of what BMO’s indicators were flagging heading into the November report, which came in weaker than forecast. Less than two hours later, Fed Chairman Jerome Powell takes part in a joint interview with his predecessors Janet Yellen and Ben S. Bernanke at the annual meeting of the American Economic Association in Atlanta. The event may give Powell the opportunity to expand upon some of the remarks he made at his press conference after the Fed’s decision to raise interest rates on Dec. 19. The markets were disappointed that Powell didn’t seem too concerned about the turmoil in markets at the time, which led to a further sell-off in equities and a rally in Treasuries.

DON’T MISS

Is Warren Buffett Sending a Signal About Bonds?: Brian Chappatta

The Yen-Inspired ‘Flash-Crash’ Is an Ugly Omen: Marcus Ashworth

Apple! Trump! Utilities Offer Safety — for a Price: Liam Denning

This Developing-World Star Looks Pretty Tarnished: Mihir Sharma

Matt Levine’s Money Stuff: Computers Are Sorry for Flash Crashes

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.