(Bloomberg Opinion) -- Are you interested in receiving John Authers' newsletter in your inbox? Please subscribe at this link.

The Reflex, as 1980s new wave and synth-pop band Duran Duran sang, is a door to finding treasure in the dark. Anyone who was long the market, or particularly momentum stocks, would have profited hugely from this dictum on Tuesday.

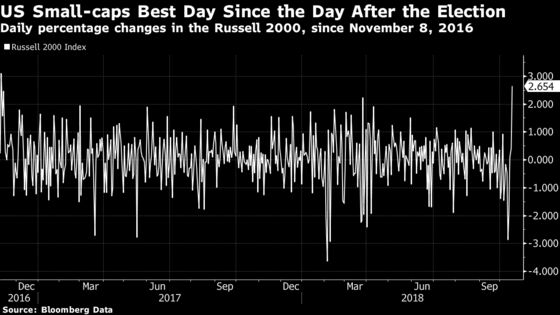

After last week’s sharp sell-off just before earnings season kicked off, Tuesday offered the opportunity to enjoy a rebound, which traders, particularly in the U.S., fully enjoyed. The Russell 2000 index of smaller companies turned in its best performance since the day after the U.S. presidential election in November 2016, rising 2.82 percent.

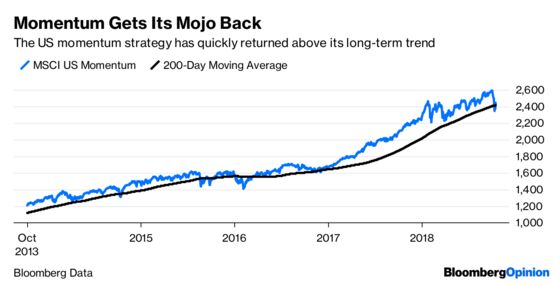

Momentum itself, which is a style of investing that involves buying stocks that are trending higher and shedding losers, was a prime beneficiary of the broad rebound. MSCI’s US Momentum index, which had lost 10 percent in only seven trading days, clawed back more than a third of its losses. It is now back above its 200-day moving average, a popular measure of the long-term trend, after spending what felt like the blink of an eye below it:

And that was before Netflix Inc.’s positive earnings report following the regular close of trading sent the ultimate momentum stock of the moment up by as much as 15 percent in after-hours trading. That should give momentum investors a further push Wednesday.

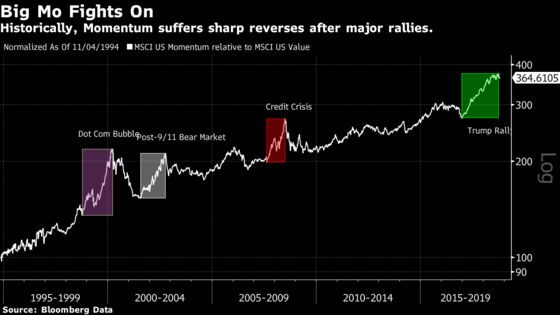

In longer context, however, the strength of momentum is beginning to look anomalous. The chart below shows how MSCI’s US Momentum index has performed compared to MSCI’s Value index, which is made up of stocks that look cheap based on fundamentals such as price-to-earnings ratios, going back to the start of the indexes in 2000. Clear patterns emerge:

Momentum has beaten value comprehensively and consistently this century. Any number of changes in market structure might help to explain this, with both easy monetary policy and the rise of exchange-traded funds popularly cited as reasons for the strength in momentum investing. But this has not been a totally free lunch.

Both the last two times momentum staged a rally of this scale, it then behaved like a cartoon character that had stepped on a rake, and juddered down again. That, in general, is the reason why momentum pays. But when it doesn’t pay, it can lose investors a lot of money in a hurry, and it can be difficult to get out in time. The last two momentum spikes overlapped with important points in the market. The 2002 momentum rally reversed when the S&P 500 Index finally made a low and began the rally that would end with the financial crisis. In 2008, the momentum rally was driven by the bull market in oil, combined with collapsing confidence in bank stocks, and terminated abruptly a few weeks before the Lehman Brothers Holdings Inc. bankruptcy when traders realized that they had taken oil prices to an infeasible level.

And this time time around, momentum appeared to have its date with destiny, but after a muted sell-off – by the standards of those who tie their fortune to the hottest stocks of the moment - it has recovered. The momentum index is back above its 200-day moving average. So is the relative performance of momentum to value.

This is unnerving. Bloomberg News macro strategist Cameron Crise wrote a post Tuesday positing that “Equities May Be Rallying Too Hard to Be Bullish.” There is something to this. A sharper and more purgative fall would have been more reassuring. With President Donald Trump still anxious about the level of the stock market, and angry with the Federal Reserve, it might make sense for him to ask the central bank to amplify its hawkish rhetoric. That might deliver the needed healthy correction.

Less flippantly, the problem remains. Uncertainty persists. Every little thing the reflex does leaves you answered with a question mark.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

John Authers is a senior editor for markets. Before Bloomberg, he spent 29 years with the Financial Times, where he was head of the Lex Column and chief markets commentator. He is the author of “The Fearful Rise of Markets” and other books.

©2018 Bloomberg L.P.