Stocks Are Sounding the Alarm on Earnings

(Bloomberg Opinion) -- The U.S. stock market is warning investors about earnings, and it’s time to pay attention.

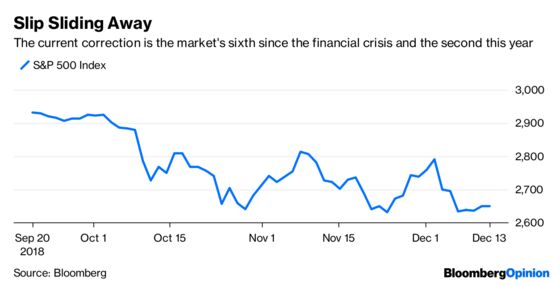

The S&P 500 Index slipped into a correction on Dec. 7. It ended the day down 10.2 percent from its recent peak on Sep. 20, breaching the 10 percent decline that customarily marks a correction. The index is little changed this week through midday Friday.

Investors are comforting themselves, as they have all year, with reassurances about strong fundamentals. According to estimates compiled by Bloomberg, Wall Street analysts expect earnings for the S&P 500 to grow by 12 percent in 2018 and by an additional 9 percent in 2019. That’s well above the average growth rate of 4 percent a year since 1871, according to numbers compiled by Yale professor Robert Shiller.

It’s false comfort, however. As I pointed out in May, declines in the stock market most often precede slumps in earnings rather than the other way around. And this would be a particularly bad time for earnings to disappoint. Stock prices have rarely been as vulnerable to a downturn in earnings as they are today. If the market decides that the earnings outlook is too rosy, the recent sell-off could get a lot worse.

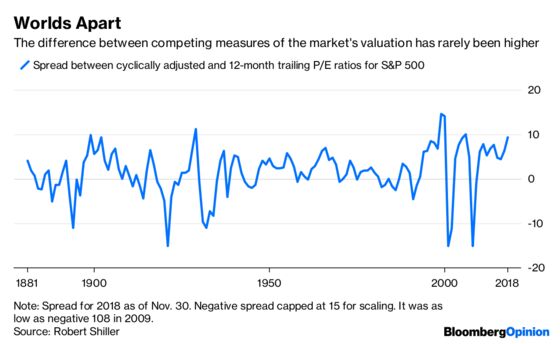

Consider the impact of earnings on the market’s valuation. The S&P 500’s price-to-earnings ratio based on analysts’ expected earnings for 2018 is 16, which is roughly in line with the long-term average. Using 12-month trailing earnings, however, the P/E ratio jumps to 20. And using cyclically adjusted earnings, or 10-year trailing average real earnings, the P/E ratio jumps to 29.

If those seem like big differences, that’s because they are. The spread between the cyclically adjusted and 12-month trailing P/E ratios has only been higher twice since 1881 — on the eve of the Great Depression in 1929 and just before the dot-com bubble burst in 1999. And since 1990, the first year for which analysts’ estimates are available, the spread between the cyclically adjusted P/E ratio and the one based on 12-month forward earnings was only higher around the dot-com bust.

The reason for the wide disparity is that earnings have grown faster than usual in recent years, as they did in the 1920s and 1990s. Earnings climbed back to their pre-2008 financial crisis high in July 2011. Since then, they’ve grown 6.3 percent a year, or more than 50 percent faster than their long-term average growth rate.

That pace isn’t sustainable. Earnings are just one component of GDP growth, so they can’t grow faster than the economy indefinitely, and no one expects it to grow that fast.

This is where cyclical adjustment is useful. By averaging earnings over a full business cycle, it reveals whether and to what extent earnings have deviated from a sustainable long-term path, deflating earnings during peaks of the cycle and propping them up during troughs.

For example, when earnings per share for the S&P 500 peaked in June 2007 at $85, the cyclically adjusted earnings were $67. The latter turned out to be a better assessment of the health of earnings, as they were $51 a year later. Similarly, earnings cratered to $7 in March 2009, whereas adjusted earnings were $68. Here again, the adjustment proved to be the better estimate, as earnings recovered to $61 a year later.

There are numerous other examples in the 138-year data set. The divergence between cyclically adjusted and current earnings can last for years, but in the end the two have always converged.

So where are we now? Analysts expect earnings per share for the S&P 500 of $164 for 2018, compared with cyclically adjusted earnings of $90. If the latter proves to be more accurate, the S&P 500 would have to decline by an additional 45 percent to maintain its current P/E ratio of 16 based on analysts’ earnings.

If you exclude the period before July 2011, when earnings were still recovering from the financial crisis, cyclically adjusted earnings rise modestly to $104. Based on those earnings, the S&P 500 would have to decline by 37 percent to maintain a P/E ratio of 16.

There are two caveats around all this. First, the next earnings recession could be more severe than cyclical adjustment implies. S&P 500 earnings declined 54 percent from peak to trough during the dot-com bust and 92 percent during the financial crisis, far worse than any adjustment would have indicated at the time. Some observers attribute the severity of those declines to changes in accounting rules in the 1990s that required companies to mark their assets to market. A more recent change extends those rules by requiring companies to report unrealized gains and losses from equity investments in net income, which may further exacerbate future earnings slumps.

Also, cyclical adjustments don’t provide any insight into timing, which brings me back to the recent sell-off. There have been five other corrections since the financial crisis, including one earlier this year, and each time the market recovered several months later. So the current correction doesn’t necessarily mean earnings are in trouble.

But with earnings at lofty levels and the risks rising from trade disputes and tighter monetary policy, investors should keep an eye on the S&P 500. If it continues to decline, earnings are most likely the next casualty.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2018 Bloomberg L.P.