(Bloomberg Opinion) -- National elections haven’t always been kind to European bonds in recent years. Italy, France and even the Netherlands saw yields fluctuate as emerging parties threatened to upend the political order and undermine the single currency.

It’s a different story in Spain. Though Prime Minister Pedro Sanchez last week called for national elections on April 28, government bonds have barely moved. And why should they? In Spain these days, a snap vote is no cause for alarm.

The current political turmoil stems from the socialist-led minority government’s reliance on Catalan independence parties for support. That recently fell away, leading to the failure of the 2019 budget bill, and the need for fresh elections.

As is frequently the case in European politics, no single party is likely to garner enough support to form a government. But following the collapse of the socialist coalition, it is far from certain whether a center-right grouping will win enough seats to form a majority in the 350-seat parliament. NatWest Markets analysts place the prospect of either a hung parliament or further elections at 50 percent and the prospect chances of a ruling combination of the People's Party and Ciudadanos at around 40 percent.

The most likely electoral outcome need not necessarily lead to higher yields. After all, Belgian debt held up remarkably well despite repeated long periods without an elected government. Really, only a protracted inability to pass a budget is likely to derail economic momentum.

And, a tie-up with one or more of the Vox far-right party, Basque separatists or even certain Catalans need not be a game changer. Though the issue of the latter’s independence is incredibly divisive, the difference in economic policy between the parties is relatively modest. So, even though a trial of 12 Catalan independence leaders is set to run throughout the election process, there’s good reason to expect that Spain's debt and equity markets will be relatively unperturbed.

If the April 28 elections do result in an administration that can pass a finance bill, this would further reinforce the bull case for Spanish bonds. It would complete the set of key positive factors for lower yields in Europe: above-average growth, the absence of a major political party currently pushing to leave the euro, and little political pressure to deviate from EU budget rules.

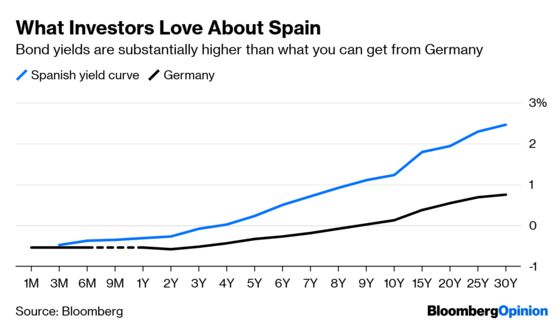

As I argued last week, Spain’s steep yield curve is attractive to yield-hungry investors. And any further stimulus from the European Central Bank, such as targeted long-term financing operations – will only add to its appeal relative to other government debt in the region.

This week has seen the announcement of a new 31-year bond from France and a Cyprus 15-year. If it weren’t for the election announcement, it might also have featured a long-dated Spanish syndication, and it might have gone very well – orders for last month's Spain 10-year sale reached a record 50 billion euros ($56.6 billion).

It’s understandable that investors will want to see how the election pans out. Political stability will be rewarded as the country will have the full hand of winning European cards. But even a limited period of uncertainty looks like it could be manageable.

If even a snap election can’t disturb Spanish debt, you know it’s in a whole new world of stability.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.