(Bloomberg Opinion) -- Spain's bond market has remained remarkably resilient in the face of the worsening political storm there. Several factors are encouraging investors to look beyond a potential failed budget for the country’s Socialist government and even fear of new elections.

Spanish 10-year yields may be low still, but they’re still 10 times that of German bunds. And that keeps them attractive to international investors; it’s all about the relative carry, to use a market term. So super-low German yields are more important in determining Spanish rates at the moment than any domestic troubles.

A bit of bad politics is far from unusual in Europe these days, and it’s going to take more to scare sovereign investors off from one of this year's more popular European destinations. As much of the euro zone is suffering from a sharp slowdown in growth, any subsequent stimulus move from the European Central Bank to boost weaker euro-area banks and economies will only highlight further Spain's relative benefits. It’s one of the least dirty shirts in Europe’s laundry basket.

Spanish GDP rose 2.4 percent in 2018, double the EU average. Helped by impressive structural reforms, the unemployment rate has halved since 2013, albeit from unacceptably high levels. That has allowed Spain to successfully detach from its bailout past and become part of the semi-core of the EU. Its credit is now rated A- (with a positive outlook) by S&P Global Ratings, three notches higher than during the euro crisis.

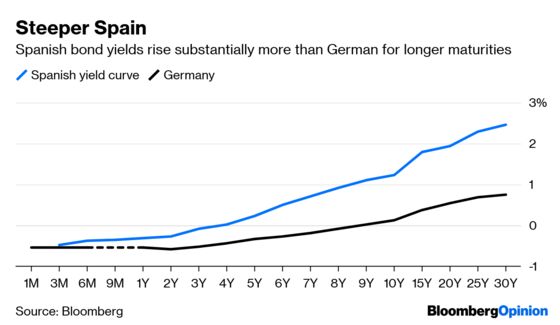

The relative steepness of the country’s yield curve is a big positive for investors too. Yields on Spanish three-month paper are within a few basis points of their German equivalents, but when you move up to 10-year maturities that widens to a 110 basis point spread. For a yield-starved bond market, that’s something to be snatched at. Remember, this is the euro area’s fourth-largest economy, but only Portugal, Cyprus, Italy and Greece yield more.

Japanese investors, who featured prominently in Madrid’s hugely popular 10-year bond sale last month, are particular fans. The negative rate on short-term euro debt means they can cut the cost of hedging their currency exposure. Spanish bonds are a compelling enough investment anyway compared to zero yields on Japanese 10-year maturities.

However, having your fortunes tied so closely to German yields cuts both ways. Spain is a higher beta market than Germany, meaning it carries more risk. So any upward spike in bunds would probably push up Spanish yields at an exponentially faster rate.

None of this is to say that local politics doesn’t matter at all. Should the crisis prevent any budget passing for a protracted period, that will put this new-found stability at risk. In the meantime, though, that steep yield curve should keep Spanish bonds out of serious trouble. Just keep an eye on Germany.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.