If Masayoshi Son Won't Invest in Japan, Why Should You?

(Bloomberg Opinion) -- Softbank Group Corp.’s Vision Fund has invested its $100 billion cash pile in 75 unicorns around the world. Not a single one is from Japan, its own backyard.

That may be because the pickings are slim: While the U.S. has 179 unicorns, China 93, and India 18, Japan has just two, according to CB Insights. How can a country that pioneered the Walkman and android robots fail to produce more valuable startups? The explanation may be somewhat arcane, but helps get to the bottom of a damaging cycle that’s left Japan with an uninspiring pool of fledgling innovators.

The listing standards for the small-cap Tokyo Stock Exchange Mothers Index are exceedingly low. To join Nasdaq, its New York counterpart, companies need a minimum of 1.25 million traded shares upon listing. That compares with just 2,000 for Mothers. This short hurdle, among others, means young, cash-hungry firms can tap public markets pretty easily, and sidestep the grinding process of courting investors through multiple rounds of funding.

The trouble is, size begets size. The bigger a company at listing, the greater the likelihood of attracting large chunks of institutional money and growing still larger. (It pays to be patient.) What’s left is an index stuffed with unreliable runts: 96% of Mothers's 283 components have a valuation of less than $1 billion, compared with roughly one-third for Nasdaq. The Japanese index was notorious for its scandal-studded constituents in the past, and remains volatile.

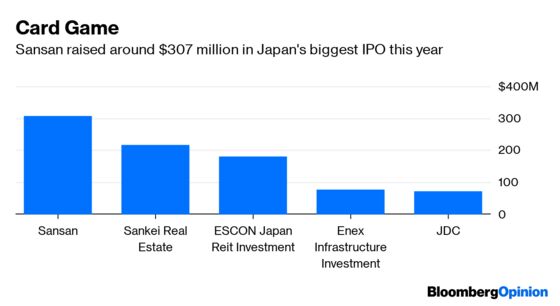

Just two Japanese unicorns have gone public in the last two years, with mixed results: Flea market app Mercari Inc. is down 4% since raising $1.2 billion last June, while business-card scanner and networking firm Sansan Inc. is up 33% after listing last month. The two unicorns left include four-year-old Preferred Networks Inc., whose app uses artificial intelligence to automate the coloring of manga cartoons, and Tokyo-based cryptocurrency trading platform Liquid Group Inc.

With few appealing options, the likes of Masayoshi Son take their venture-capital dollars elsewhere. But the bigger the funding vacuum, the greater the incentive startups have to list early and small. And so the cycle continues.

There are cultural challenges to Japanese innovation, too. Attracting young graduates to unsteady jobs can be a tough sell: Many would rather join Toyota Motor Corp. or other established firms. Japanese founders also have a reputation for crippling timidity when asking for money, unlike their brazen rivals in Silicon Valley.

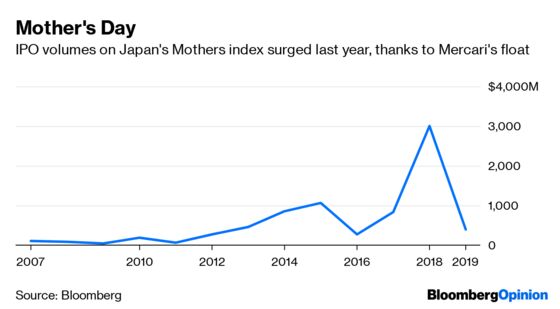

That’s not to say that startup activity has plateaued. Venture funding hit a record $3.5 billion last year, though that’s a shadow of levels in the U.S. and China, which both top out at more than $100 billion. This year, the Mothers index is up around 20% in local currency terms, outperforming the 9% gain for the benchmark Topix index, and IPO volumes reached a high last year.

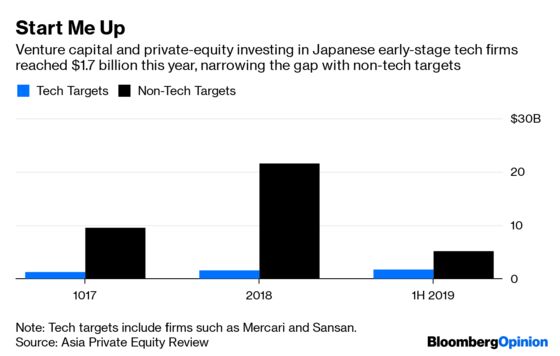

Attitudes are also changing. Startups are losing their stigma and luring more graduates, Yoshito Hori, managing partner of domestic venture-capital firm Globis Capital Partners told the AVCJ Japan Forum last week in Tokyo. Funding into early-stage tech firms reached $1.7 billion this year, according to Asia Private Equity Review, compared with more than $1.6 billion in all of 2018.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.