(Bloomberg Opinion) -- The trading debut of SoftBank Group Corp.’s Japanese telecom unit shows the perils of buying into an IPO purely for the dividend yield.

SoftBank Corp., as the new entity is known, was heavily marketed to individual investors, who took up a majority of the 90 percent of shares that were sold domestically. Institutional investors were less keen. Their caution looks warranted, with the stock dropping as much as 10.4 percent Wednesday in Tokyo.

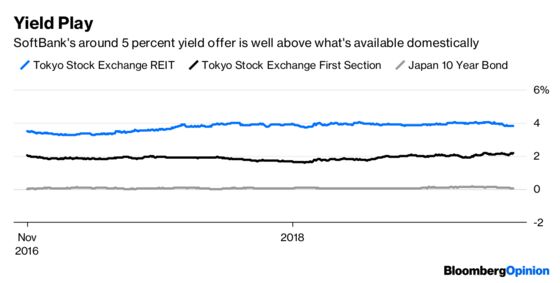

The wireless business offers a yield of 5 percent to 5.4 percent, according to analysts. That’s an attractive proposition for retail investors – the fabled Mrs. Watanabe – in a country where interest rates are negative. It’s also well above the 4.4 percent payout on shares of NTT DoCoMo Inc. and 3.8 percent for KDDI Corp.

The IPO targeted individuals through TV adds and apps that made it cheaper for small investors to buy. That was no accident: Japan Post Holdings Co.’s $11.6 billion offering last year showed the hunger for yield.

But the signs of trouble were there. Since bankers started taking orders on Dec. 3, sentiment toward the Japanese market has cratered, with SoftBank Group faring even worse: The technology investor’s shares have fallen 15 percent, compared with a 7.9 percent decline in the Topix index.

That juicy dividend yield will inevitably decline as the company’s cash flow faces headwinds. The telecom firm is promising a payout ratio of about 85 percent but those earnings will be hard to sustain. Competition is increasing in the Japanese mobile market, with the entry of a fourth operator in Rakuten Inc., and the government is pressuring SoftBank to lower its tariffs, as we noted last week. Moreover, the company must shoulder the cost of building out 5G operations.

There’s also the liability of the relationship with its parent, which retains a 67 percent stake and has a history of draining cash from its wireless division. With SoftBank Group’s debt continuing to rise, and a growing backlash against Saudi Arabia – the biggest investor in its $100 billion Vision Fund – the parent’s need for cash is unlikely to diminish.

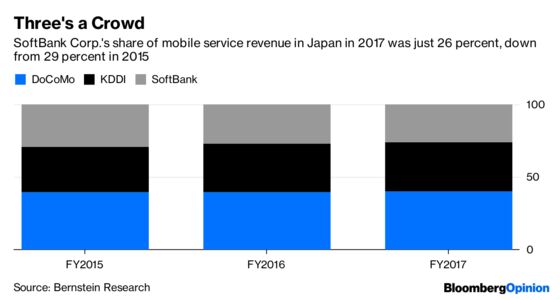

Compared with rivals DoCoMo and KDDI, SoftBank Corp. is a lot more leveraged. The company is also relatively expensive, with an enterprise value to Ebitda ratio of 8.2 times versus 5.5 times for market leader DoCoMo and 4.4 times for the faster-growing KDDI, Bernstein Research analyst Chris Lane notes.

SoftBank founder Masayoshi Son understood that if enough individual investors could be persuaded to buy in, institutional investors would be forced to follow given the size of the business. The $23.6 billion SoftBank raised makes it the world’s largest flotation since Alibaba Group Holding Ltd.’s $25 billion New York listing in 2014.

That was a smart strategy, at a time when institutional investors have been worrying that we’ve reached peak tech. The six lead underwriters on the deal, from Japan's Nomura Holdings Inc. to Goldman Sachs Group Inc. and JPMorgan Chase & Co., have also all extended loans to SoftBank, totaling about 1 trillion yen ($8.9 billion) collectively, Nikkei reported last month. Other banks vying to get a spot on the deal had been asked to fork out funds, it said.

Son, at least, has been left sitting pretty. As for Mrs. Watanabe, watch out for calls to the telecom unit’s complaints line.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2018 Bloomberg L.P.