SoftBank Buyback Magic May Soon Wear Thin

There are risks for the Japanese technology investor in deciding to spend $5.5 billion on its own stock.

(Bloomberg Opinion) -- Day traders may be rejoicing at SoftBank Group Corp.’s biggest ever buyback, but for loyal believers in Masayoshi Son’s magic wand, it’s another worrisome development.

SoftBank unveiled the repurchase program last week, promising to spend as much as 600 billion yen ($5.5 billion) on its own stock over the coming year. That would be enough to buy 71 million shares, or 6.5 percent of the total, based on the closing price on Feb. 5. There’s an upper limit of 112 million shares, or 10.3 percent of the total.

That’s a lot of buybacks — good news, right? SoftBank’s shares soared 17.7 percent to a four-month high on Thursday.

There’s a risk in such largess, though. Buybacks shrink the public float, potentially reducing SoftBank’s weighting in benchmark indexes and causing passive investors that track those gauges to cut their holdings. As a result, market sentiment toward buybacks among institutional investors is shifting, with large repurchases increasingly seen as inferior to special dividends.

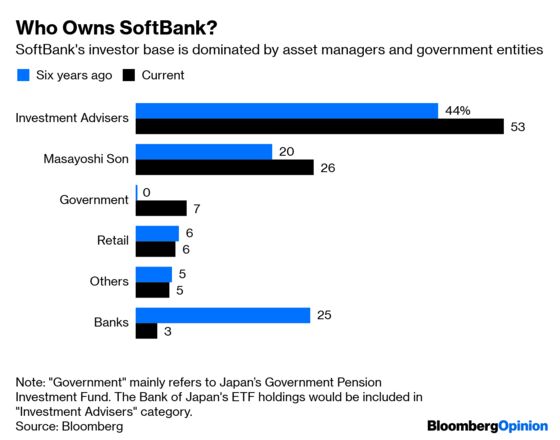

Passive investing has been on the rise since Japan’s central bank started buying stock ETFs in early 2013. Over the last three years alone, Japanese ETFs received more than $140 billion of net inflows. Billions will have gone into SoftBank, a member of both the Nikkei 225 Index and the Topix. Nomura Holdings Inc., which manages a $77 billion Topix ETF, owns 4.9 percent of the company. Japan’s Government Pension Investment Fund has become the second-largest investor after tilting toward equities in late 2014.

Keeping a large public float is how to play passive money. Hong Kong-listed HSBC Holdings Plc, for instance, is a master at that game. Dividends rather than share buybacks are the main channel through which the bank rewards its shareholders. Investors can elect to receive payments in cash, or as a scrip dividend in the form of new shares. As a result, HSBC has a 9.4 percent weighting — the third largest — on the benchmark Hang Seng Index, even though it’s not in the top five in terms of total market value.

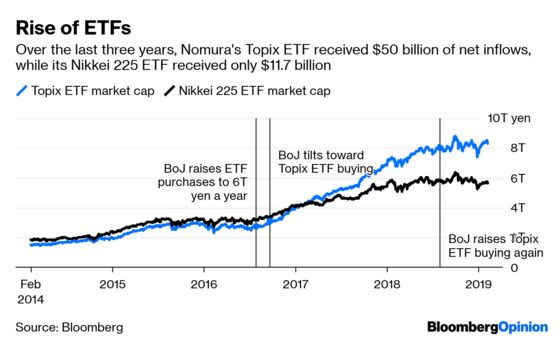

Mindful of the unscientific construction of the Nikkei index, which assigns weightings based on price levels, the Bank of Japan has been steadily moving toward the market-weighted Topix Index, which scrutinizes a firm’s public float. Over the last three years, Nomura’s Topix ETF received more than $50 billion of net inflows, while its Nikkei 225 ETF got less than half that amount.

So SoftBank has to be careful. It has a 5.4 percent weighting in the Nikkei 225 because of its relatively high stock price (about 10,000 yen compared with, say, less than 5,000 yen for Sony Corp. or 570 for Mitsubishi UFJ Financial Group Inc.). But SoftBank accounts for only 1.9 percent of the Topix.

It’s surprising that a company financially savvy enough to use collar trades to limit losses in its Nvidia Corp. holdings wouldn’t know the pitfalls of share repurchases.

Chances are, a splashy buyback was seen as having a public relations value that a dividend payout couldn’t provide. Son is now back in the media limelight, bemoaning the valuation gap his flagship holding company is suffering. The buyback also rewards investment banks, which can earn money from executing the trades. Dividends, on the other hand, are just boring checks from the company’s finance department that don’t involve reporters or brokers.

Son has alienated many fans in the past year. Last March, he threw holders of SoftBank dollar bonds under the bus as part of preparations for the firm’s domestic telco IPO. Small individual investors in Japan, who long supported Son’s quest to buy up the world’s hottest unicorns, are now feeling burned after the offering flopped.

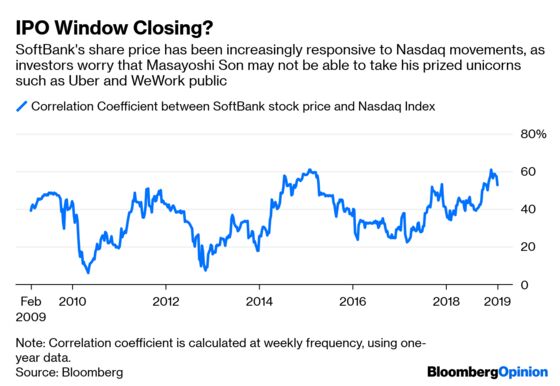

Cash dividends are money in the bank, while a run-up in the stock price is just a paper gain that can evaporate quickly. With SoftBank’s fortunes increasingly tied to the Nasdaq, all it would take is another correction in U.S. tech stocks for that to happen. Son had better be careful not to alienate fund managers this time; otherwise he may find himself running out of supporters.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.